Further competition ahead for Hua Yang

Hua Yang Bhd (Jan 19, RM1.07)

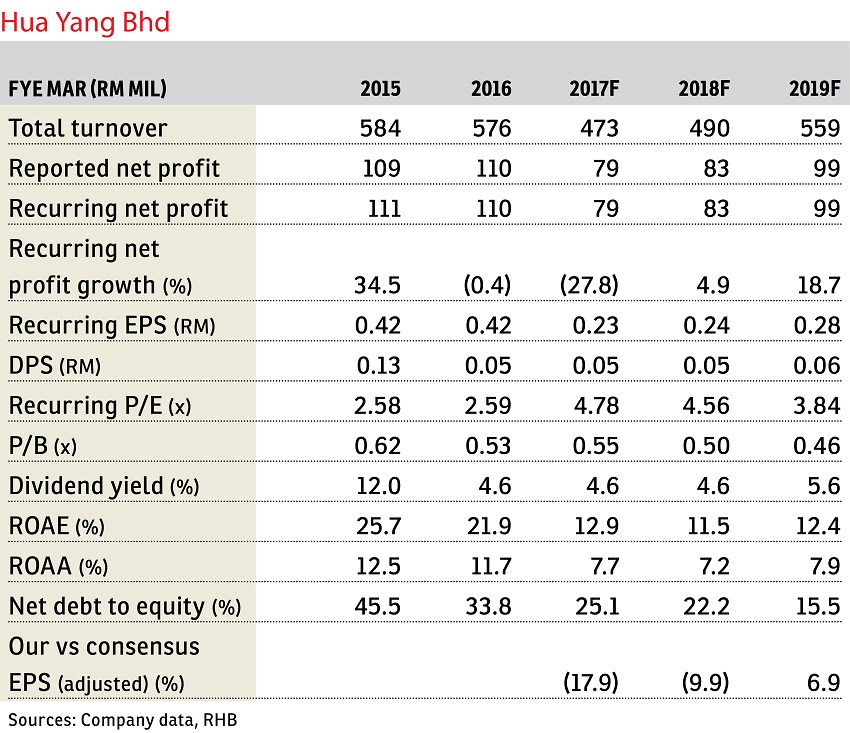

Maintain neutral with a lower target price (TP) of RM1.05: We believe the relaxation of the 1Malaysia People’s Housing Programme (PR1MA) housing policies would have a negative impact on Hua Yang Bhd. This is as the company is in the affordable housing and high-rise segment in the Klang Valley with the property prices of around RM500,000. The new policies may pose a threat to Hua Yang, as the government has cut the moratorium period for PR1MA housing to five years, from 10 years. The government has also raised the household income eligibility to RM2,500 to RM15,000 per month, from RM2,500 to RM10,000 per month.

Although two new projects have been previewed in the last quarter (Astetica Residence in Seri Kembangan, Selangor and Meritus Residensi in mainland Penang), we think the bookings may not be converted so soon. Hence, full-year new sales may fall short of management’s revised sales target of RM300 million. We think RM220 million to RM250 million would be a more realistic target, given the current weak market conditions. Note that, we have already factored in the lower sales into our forecasts earlier.

During the briefing yesterday, the management highlighted that the gross development value (GDV) for its Puchong West is now higher at RM2.02 billion from RM1.3 billion. The higher GDV was due to the development order that the company had just received, higher product pricing and higher commercial content. This project is expected to be launched in financial year 2018 (FY2018), but it would also depend on market conditions.

Management is sticking to its total launch target of RM721 million for FY2017 ending March 31, 2017, with RM706 million of new launches expected to be rolled out in the fourth quarter of FY2017 (4QFY2017). The projects with the highest GDV are Astetica Residences, a mixed development project (GDV of RM368 million), and the first phase of Meritus Residensi, also a mixed development project (GDV of RM220 million). Sales from both projects should also flow to FY2018.

Given the potential competition arising from PR1MA housing, we lower our TP to RM1.05, based on a higher 60% discount to revised net asset value (from 50%). Given the weaker earnings, there could be downside risks to dividend yield. Maintain “neutral”. — RHB Research Institute, Jan 19

This article first appeared in The Edge Financial Daily, on Jan 20, 2017. Subscribe to The Edge Financial Daily here.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.