Crescendo Corp Bhd (March 30, RM1.33)

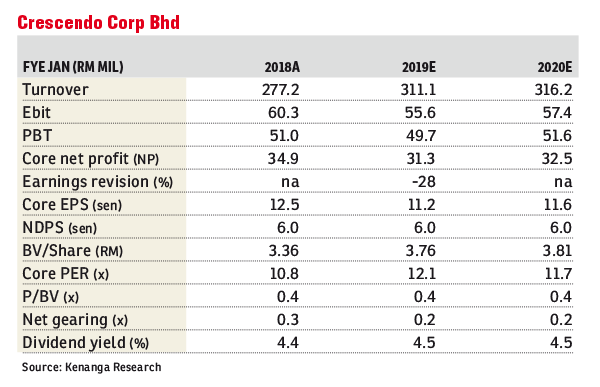

Maintain market perform with a lower target price (TP) of RM1.30: Financial year 2018 (FY18) core net profit (CNP) of RM34.9 million came in below expectations, making up 82% of our full-year estimate. The negative variance is due to lower-than-expected margin arising from higher mix of low-cost housing products compared to industrial and commercial ones. Positively, full-year property sales of RM271.2 million came in higher compared to our target of RM221 million. A three sen dividend was declared, bringing the full-year dividend to six sen, in line with our full-year target.

FY18 CNP grew 21%, underpinned by: revenue growth of 9%, and improvement in earnings before interest, taxes, depreciation and amortisation (Ebitda) margin by three percentage points (ppt) from 21%. The improvements in revenue and margins are mainly driven by higher property sales compounded by change of sales mix with higher proportion of industrial property sales that generally commands higher margin. Quarter-on-quarter-(q-o-q) wise, fourth-quarter 2018 (4QFY18) CNP registered a sharp plunge of 77% despite flattish revenue as it saw major compression in Ebitda margin to 13% (-12ppt) mainly due to higher proportion of sales of affordable housing, which has extremely low margins.

Currently our outlook, its unbilled sales stand at RM190.5 million providing less than one year’s visibility. Going forward, Cresendo Corp Bhd (Cresendo) is planning to launch 102 units of mid-market landed residential properties at Bandar Cemerlang, 24 units of shop offices at Bandar Cemerlang as well as 426 units of affordable housing at Bandar Cemerlang and Tanjung Senibong with a combined gross development value of more than RM100 million in the medium-to-near term.

Post results, we reduce our FY19E CNP by 28% after factoring in a lower margin arising from a higher component of low-cost housing and also introduce our FY20E of RM32.5 million.

Post results, we reiterate our “market perform” call on the stock with a lower TP of RM1.30 (from RM1.50) based on a higher revalued net asset valuation discount of 79% (previously, 76%) which is at its historical high levels. We believe such valuations levels are fair considering its full exposure to Johor. — Kenanga Research, March 30

This article first appeared in The Edge Financial Daily, on April 2, 2018.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Livia @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Robin @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Penduline @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Chimes @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Penduline @ Bandar Rimbayu

Telok Panglima Garang, Selangor

Taman Tun Dr Ismail (TTDI)

Taman Tun Dr Ismail, Kuala Lumpur

Pangsapuri Akasia, Bandar Botanic

Bandar Botanic/Bandar Bukit Tinggi, Selangor

Pangsapuri Akasia, Bandar Botanic

Bandar Botanic/Bandar Bukit Tinggi, Selangor

Pangsapuri Akasia, Bandar Botanic

Bandar Botanic/Bandar Bukit Tinggi, Selangor

Bandar Bukit Tinggi

Bandar Botanic/Bandar Bukit Tinggi, Selangor

Kawasan Industri Desa Aman

Sungai Buloh, Selangor

{kind=link}