Axis REIT 2Q core net earnings within expectations

Axis Real Estate Investment Trust (July 25, RM1.63)

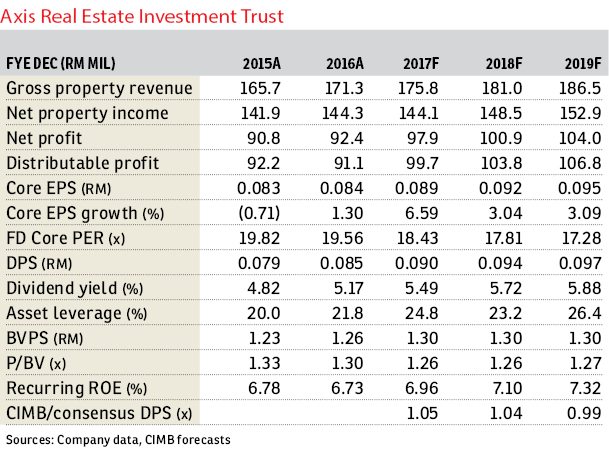

Maintain hold call with a target price of RM1.72: Axis Real Estate Investment Trust’s (Axis REIT) second quarter of financial year 2017 (2QFY17) core net earnings rose 2.4% year-on-year (y-o-y) to RM23.3 million, bringing first-half (1HFY17) core net earnings to RM46.3 million (up 2.2% y-o-y).

This was within both our and the Bloomberg consensus expectations, and accounted for 47% of both full-year forecasts. There were no revaluation gains/losses reported for 2QFY17.

The group declared a distribution per unit (DPU) of 2.17 sen for 2QFY17 (up 5.9% y-o-y), bringing 1HFY17 DPU to 4.3 sen (up 5.4% y-o-y), accounting for 48% of our full-year DPU forecast of nine sen.

The 2QFY17 DPU of 2.17 sen comprised 2.1 sen from operations and 0.07 sen from the final tranche of the realisation of unrealised income (recognition of prior years’ unrealised fair value gains on the market value of Axis Eureka as realised income upon its disposal).

1HFY17 revenue rose 1.6% y-o-y to RM84.3 million, on the back of positive portfolio rental reversions as well as additional contributions from the Scomi facility in Rawang (acquired in November 2016), which more than offset the loss of income from the Delfi Warehouse since the beginning of 2017. 1HFY17 core net earnings growth was further lifted by lower property and non-property expenses, which collectively declined 2.2% y-o-y to RM37.6 million.

Axis REIT also proposed the acquisition of two plots of leasehold land totalling 126.6 acres (51.23ha) in Gebeng, Pahang, for a total cash consideration of RM155 million. The property will be leased back to Wasco Coatings Malaysia Sdn Bhd on a 15-year lease, with a 10% step-up in rental rates every three years.

It will be fully funded by debt, and we estimate gearing to rise to 0.39 times post acquisition (0.34 times as at 2QFY17), well below the regulator’s prescribed gearing limit of 0.5 times, but above its internal gearing limit of 0.35 times.

The group expects a net yield of 7% for the Gebeng asset, which we deem as fair against its recent targeted acquisition yields of 7% to 8%. The property is within the MIEL Gebeng industrial estate in Kuantan, 4km from the Kuantan Port, a multi-cargo deep seaport located in the heartland of the petrochemical industry. We expect the acquisition to be neutral for earnings in FY17, but accretive to earnings from FY18.

Though we like the REIT’s healthy appetite for continuous asset injections, we think this has been priced in. A key upside risk to our call is further development of Phase 2 of the Axis Pre-Delivery and Inspection Centre, while a key downside risk is non-renewal of expiring leases of the Axis Steel Centre in FY17, which make up of 4.7% of the group’s total net lettable area. — CIMB Research, July 25

This article first appeared in The Edge Financial Daily, on July 26, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.