YTL Corp’s ability to meet its order book target in the near term in doubt

TL Corp Bhd (May 14, RM1.16)

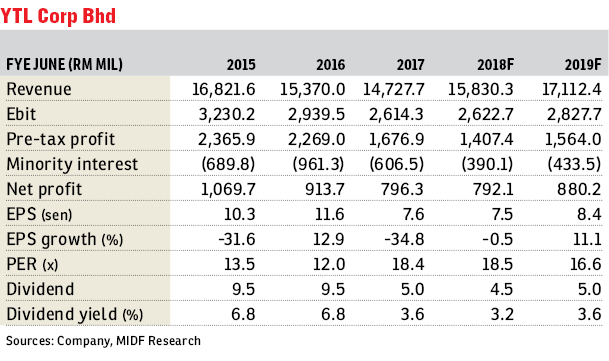

Downgrade to neutral with a lower target price (TP) of RM1.30: Our earlier “buy” thesis on YTL Corp Bhd was premised on a revival of its construction unit with management targeting order book to swell to some RM12 billion (from about RM400 million at end of calendar year 2017 [CY17]), driven mainly by rail-related contracts. However, the new Pakatan Harapan government is expected to review all megaprojects in the construction sector, particularly those awarded to China-based contractors. This raises uncertainty over YTL Corp’s ability to hit its order book target in the near term and derails our earlier thesis. Cement earnings are also likely to be impacted negatively from a review of major construction contracts.

To recap, YTL Corp’s construction order book was expected to expand significantly by end-CY18. From about RM400 million (comprising mainly internal property development projects, for example, YTL Corp’s new Pavilion headquarters), order book was expected to expand to some RM12 billion by year end. Key drivers for this are the RM9.4 billion Gemas-JB double-tracking project over the next four years, project delivery partner role for the Kuala Lumpur-Singapore high-speed rail project, construction of 80%-owned Tanjung Jati coal power plant in Indonesia over the next three years — US$1 billion (RM3.95 billion) of the project’s US$2.7 billion project value comprising construction. The Gemas-JB double-tracking project was awarded to a consortium of Chinese companies comprising China Railway Construction Corp Ltd, China Communications Construction Co Ltd, and Congressional-Executive Commission on China in 2016.

We downgrade our financial year 2018 (FY18) and FY19 earnings estimates by 3% and 13% respectively as we now exclude contribution from the Gemas-JB double-tracking project. Cement earnings are also tuned down as earnings will be indirectly impacted by a potential delay or slowdown in progress of major construction projects from the expected review.

We downgrade YTL Corp to “neutral” from “buy” and lower our TP to RM1.30 from RM1.82 following the earnings downgrade and after imputing a larger discount to our sum-of-the-parts-based valuation to reflect the higher earnings risk in the near term. — MIDF Research, May 14

This article first appeared in The Edge Financial Daily, on May 15, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.