UOA Development lines up RM1.37b worth of new launches for FY18

UOA Development Bhd (Feb 22, RM2.57)

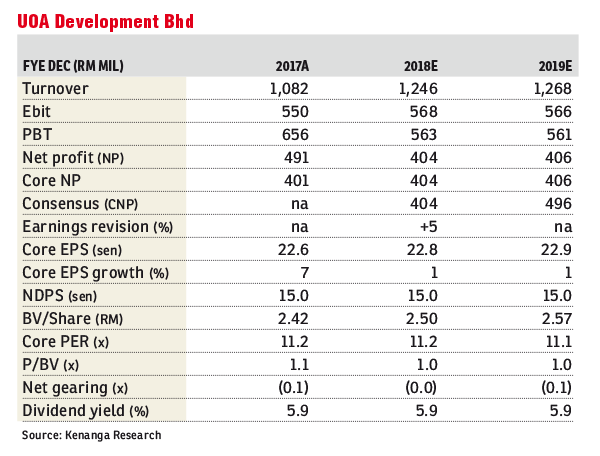

Maintain market perform with a target price (TP) of RM2.50: UOA Development Bhd’s financial year 2017 (FY17) core net profit (CNP) of RM401 million was within expectations at 104% of the street’s full-year estimate and 105% of ours — CNP calculation excludes RM90 million one-off remeasurement gain upon acquiring an additional 35% in UOA Business Park. The group secured sales of RM1.3 billion (-12% year-on-year [y-o-y]) which were in line at 104% of our forecast of RM1.25 billion. Key sales drivers were Sentul Point and United Point which drove 71% of sales. The proposed first and final single-tier dividend of 15 sen was spot-on with our estimates.

Quarter-on-quarter (q-o-q), fourth quarter of FY17 (4QFY17) CNP rose by 13% largely due to a surge in other operating income (comprising mainly hospitality/rental income), with the segment’s contribution rising by 58%.

Y-o-y, FY17 CNP was up by 7% in tandem with higher billings, stable development margins and improving recurring income streams. The group remains in a net cash position (0.07 times).

For FY18, UOA Development has lined up RM1.37 billion worth of new launches for sale. The company does not provide official sales target guidance but based on its new launches and inventories/WIPs, we expect a flattish sales growth trajectory.

The group’s inventories have hit a record high of RM1 billion (at cost) — but we estimate a market value of about RM2 billion.

While this may be alarming, UOA Development has very strong holding power and has demonstrated its ability to realise its inventories at the “right time”.

Note that we only expect Southbank Phase II and Danau Kota to be completed this year, while the group will focus on realising its inventories — so group margins may not be as strong as that of FY17.

Notably, there is more emphasis on recurring income.

Over 2018, the group plans to commence works on Bandar Tun Razak, Cheras (age-care facilities; RM300 million gross development value [GDV]) and South Point, Bangsar South (RM220 million GDV) but is likely to keep them for recurring income purposes.

UOA Development investment properties in the books are at RM1.67 billion and rental income streams make up close to 40% of the group’s earnings before interest and tax.

We reiterate “market perform” with an unchanged TP of RM2.50 based on a 40% discount (+0.5SD levels) to its fixed deposit revalued net asset valuation of RM4.20.

We think our valuation level is fair considering its attributes, such as high margins, a net cash position, a more prominent recurring income stream from its hospitality and property investment assets, and a dividend yield of 5.9% which is already almost on a par with the sizeable Malaysian real estate investment trusts’ average dividend yield of 5.8%.

Although we recommend “market perform”, we believe this may be a “flight to safety” stock considering its defensive qualities.

Risks include weaker/stronger-than-expected property sales, margin fluctuations, and changes in real estate policies and/or lending environments. — Kenanga Research, Feb 22

This article first appeared in The Edge Financial Daily, on Feb 23, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.