MBSB 3Q, 4Q results seen to reflect loan loss provisions

Malaysia Building Society Bhd (July 31, RM1.12)

Maintain hold with a lower fair value (FV) of RM1.27: Malaysia Building Society Bhd’s (MBSB) net profit for the second quarter of financial year 2018 (2QFY18) fell 71.8% quarter-on-quarter (q-o-q) due to a charge in impairment allowances for loans of RM124 milliion compared to a net write-back in provisions of RM154 million in 1QFY18, and higher operating expenses (Opex) from integration cost and amortisation of information technology (IT) investments.

Net profit for the first half of financial year 2018 (1HFY18) rose to RM402 million (+109.2% year-on-year [y-o-y]), largely due to a write-back in provision for loan impairment in 1QFY18. Recall that in 1QFY18, the write-back was a result of the group lowering its probability of default (PD) and loss given default (LGD) estimates as well as reducing the provisions required for corporate loans where settlements have been made, consequently resulting in the cancellation of undrawn portion of credit facilities.

1HFY18 earnings were ahead of expectations, accounting for 59.3% of our and 63.9% of consensus estimates. The variance was due to the net write-back of loan impairment from the 1QFY18. Despite this, we are not raising our earnings as the 1QFY18 net write-back in loan impairment is not expected to recur. We expect the subsequent 3QFY18 and 4QFY18 results to reflect provisions in loan losses. We estimate the full FY18 credit cost to be 0.7%.

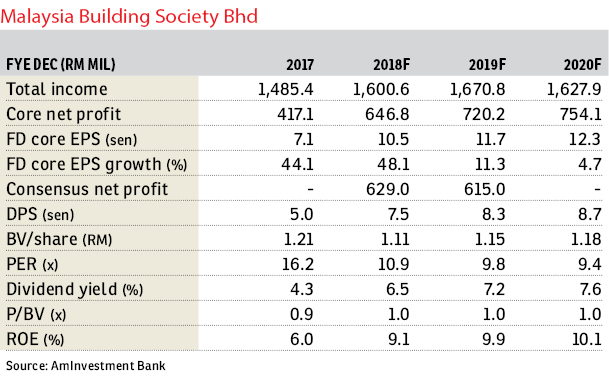

Total income declined by 3.6% y-o-y due to lower net interest income from the termination of conventional business coupled with a drop in Islamic banking income.

2QFY18 saw a credit cost of 1.4% versus -1.8% in 1QFY18. This was due to changes in the credit quality of certain retail and corporate loans from stages one to two and three. We understand that this was partly contributed by the pass due payments from borrowers which were more than 30 days as a result of the festive season. For 1HFY18, credit cost was -0.2% versus 1.8% in 1HFY17.

Gross impaired loan ratio continued to trend higher to 5.5% in 2QFY18 from 4.8% in the preceding quarter. This has resulted in the drop in the group’s loan loss cover to 128.3% in 2QFY18 from 133.3% in 1QFY18.

Gross loan growth remained modest at 1.2% q-o-q with the contraction in personal financing while mortgage financing expanded slightly by 0.6% q-o-q and corporate loans grew 6.3% q-o-q. — AmInvestment Bank, July 31

This article first appeared in The Edge Financial Daily, on Aug 1, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.