Malaysia Building Society Bhd (Nov 7, RM1.17)

Maintain buy with an unchanged target price of RM1.50: Malaysia Building Society Bhd (MBSB) has moved a step closer to become a full Islamic financial institution after the previous two failed merger attempts — with Bank Muamalat, and with CIMB Group and RHB Bank.

On Monday, the group announced that it will acquire a 100% stake in Asian Finance Bank (AFB). The proposed exercise will result in the acquisition of AFB’s deposit-taking licence. The full bank licence will allow MBSB to tap into financial services which it currently cannot offer (such as trade facilities, current account and savings account deposits, and interbank instruments).

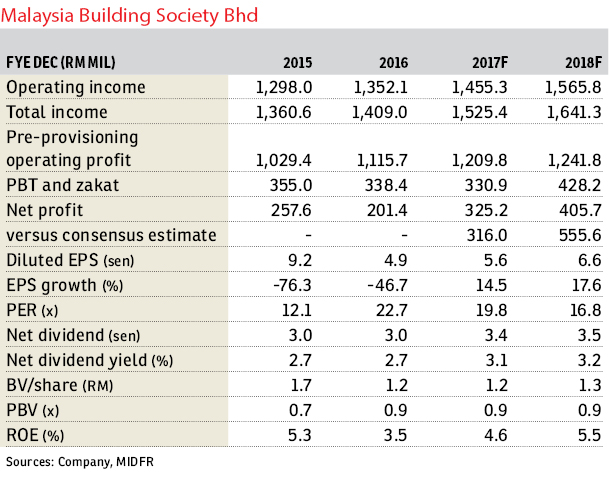

The purchase consideration for the acquisition is RM644.95 million. This represents a price-to-book value (PBV) of 1.3 times, based on net assets as at Dec 31, 2016, of approximately RM497.26 million.

The purchase consideration will be satisfied through a combination of cash amounting to RM396.9 million and the issuance of 225.5 million of new ordinary shares in MBSB at an issue price of RM1.10 per consideration share.

We believe that the valuation of the merger is fair. Our view is premised on valuations of previous financial-sector mergers of approximately 1.4 times PBV.

Pursuant to the merger exercise, MBSB will transform its status to a full-fledged Islamic bank. The group is expected to emerge as the second-biggest Islamic bank in Malaysia after Bank Islam, with total estimated assets of RM44 billion.

The transition of MBSB into syariah status will require the company to transfer its syariah-compliant assets and liabilities (A&L) to AFB in tranches.

All the residual conventional financial A&L, which cannot be converted into Islamic A&L, will be disposed of to third parties. MBSB is expected to obtain its full Islamic status in two to three years’ time, pending the completion of this transfer consideration.

In terms of the new share issuance, the dilutive effect will be minimal. Assuming a shareholder with a 10% stake in the group, post merger the shareholding will drop to only 9.6%.

In addition, we believe that the merger will enhance the group’s growth potential, which would increase its future value and compensate the dilution.

MBSB’s forward strategy now will be to enhance its focus on upgrading the company’s digital capacity to improve the existing business and operating model.

The new banking platform will leverage digitalisation to capture fee-based income from both consumers and corporates.

Additionally, the company is expected to solidify its presence in the niche segments, which primarily comprise property, housing and infrastructure.

We believe the acquisition of the banking licence will stimulate an upward trajectory of MBSB’s operating income.

This is premised on the new banking platform of MBSB, which is now able to offer Islamic universal banking services to both retail and wholesale banking customers such as, among others, wealth management, foreign exchange, investment banking, debt capital management and trade finance.

The future looks rosy for MBSB given the encouraging progression of Islamic finance in the region.

With Malaysia being an important part of Islamic finance development, MBSB is poised to benefit in the long run, both locally and internationally.

This is taking into account growing demand for Islamic financial products and the favourable consumer demographic in Malaysia.

As such, this positive trend provides a vast array of opportunities for MBSB to grow, with syariah-compliant financing expected to account for 40% of total financing in Malaysia by 2020.

The proposed acquisition will not have any material effect on our financial year ending Dec 31, 2017 (FY17) earnings forecast.

This is premised on the expectation that the proposed merger will be completed in the first quarter ending March 31, 2018.

Also, we opt to maintain our earnings forecasts for FY18 at this juncture, pending further management guidance on the expected earnings contribution after the completion of the proposed merger. Accordingly, management has indicated that guidance will be made available in calendar year 2018. — MIDF Research, Nov 7

TOP PICKS BY EDGEPROP

Residensi Hijauan (The Greens)

Shah Alam, Selangor

Baypoint @ Country Garden Danga Bay

Johor Bahru, Johor

Menara Bintang Goldhill

Bukit Bintang, Kuala Lumpur

Pangsapuri Akasia, Bandar Botanic

Bandar Botanic/Bandar Bukit Tinggi, Selangor

Pangsapuri Akasia, Bandar Botanic

Bandar Botanic/Bandar Bukit Tinggi, Selangor

Bandar Bukit Tinggi

Bandar Botanic/Bandar Bukit Tinggi, Selangor

hero.jpg?GPem8xdIFjEDnmfAHjnS.4wbzvW8BrWw)

{kind=link}