Express Rail Link facing financial woes

AFTER operating for almost 15 years and now enjoying record-high passenger volumes, many would expect that KLIA Ekspres to be a commercially viable project that can stand on its own.

Unfortunately, that does not appear to be the case. Express Rail Link Sdn Bhd, KLIA Ekspres’ operator, is actually under financial stress and is looking for a way out.

Along with a 30-year extension that ERL is seeking from the government in lieu of RM2.9 billion in compensation owed to it, the company is also said to be restructuring about RM2.8 billion in debts owed to Bank Pembangunan Malaysia Bhd (BPMB).

Furthermore, sources tell The Edge ERL is seeking higher collection from the passenger service charge (PSC). Currently, ERL collects RM5 and RM1 from outbound international and domestic passengers respectively.

PSC collected from passengers in KLIA and klia 2 is shared between Malaysia Airports Holdings Bhd and the government based on a formula. ERL gets a share of the portion that the government receives.

In short, the extension of concession alone might not be enough for ERL to turn profitable. It will also need to defer the bulk of its debt payments while boosting its non-fare PSC income.

Note that YTL Corp Bhd owns a 45% stake in ERL and Lembaga Tabung Haji, 36%. SIPP Rail Sdn Bhd, which is linked to the Sultan of Johor, owns a 10% stake and the balance of 9% is held by Trisilco Equity Sdn Bhd.

Currently, the company is negotiating with the Public Private Partnership Unit under the Prime Minister’s Department to settle the RM2.9 billion it is claiming from the government for not being able to raise fares according to the concession agreement.

Meanwhile, filings with the Companies Commission of Malaysia in December 2016 show an increase in “liability secured under a charge” from RM940 million to RM4.08 billion by ERL.

The charge was originally lodged in late 1998 as a soft loan provided by the government to help ERL finance a portion of the RM2.4 billion cost to build the KLIA Ekspres.

Based on ERL’s financials as at June 2015, the outstanding debts owed to BPMB have ballooned to RM2.8 billion in total — RM1.071 billion under a “BPMB facility” and RM1.73 billion under a “repayment facility”.

ERL, which seems to be struggling to service its debts, has requested deferment of instalments for the Repayment Facility due on May 5, and Nov 5, 2015.BPMB agreed to the deferments.

While ERL’s FY2016 financials have not yet been lodged, sources familiar with the company say that some debt repayments were met during the financial year, reducing total borrowings to RM2.3 billion. To meet the obligations however, it is understood that additional capital had to be injected into the company.

But given ERL’s losses, this is not sustainable and repayments have to be deferred as part of a wider debt restructuring. ERL posted an after tax loss of RM4.07 million in FY2015.

This is the second time that ERL needs to restructure its debts. The BPMB and repayment facilities were both restructured in 2005, with the Finance Ministry’s approval, according to ERL’s financial statements.

The previous restructuring fixed the interest rate for both the facilities at zero — from January 1999 to January 2012 and from November 2002 to November 2015 respectively (see Table 1). The BPMB Facility was then subject to an interest rate of 13.01% per annum from January 2012 to January 2024. The Repayment Facility was subject to an interest rate of 11.3% per annum starting from November 2014 to November 2027.

Presently, additional deferment of the debt repayments is crucial for ERL if the company hopes to turn a profit. The 30-year extension will be meaningless if the repayments outpace the growth in operational profits.

Based on ERL’s liquidity risk analysis, the company would have to repay RM1.178 billion over two years (July 2015 to June 2017). In total, the terminal cash value of the debts would amount to RM3.57 billion based on the current repayment schedule.

While ERL is operationally profitable — making RM122.09 million in FY2015 — its earnings are grossly insufficient to meet its obligations.

At face value, it appears that the excessive debts may cause the downfall of the ERL project. However, this should not be the case given the relatively lenient interest and repayment terms of the debts thus far.

In fact, it is quite surprising that the ERL project is struggling financially at all.

After all, it services one of the top 10 busiest airports in Asia-Pacific, with over 51 million passengers a year. Besides, KLIA is far from the city centre — 67km by road — which increases the appeal of rail travel.

The addition of klia2 to the ERL’s line was also a huge windfall — it more than doubled ridership volumes to a record 11.03 million in 2015. The government even paid the RM100 million cost to connect klia2 to the KLIA Ekspres line in 2014.

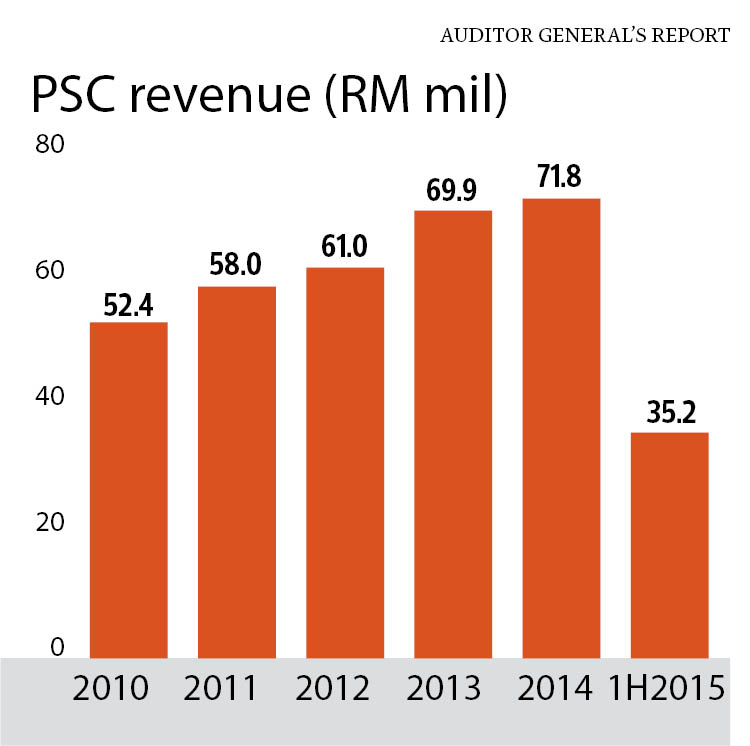

On top of that, ERL’s revenue is substantially boosted by the PSC collection. In FY2015, the RM70.9 million of PSC revenue collected made up 28.8% of the total revenue that year — RM246.2 million. Fare revenue was RM175.15 million.

Whopping RM2.9 bil claim

It could be argued that ERL is loss-making because it was not allowed to raise fares in line with the fare schedule under the original concession agreement. Consequently, it is claiming RM2.9 billion in compensation.

However, it could be argued that the ERL fare schedule is highly unrealistic. Based on it, fares for the express service should have been increased to RM41 in 2004, RM56 in 2009 and RM74 in 2014. By 2024, the fares would be a hefty RM126 for a single trip.

Instead, the fares were kept at RM35 for many years before being increased to RM55 a trip in late 2015. This hike, however, caused passenger volumes to fall for the first time, down 12% year on year to 9.7 million in 2016.

This is not entirely surprising given there are ample alternatives to the ERL. Services like Grab that can easily seat more than one passenger are offering airport rides for as low as RM65. Meanwhile, airport shuttle buses can be as cheap as RM17 for a one-way trip.

Based on the fare schedule, ERL would be charging RM74 for a one-way ride today. That would be about the same fare an airport taxi would charge to most areas in the Klang Valley. Clearly, the RM74 fare would not make commercial sense.

ERL is currently adding six more trains that will boost capacity by 50%. Hiking the fares further at this point would be counter-productive when more ridership is needed.

Thus, asking for higher PSC revenue makes more sense for ERL as it would not impact the rail’s ridership volumes.

Sources familiar with ERL however, point out that the PSC hike is unrelated to the compensation negotiations with the government.

But combined, the 30-year extension, higher PSC charges, and the debt restructuring will definitely serve ERL better than the original fare-hike schedule.

Meanwhile, the government is compelled to negotiate with ERL or be forced to pay the RM2.9 billion.

“Although the fare compensation calculations that were fixed in the concession agreement do not appear to be fair to the government, the attorney-general has advised that the formula that was set in the agreement is binding on the government,” reads the Auditor-General’s 2016 report.

“Alterations to the compensation formula can only be done with agreement from both parties,” notes the report.

In fairness, ERL was a greenfield project and the first of its kind. The government had to dangle a carrot for the private sector. At the very least, ERL operations have been running relatively smoothly over the years despite the growing financial challenges, which is more than can be said for other public-private partnership projects that needed government bailouts over the years.

But if the government hopes to secure a fairer deal going forward, ERL must strike a better balance between commercial viability and government support.

This article first appeared in The Edge Malaysia on Jan 23, 2017. Subscribe here for your personal copy.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.