UEM Sunrise’s proposed land buy expected to raise GDV

UEM Sunrise Bhd (April 16, 94.5 sen)

Maintain hold with a target price (TP) of RM1.20: UEM Sunrise Bhd (UEMS) proposed acquisitions of 72.73 acres (29.4ha) of leasehold land in Kepong via share subscription of (50%+1) in Mega Legacy Sdn Bhd (MLM) for RM279.3 million. MLM will develop a mixed residential and commercial development on the land with an estimated gross development value (GDV) of RM15 billion over the next 15 years. The maiden launch is targeted for FY19. The acquisitions will be funded via internal generated funds.

We are positive on the proposal as it is expected to increase the group’s effective GDV by 6.9% to around RM117 billion. Assuming an earnings before interest and tax (EBIT) margin of 14%, the project’s net present value (NPV) is estimated at RM112.7 million or revalued net asset valuation (RNAV) of three sen per share (0.9% of our TP). Note that UEMS will consolidate the results of MLM given that it owns a controlling stake. Net gearing may inch up to 0.52 times from the current level of 0.48 times.

The implied land cost to UEMS is around RM88.2 per square foot (psf) and is very competitive at only 3.7% of the estimated GDV. However, it does not include the construction cost of the two interchanges connecting to MRR2 as stiputed in the development order. The allowable plot ratio on the land is 1:6.

The land is located adjacent to the Kepong Metropolitan Park, approximately 13km north west of Kuala Lumpur.

They are currently accessible via Jalan Kepong and two new interchanges will be constructed directly to MRR2 with the first interchange to be completed within 18 months from the first launch.

In line with group strategy, the acquisition bolds well with the strategy of the company to increase its presence in the Klang Valley. Given the strategic location and size of the land along with UEMS’ track record in Mont Kiara, we believe the development should contribute positively to the group in the future.

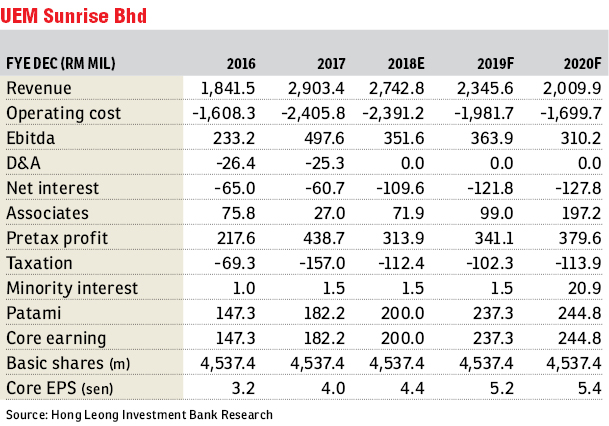

We impute the contribution from the above development (expected from FY20 onwards) and introduce our FY20 forecast. We also take the opportunity to revisit our forecast assumptions (take-up rates and launches) and lower our FY18E and FY19F earnings forecast by 8% and 25.4%.

TP is raised to RM1.20 (from RM1.18) after taking into account the new land bank and estimated GDV from the above. Our TP is based on unchanged 60% discount to RNAV of RM2.99. Despite trading at a steep discount to its RNAV and significant upside to our target price, we see lack of near term catalyst given the subdued sentiment for property outlook in Johor. — Hong Leong Investment Bank Research, April 16

This article first appeared in The Edge Financial Daily, on April 17, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.