Is freehold always better than leasehold?

Many have debated whether freehold properties are better than leasehold ones, especially in terms of capital appreciation. The answer may simply lie in the entry price. Owing to their perpetual legal lifespan, freehold properties command a price premium over comparable leasehold properties. The question is what premium would be considered reasonable.

Based on the Singapore Land Authority’s leasehold table, freehold properties command premiums of around 4% to 10% over leasehold properties that have remaining leases of between 80 and 99 years. Actual transactions, however, suggest that paying premiums of up to 20% over comparable leasehold properties is reasonable.

Southaven I and Southaven II offer some clues. The projects are located next to each other on Hindhede Walk and were completed two years apart. However, Southaven I is on a 99-year leasehold site while Southaven II is on a 999-year leasehold site. This study shall treat 999-year leasehold as freehold.

The price gap between Southaven I and II was 8% in 1995, the earliest date when official data became available. That year, 39 units at Southaven I sold for S$634 (RM1,983) psf and 83 units at Southaven II sold for S$688 psf. The price gap widened to 20% by 2012 (see Chart 1a). As a result, prices appreciated around 27% at Southaven I to S$804 psf and 40% at Southaven II to S$962 psf during that period. Although the price gap fluctuated over time and hit 34% in 2005, the median stood at 20% between 1995 and 2012.

In Toa Payoh, the freehold Trellis Towers commanded an initial price premium of 19% in 1996 over the 99-year leasehold Oleander Towers. The price gap widened to as high as 44% in 2002 although it narrowed again to 23% in 2017, with a median price gap of 31% between 1996 and 2017. Prices appreciated 35% at Oleander Towers and 40% at Trellis Towers in that period (see Chart 1b).

Anecdotal evidence suggests that when the premium exceeds 30%, the capital appreciation for freehold properties could fall behind that for comparable leasehold properties. In 2006, freehold One Jervois commanded an initial price premium of 37% over the 99-year leasehold Domain 21 located nearby. A total of 205 units at One Jervois were sold in that year at an average price of S$1,004 psf compared with the S$731 psf fetched by 44 units at Domain 21. The premium fell over the years, with a median of 16% between 2006 and 2017. As a result, the capital appreciation for Domain 21 outperformed that of One Jervois during this period (see Chart 2a).

Similarly, prices at 99-year leasehold Amaryllis Ville rose faster than those at Newton 18, a freehold property located next door. In 2002, 59 units at Newton 18 changed hands at an average price of S$1,115 psf, or at a 31% premium to the 41 units sold at Amaryllis Ville, which went for S$854 psf. The premium also diminished over the years, resulting in a median of 21% between 2002 and 2016. In 2016, prices averaged S$1,737 psf at Newton 18 and S$1,434 psf at Amaryllis Ville, which translates into capital appreciations of 56% and 68%, respectively, since 2002 (see Chart 2b).

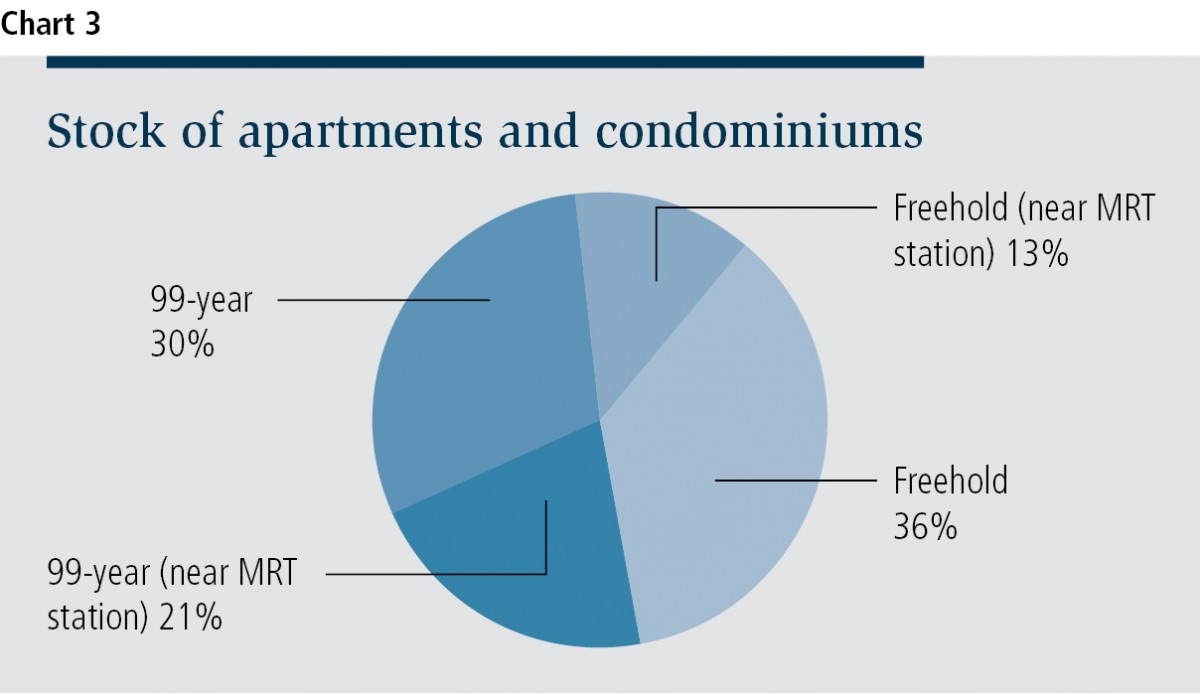

With an appropriate entry price, freehold properties offer several key advantages. For one, the government has ceased to offer freehold land parcels for sale. The scarcity factor will make freehold properties an attractive asset class for homebuyers. Currently, freehold properties account for about 49% of total apartment and condominium stock in Singapore, while leasehold properties make up the remainder. The proportion of freehold properties is set to decline as future launches will comprise mainly leasehold projects. Freehold apartments and condos located within walking distance of an MRT station are even more limited, accounting for just 13% of total stock island-wide (see Chart 3).

Certain foreign nationalities show a preference for freehold properties. Between January 2016 and August 2017, 71% of transactions were for leasehold properties and 29% for freehold ones. The proportion of freehold transactions, however, was higher among several key foreign purchasers, namely those from Indonesia (40%), the US (41%), the UK (50%), Australia (50%) and Hong Kong (34%). Interestingly, freehold properties accounted for 60% of purchases by companies.

Freehold properties are also said to have better en-bloc potential. A logistic regression analysis shows that tenure is not a statistically significant variable at the 5% level in determining the success of an en-bloc sale. It is, however, an economically significant variable with a large coefficient.

Finally, the risk of owning a leasehold property becomes significant as the remainder lease runs low. To finance a property using the Central Provident Fund, the sum of the remaining lease and the age of the buyer must be at least 80 years. For properties with remaining leases of between 30 and 60 years, a valuation limit will apply on the amount of CPF contribution that can be used to finance the property. The financing restriction would shrink the pool of potential buyers for ageing leasehold properties. Meanwhile, en bloc is not a guaranteed option for leasehold properties and there is a possibility that the land will return to the state at the end of a lease.

On the flip side, the rental market does not differentiate between the types of tenure of the property. Leasehold properties offer higher rental yields over comparable freehold properties, owing to their discounted prices. The higher yields serve to compensate for their depreciating tenure, higher risks and shorter lifespan to recoup the owner’s capital outlay.

This article first appeared in The Edge Property Singapore, a pullout of The Edge Singapore, on Sept 11, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.