Sunway REIT seen resilient amid challenges

Sunway Real Estate Investment Trust (July 5, RM1.70)

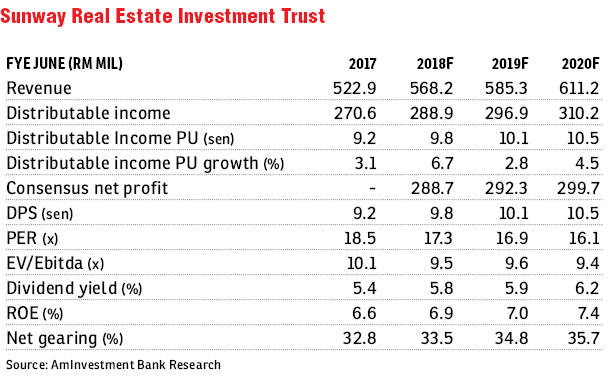

Maintain hold with a lower fair value of RM1.68: We maintain our “hold” recommendation on Sunway Real Estate Investment Trust (SunREIT) with a lower fair value of RM1.68 (from RM1.70 previously) based on a forward target yield of 6%, following our earnings revision.

We are revising our financial year ending June 30, 2018 (FY18) till FY20 earnings downwards by 3.4%, 6.0% and 2.0% to RM288.9 million, RM296.9million and RM310.2million respectively with minor tweaks in operating expenses; and the refurbishment of Sunway Resort Hotel and Spa, which will impact its hospitality revenue mainly in FY19 and FY20. The refurbishment will be completed in 2020.

Occupancy rates at Sunway Pyramid, Carnival and Putra Mall have remained stable at 99%, 97% and 90% respectively. Both Sunway Pyramid and Carnival have captive markets surrounded by mature townships, making them the leading malls in their locality, with a wide array of retailers.

Meanwhile, SunCity Ipoh Hypermarket is leased to a single tenant, a major hypermarket and retailer chain operating under the Giant brand.

Following the refurbishment of Putra Mall in 2013 till 2015, occupancy rate has been on an uptrend, growing from 60% (before refurbishment) to 90.5% presently. At the same time, it provides rental rebates to encourage both tenant retention and new occupancy.

The hotel segment remains stable as all assets are currently on 10-year master leases. The refurbishment of Sunway Pyramid Hotel was completed in June 2017; hence we expect full-year contribution from FY18. Meanwhile the latest acquisition, Sunway Clio Property, has started contributing in third quarter (3QFY18).

SunREIT is still predominantly a retail REIT with about 70% contribution from its retail assets, and the balance from hotels (about 20%), offices, hospitals and industrial assets (10%).

Overall, we are “neutral” on the REIT sector over the next 12 months. Prospects for the sector are expected to be subdued, especially with potential overnight policy rate hikes in 2018, as well as muted rental reversion opportunities affected partly by the oversupply of retail and office spaces. However, we believe that SunREIT will fare slightly better. — AmInvestment Bank, July 5

This article first appeared in The Edge Financial Daily, on July 6, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.