Pavilion REIT expected to see subdued rental reversion growth

Pavilion Real Estate Investment Trust (March 15, RM1.42)

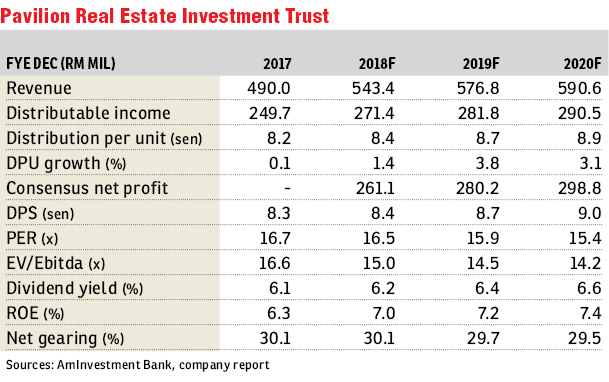

Maintain hold with a lower fair value (FV) of RM1.53: We maintain our “hold” call on Pavilion Real Estate Investment Trust (REIT) with a lower FV of RM1.53 from RM1.87 based on a forward target yield of 5.5% versus 4.7% previously. The downward FV revision is in line with the rising interest rate environment, matching investors’ demand for higher yields. We have revised our earnings forecast downwards by 3% and 5% for financial year 2018 forecast (FY18F) and FY19F based on the expectation of minimal growth on rental reversions from various properties and taking into account that the injection of Pavilion Elite is reflected only after the first half of FY18.

We expect Pavilion Kuala Lumpur as well as Intermark Mall to continue maintaining high occupancy rates at 99% and 90% respectively with marginal growth on rental reversions and minimal leases expiring in FY18 (14% and 20% respectively). Likewise, Pavilion Tower, which has 37% of leases expiring in 2018, is expected to retain all tenants, maintaining close to full occupancy. The successful tenant reversion at Pavilion Tower may however be at the expense of positive rental reversions as maintaining high occupancy remains the priority.

Da Men Mall continues to lag behind in terms of occupancy rates at 86%. The management is currently evaluating the tenant mix for Da Men to increase footfall. Additionally, rebates may be offered to assist underperforming tenants and encourage higher occupancy rates, especially with 51% of leases expiring in 2018.

Pavilion REIT’s gearing level is low at 0.26 times, with 80% of it being floating rate borrowings. However, management has guided that while interest rates are rising, existing floating remains more favourable as compared to locking in fixed rates previously. Hence, we expect minimal impact from the potential interest rate hikes on Pavilion REIT’s earnings for FY18F to FY19F. At the same time, the low gearing level indicates room for future acquisitions, particularly since Pavilion REIT has the right of first refusal for properties such as Fahrenheit88 in Bukit Bintang, subject only to the owner’s intention to sell.

Overall, Pavilion REIT’s debt maturity looks concentrated with RM733 million maturing in 2019 and another RM736 million in 2021. Management has advised that the 2019 maturities will be refinanced to smoothen the repayment profile. — AmInvestment Bank, March 15

This article first appeared in The Edge Financial Daily, on March 16, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.