Niche office, prime mall segments to remain resilient in the long term

REIT sector

Maintain market weight: The sector’s core net earnings (excluding fair value gains) in the second quarter of financial year 2017 (2QFY17) improved by 7.4% year-on-year (y-o-y), mainly driven by strong y-o-y growth at MRCB-Quill REIT, which was largely due to acquisition of Menara Shell, and Sunway REIT, which partially offset the dent in sector net profit by Pavilion REIT. Excluding MRCB-Quill REIT, core earnings grew at a decent rate of 1.4% y-o-y versus 0.9% y-o-y in 1QFY17.

Pavilion Mall and Suria KLCC continued to see y-o-y declines in 2QFY17 due to major tenant relocation exercises. Tenants at Pavilion Mall have been gradually moving to Pavilion Elite since the third quarter of 2016 (3Q16) and the relocations should have been fully completed by 1H17. On the other hand, the development of a men’s and women’s luxury precinct on level 1 of Suria KLCC will only be completed by 4Q17.

We maintain our “market weight” call on the sector given the lack of compelling catalysts in the near term. We still believe that the oversupply of office malls and retail space is far from over. However, we think that the niche office building and prime retail mall segments will remain resilient in the long term.

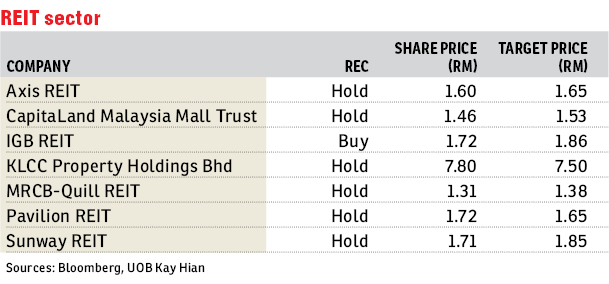

For exposure to retail REITs, we like IGB REIT as we believe it has the lowest earnings risk due to solid rental reversion and the highest retail sales, and an implied dividend yield of 5.2%. IGB REIT also posted resilient growth in 1H17 solely due to organic growth at Mid Valley Megamall and The Gardens Mall. It was also able to record a rental reversion of 5% during the quarter with tenant sales reported in the high single digits. Its sponsor’s asset — Mid Valley Southkey Megmall — is expected to be opened on Aug 18, 2018, but we gather that its acquisition will not take place in the near term.

We downgrade MRCB-Quill REIT from “buy” to “hold” given limited share price upside, following its share price increase. However, we still like the company for its built-to-suit strategy which allows it to lock in tenants for a longer period and shields it from the office oversupply issue. After the series of acquisitions by its sponsor (Platinum Sentral and Menara Shell from Malaysian Resources Corp Bhd), the next acquisition could be Menara Celcom in PJ Sentral which is slated for completion by end-2017. Hence, we expect the acquisition exercise to take place in 2018 and earnings contribution will only start in 2019. Although the acquisition resulted in improved earnings per unit, distribution per unit is, however, likely to remain flat in the near term due to the enlarged share base from a placement exercise and/or share swap exercise to fund the acquisition. — UOB KayHian Research, Sept 6

This article first appeared in The Edge Financial Daily, on Sept 7, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.