Kerjaya Prospek Group Bhd (May 12, RM3.11)

Downgrade to market perform with an unchanged target price (TP) of RM3.10: Last Thursday, Kerjaya Prospek Group Bhd announced that they had secured a project known as “Hometree — Phase 2” worth RM207.4 million from BCB Bhd.

The scope of works comprises main building works for 166 units of three-storey semi-detached houses, 99 units of three-storey bungalows, a two-storey club house, two security guard houses, four electrical substations and a single-storey mosque at Seksyen 31, Shah Alam, Selangor — slated for completion by September 2019 (around 29 months duration).

We note that this is the second project Kerjaya is securing from BCB whereby the first project (worth RM313 million) was secured back in May 2016.

We are “neutral” about the award, given that Kerjaya’s year-to-date (YTD) wins of RM239 million are still within our financial year ending Dec 31, 2017 (FY17) replenishment target of RM1.6 billion; making up 15% of our replenishment target with a remainder of RM1.36 billion to be achieved for the rest of year.

Assuming profit before tax margins of 14%, this newly secured project is expected to contribute about RM10.4 million to Kerjaya’s bottom line per annum.

Post-award, Kerjaya’s outstanding order book stands at around RM2.5 billion providing healthy earnings visibility for the next two years.

We believe Kerjaya is set to achieve our replenishment target of RM1.6 billion mainly backed by projects from Eastern & Oriental Bhd, S P Setia Bhd and Datuk Tee’s (major shareholder of Kerjaya) private property arm.

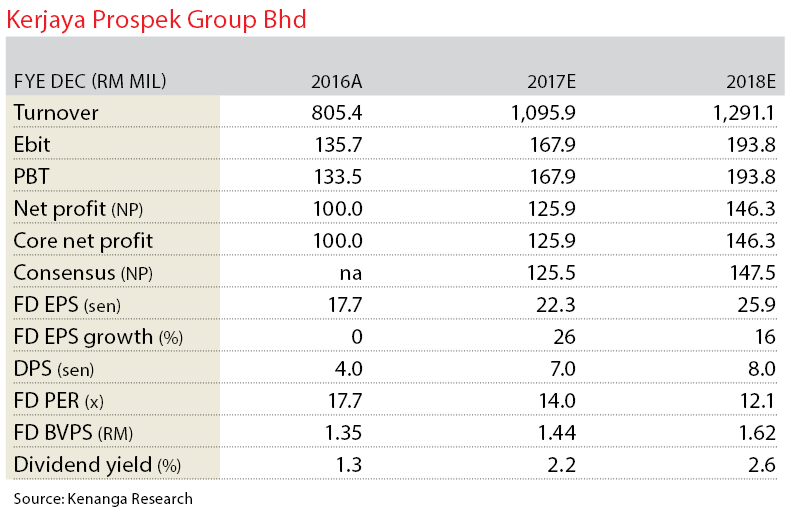

Post-award, we make no changes to our FY17 to FY18 core net profit RM125.9 million to RM146.3 million.

YTD, Kerjaya’s share price has performed very well registering gains of 43.8%, also hitting our TP of RM3.10. Given the rally, we believe the risk-to-reward ratio is no longer as compelling and thus, downgrade our call to “market perform” (from “overperform”) with an unchanged sum of parts-derived TP of RM3.10.

Our TP implies 12 times FY18 price-earnings ratio in line with our targeted peers’ range of nine times to 13 times. We note that while our valuation is at the higher end of our targeted range, we deem it fair considering that Kerjaya’s net margins of around 11% remain superior over peers’ (Mitrajaya Holdings Bhd, Hock Seng Lee Bhd, Kimlun Corp Bhd) average of 9%.

Risks to our call include lower-than-expected replenishment and margins, delays in construction works. — Kenanga Research, May 12

This article first appeared in The Edge Financial Daily, on May 15, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Wangsa Maju Seksyen 5

Wangsa Maju, Kuala Lumpur

Duduk Se.Ruang @ Eco Sanctuary

Kuala Langat, Selangor

Pulau Indah Industrial Area

Pulau Indah (Pulau Lumut), Selangor

{kind=link}