Engineering, property units looking good for PPB

PPB Group Bhd (March 6, RM16.64)

Maintain market perform with an unchanged target price (TP) of RM17.60: We attended PPB Group Bhd’s fourth quarter of 2016 results briefing, which was well attended by around 50 people and came away maintaining our “neutral” short-term outlook for the group, though the engineering and property segments’ long-term outlook could improve.

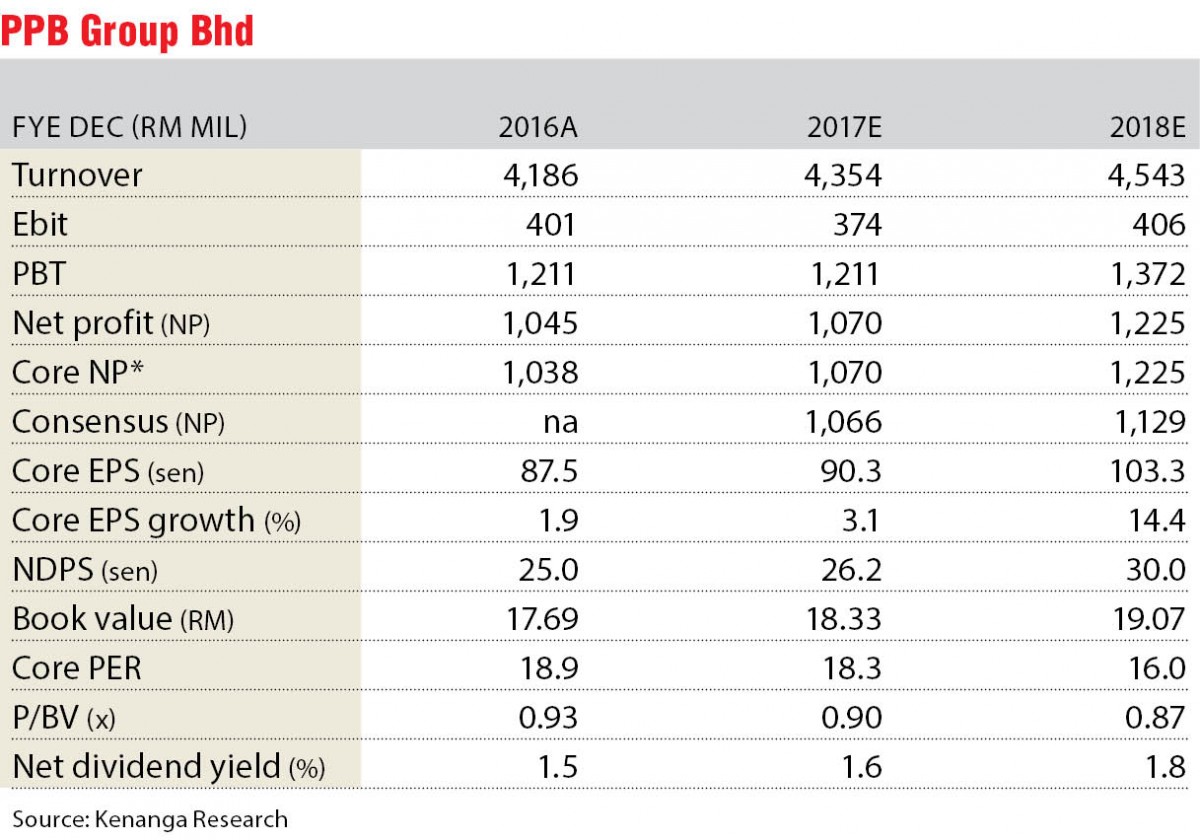

Maintain financial year 2017 (FY17) to FY18 core net profit (CNP) at RM1.07 billion to RM1.22 billion. No change to market perform call and TP of RM17.60.

In the grains and agribusiness (grains) segment, management noted that its Indonesian and Vietnamese subsidiaries recorded good volume improvement. Going forward, price outlook is relatively stable due to good global corn and wheat stock levels.

Costs should be slightly lower on switching to larger capacity vessels.

Meanwhile, the long-term growth prospect remains intact with Malaysian and Vietnamese mill expansions, in addition to a new collaboration with Brazilian poultry company BRF SA to provide finished-goods chicken products. We gather that the BRF joint venture will require minimal new investment as the existing plant has excess capacity for finished-goods production.

The film exhibition and distribution (film) segment should see top-line improvement with nine new locations scheduled for 2017.

In light of recent news reports regarding a sale of the film division, management said that while the company has received interest from international cinema chains for Golden Screen Cinemas, they are not in any sale negotiation and ruled out the possibility of an initial public offering.

The management added that the film division remains one of the company’s core businesses, which should see continued earnings growth over the next few years.

In the property segment, we understand that while sales for the Johor Southern Marina project remains relatively weak, management noted a recent pickup in inquiries, especially from foreign buyers.

Meanwhile, the company aims to launch its Taman Megah (Petaling Jaya) redevelopment project with a gross development value of RM500 million, which should improve segment sales in the next one to two years.

Other upcoming projects include the renovation of New World Park (Penang) and a link bridge to the upcoming mass rapid transit station at Cheras Leisure Mall (Kuala Lumpur).

The engineering segment saw some order book improvement (RM160 million as at end-2016, from RM132 million in mid-2016) with management more optimistic about its outlook as it is tendering for around RM600 million worth of water and sewerage projects.

Maintain FY17 to FY18 CNP at RM1.07 billion to RM1.22 billion as company updates are largely priced in our estimations. Reiterate market perform with unchanged TP of RM17.60 based on an unchanged forward price-earnings ratio (fwd PER) of 19.5 times applied to FY17 earnings per share of 90.3 sen. Our fwd PER of 19.5 times is based on a mean valuation basis. We remain “neutral” on PPB’s near-term outlook given the soft local consumer outlook.

With group earnings heavily contingent on its associate Wilmar’s performance, we expect the seasonally weaker first half of 2017 to result in subdued investor interest in PPB in the short term. — Kenanga Research, March 6

This article first appeared in The Edge Financial Daily, on March 7, 2017.

For more stories, download TheEdgeproperty.com pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.