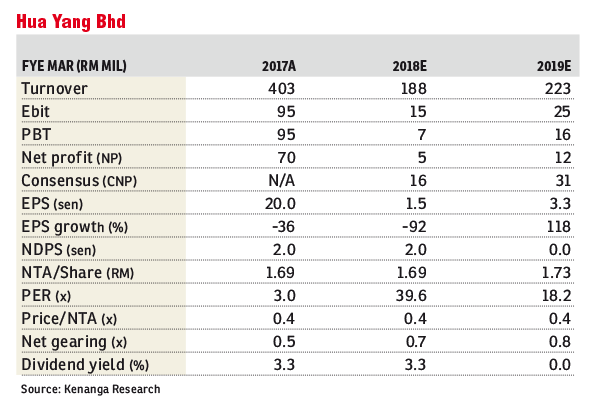

Hua Yang Bhd (Dec 28, 60.5 sen)

Upgrade to market perform with a lower target price (TP) of 63 sen: Yesterday, Hua Yang Bhd announced that it is acquiring four parcels of freehold land measuring 19.8 acres (8ha) for a total consideration of RM70 million or at RM81.3 per sq ft (psf). The land is adjacent to the Kajang 2 development and is accessible via Jalan Reko via the Kajang SILK Highway.

We were surprised with Hua Yang’s land banking move as we were not expecting any land banking activities for the year, given its high net gearing of 0.70 times (as of second quarter ended Sept 30, 2017 [2QFY18]).

Hua Yang’s management estimates a gross development value (GDV) of RM800 million for these four parcels of land, which we believe is fair as it would translate to an average selling price of RM300 psf derived from four times plot ratio, enabling them to position its product below RM500,000 per unit in the Klang Valley for the affordable segment. In terms of land cost, we deem that it is reasonable as the land cost to GDV ratio of 8.8% is still within our comfortable range of 15% to 20%.

While we are positive with its land bank replenishment, we remain worried about its high net gearing of 0.70 times (as of 2QFY18) which is set to reach 0.82 times upon completion of the deal.

Going forward, we are not expecting any more major land banking activities as we believe that Hua Yang needs to focus on realising their pipelines and also future plans with Magna Prima Bhd.

Considering its unbilled sales, which have fallen to a historical low of RM209 million, which is only sufficient for another one to two quarters, we opine that Hua Yang should be more aggressive driving its sales from launched projects that received a slow response from the market, inspite of its positioning as an affordable housing player (more than 50% of products priced around RM550,000 per unit) in the Klang Valley, Penang and Johor.

As we believe that the average selling price of RM300 psf for its Kajang land is reasonable in the long term, we think that Hua Yang will need to step up its marketing efforts, as it is set to face stiff competition from other developers in Kajang, given that the current pricing for condo/apartments ranges between RM240 psf and RM260 psf.

Following its land banking move, we maintain our financial year ending March 31, 2018 (FY18)/FY19 earnings for now as we are only expecting the earliest launch from these four parcels of land to take place in FY20.

Risks to our call includes lower-than-expected sales, higher-than-expected administrative costs, negative real estate policies, less conducive lending environments, and lower-than-expected dividend payout. — Kenanga Research, Dec 28

This article first appeared in The Edge Financial Daily, on Dec 29, 2017.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Taman Industri Oug

Jalan Klang Lama (Old Klang Road), Kuala Lumpur

Taman Industri Oug

Jalan Klang Lama (Old Klang Road), Kuala Lumpur

Bandar Puteri Puchong

Bandar Puteri Puchong, Selangor

Kinrara Anggun

Bandar Kinrara Puchong, Selangor

The Zest @ Kinrara 9

Bandar Kinrara Puchong, Selangor

The Zest @ Kinrara 9

Bandar Kinrara Puchong, Selangor

Boulevard Residence Damansara

Kayu Ara, Selangor

Boulevard Residence Damansara

Kayu Ara, Selangor

{kind=link}