LBS targets RM1.5 bil sales for 2017

LBS Bina Group Bhd (Jan 18, RM1.74)

Maintain add with an unchanged target price (TP) of RM2.15: We spoke to management for an update on LBS Bina Group Bhd. Work has been progressing well at the start of 2017 and we believe that the potential rerating catalysts for LBS’s share price are intact. These include stronger sales, unlocking of the Zhuhai land value and stronger interest in Bursa-listed ML Global Bhd, an LBS subsidiary.

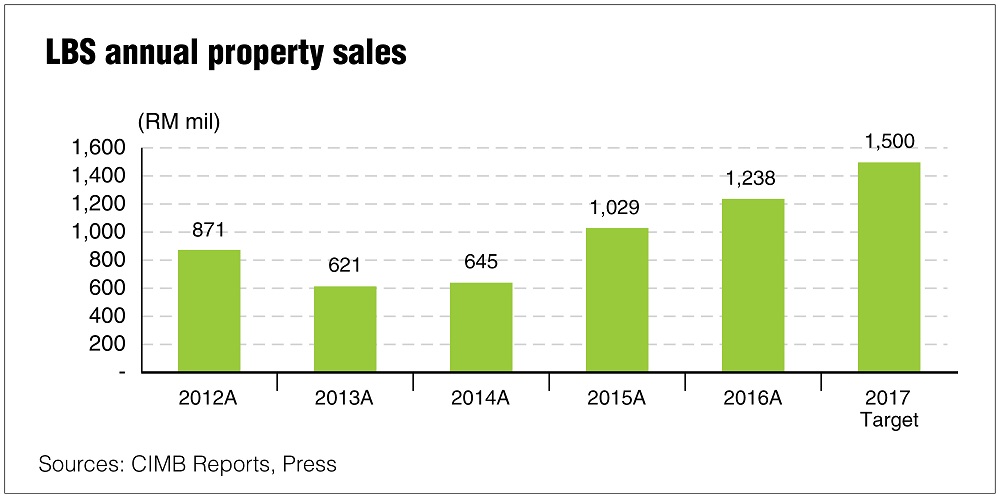

LBS recently announced that it achieved RM1.24 billion worth of sales in 2016, surpassing its RM1.2 billion target. In 2017, it aims to sell RM1.5 billion worth of properties. The company is confident that it will achieve the 2017 target as it plans for 13 new launches (comprising mostly mass-market housing), with a combined gross development value (GDV) of RM2.35 billion this year. One-third of the launches are expected to take place in the first half of 2017 (1H2017), while the remaining launches are planned for 2H2017.

While new property sales are typically lower in the early part of the year, we gathered from the company that its recent sales performance has been strong. LBS just launched the final block of its RM1.4 billion BSP21 project over the weekend. We estimate that this block has a potential GDV of about RM200 million and expect it to be one of the key sales contributors for the company in first quarter of 2017.

On the international front, LBS still targets to obtain regulatory approval to upgrade its 60%-owned Zhuhai International Circuit (ZIC) in China in 1H2017. The approval could pave the way for LBS to unlock the value of ZIC’s land by upgrading it to an integrated tourist attraction. The approval may also be positive for LBS’ share price as ZIC’s comprises 16% of LBS’ revised net asset value by our estimates.

The share price of ML Global, a 56%-owned listed subsidiary of LBS, has risen by 40% since LBS announced the injection of its construction arm into the listed entity in September 2016. Including the convertible preference shares, LBS’ stake in ML Global is worth RM286 million based on ML Global’s closing share price on Monday. This is 26% of LBS’ current market cap.

We understand from LBS that ML Global is likely to undertake the construction jobs for LBS’ projects as ML Global is LBS’ subsidiary. The strong pipeline of new launches by LBS could provide sustainable job awards to ML Global and support the latter’s earnings and share price. On top of that, ML Global targets to win more external jobs to drive earnings growth in the near future. We maintain “add”. The prospects of stronger sales in 2017, approval for ZIC upgrade in 1H2017 and good share price performance by ML Global are the key potential rerating catalysts for LBS’ valuation. These catalysts, coupled with the potential dividend yield of 7% in 2017, make LBS one of our top picks among Malaysian developers. Key risk to our “add” call is a sharp deterioration in sentiment on the local property market. — CIMB Research, Jan 17

This article first appeared in The Edge Financial Daily, on Jan 19, 2017. Subscribe to The Edge Financial Daily here.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.