YTL Hospitality REIT (Dec 30, RM1.09)

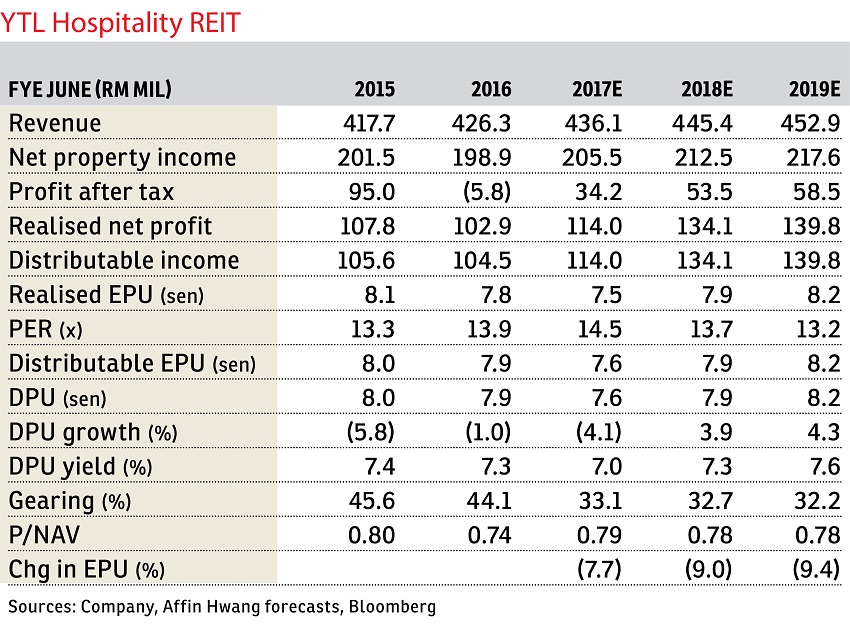

Maintain buy call with a lower target price of RM1.38: On Dec 16, 2016, a RM402 million equity private placement was raised, comprising 380 million new shares in YTL Hospitality Real Estate Investment Trust (YTL REIT). Proceeds from the placement will be utilised to de-gear existing Malaysian bank borrowings (based on a cost of debt of 4.9%). The higher distributable income — as a result of interest savings — will be distributed back to shareholders.

Due to the higher cost of capital from the proceeds, as it is based on a cost of equity of 8.08% vis-à-vis a cost of debt of 4.9% (with bank borrowings), distributable income (per unit) to the common equity shareholders of YTL REIT had been diluted by 7.7% for its financial year ending Dec 31, 2017 (FY2017), and 9% and 9.4% for FY2018 and FY2019. This is despite an increase of 16% to 17% in absolute distributable income. In our FY2017 forecasts, we have also factored in administrative cost of RM4 million due to placement fees.

FY2017 to FY2019 distribution per unit yields remain attractive at 7% to 7.6% while trading at price per net asset value of 0.73 times. With an anticipated lower gearing of 0.33 times (with the repayment of bank borrowings) compared with 0.44 times previously, YTL REIT could gear up by approximately RM617 million (based on a 60% limit which was approved by shareholders) for future acquisitions.

Compared with peers, management of YTL REIT could at any time inject mature properties under the stable of YTL Hotels & Properties Sdn Bhd (the hospitality arm of YTL Corp Bhd) into YTL REIT. Meanwhile, management is also constantly on the lookout for strategic acquisitions in more robust cities such as London. Key risks to our call include i) non-renewal of lease agreements, ii) a sharp slowdown in economic growth, especially in Australia’s key cities, iii) higher debt-refinancing rates, and iv) a steepening of the 10-year Malaysian Government Securities yield curve would continue to dampen REIT valuations. — Affin Hwang Capital, Dec 30

This article first appeared in The Edge Financial Daily, on Jan 3, 2017. Subscribe to The Edge Financial Daily here.

TOP PICKS BY EDGEPROP

Livia @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Chimes @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Penduline @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Penduline @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Robin @ Bandar Rimbayu

Telok Panglima Garang, Selangor

D'Ambience Residences (Ikatan Flora), Bandar Baru Permas Jaya

Permas Jaya/Senibong, Johor

D'Carlton Seaview Residences (Seri Mega)

Masai, Johor

Apartment Tanjung Puteri Resort

Pasir Gudang, Johor

{kind=link}