")

KUALA LUMPUR (Feb 3): Real estate investment trusts (REITs) are expected to be sought after, more so after Bank Negara Malaysia’s recent cut in the overnight policy rate (OPR) by 25 basis points which resulted in lower bank deposit rates.

The OPR cut, which had an impact on Malaysian Government Securities (MGS) yields could drive investors for alternative yielding assets, said Affin Hwang Capital Research.

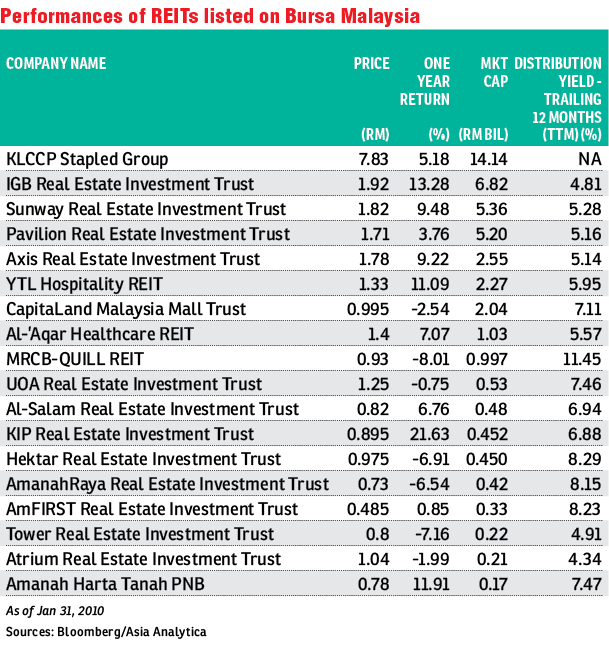

“We anticipate the compression in MGS yields to drive investors to demand alternative yielding assets such as REITs, thereby rerating the sector’s valuation,” it added. Currently, REITs listed on Bursa Malaysia are offering yields at above 4% (see table), compared with banks’ fixed deposit rates of below 3%.

Rakuten Trade Research vice-president Vincent Lau believes that REITs would do well in a low-interest rate environment, particularly those who are in the retail space.

“REITs would do well in a low-interest-rate environment. In particular, retail REITs are expected to be resilient as high tenant occupancy alongside food and beverage (F&B) demand in shopping malls will continue to be a driving force for footfall,” said Lau, who cited REITs such as Pavilion REIT and IGB REIT will fare well in 2020.

Meanwhile, TA Securities concurred that a rate cut could serve to restore the attractiveness of REITs vis-à-vis the yields of other fixed income instruments.

TA Securities forecasted an 8.1% year-on-year (y-o-y) growth in the distribution per unit (DPU). This growth is expected to be driven by higher rental post asset enhancement initiatives (AEIs), contributions from newly acquired assets and better operational efficiencies.

Should domestic economic activities continue to gain traction, TA Securities noted that the potential upside to its DPU forecasts is present. Balance sheet-wise, REITs’ financial footing remains solid according to TA, with an average gearing ratio of the REITs that it covers standing at 36.1% as at Sept 30, 2019, while the debt maturity is well spread and financing costs are expected to remain stable.

“Over the near term, we believe refinancing risks are low as REIT managers have been proactive, taking advantage of the current accommodative interest environment to lengthen debt tenures, refinance loan ahead of maturities and establish new loan facilities for future drawdown,” said TA Securities.

REITs that own mall and hotel assets are expected to perform better pinning hope that the Visit Malaysia 2020 programme will help to draw higher tourist arrivals for the year.

Beside the rate cut that has made REIT attractive to yield-seeking investors, lower interest rate also help to reduce financing costs for any asset acquisitions.

PublicInvest Research said in a recent research note dated Jan 23, the low-interest-rate environment could serve to stoke risk-appetite for asset acquisitions, as they are generally funded by borrowings.

However, from the earnings perspective, PublicInvest Research opined that the impact of the OPR cut would be mildly positive, as there would be cost savings from lower interest rates on the floating rate debts owed by REITs.

“That said, impact to earnings is marginal with the lower finance costs only expected to increase earnings [of those REIT with floating rates] by circa 1%,” opined PublicInvest Research.

The research house added that of the REITs it covers, Sunway REIT’s floating-rate loans account for 57% of its loans, while Axis REIT is 21%. Over at IGB REIT, all its borrowings are placed at fixed rates.

Affin Hwang Capital viewed that the OPR cut would reduce REITs finance costs and lift earnings, but impact on near term profits in 2020 and 2021 is likely minimal.

“Most of the MREITs under our coverage [Axis REIT, IGB REIT, KLCCSS and YTL REIT] have the majority [more than 70%] of their borrowings pegged at a fixed rate, while the others have pegged 43% of their borrowings at a fixed rate,” noted AffinHwang.

AffinHwang has maintained its overweight call on the REIT sector, and highlighted KLCCP Stapled Group is highly defensive in terms of earnings and its yield is sustainable.

It also liked Axis REIT for its industrial and warehouse portfolio and attractive valuation, and IGB REIT for its prime assets, robust earnings track and strong management.

This article first appeared in The Edge Financial Daily, on Feb 3, 2020.

TOP PICKS BY EDGEPROP

Taman Perindustrian Bukit Serdang

Seri Kembangan, Selangor

Putra Indah Condominium

Seri Kembangan, Selangor

Putra Indah Condominium

Seri Kembangan, Selangor

City of Green Condominium

Seri Kembangan, Selangor

Pusat Bandar Putra Permai

Seri Kembangan, Selangor

{kind=link}