Pestech earnings growth story seen as positive

Pestech International Bhd (Oct 10, RM1.42)

Maintain outperform with an unchanged target price (TP) of RM1.95: Pestech International Bhd announced on Tuesday that the Ansaldo STS Pestech Consortium, an unincorporated consortium between Pestech’s wholly-owned subsidiary Pestech Technology Sdn Bhd and Ansaldo STS Malaysia Sdn Bhd, had accepted a letter of award from Syarikat Pembinaan Yeoh Tiong Lay Sdn Bhd, under the SIPP-YTL joint venture for the turnkey EPC (engineering, procurement and construction) relating to the signalling system for the Gemas-Johor Bahru electrification double-track at a fixed subcontract price of RM339 million. The project will be completed by April 1, 2021.

The total subcontract value for Pestech’s portion of work is RM75 million, totalling its contract value win from the double-track project to RM474 million after it earlier secured the EPC and maintenance of the electrification system worth RM399 million in end-September. This is definitely positive for Pestech as it has further built up its local participation for the signalling portion of the rail electrification and is a good future reference in bidding for projects both locally as well as regionally.

This is the third contract Pestech has secured in financial year 2019 (FY19), totalling RM532 million and bringing the total current order book to RM2.1 billion, which will keep it busy until 2021. With the East Coast Rail Link and Kuala Lumpur-Singapore high speed rail projects still uncertain at the moment and the Klang Valley Double Track 2 to be retendered, Pestech’s focus will switch back to the region for the transmission line, substation and underground cable projects.

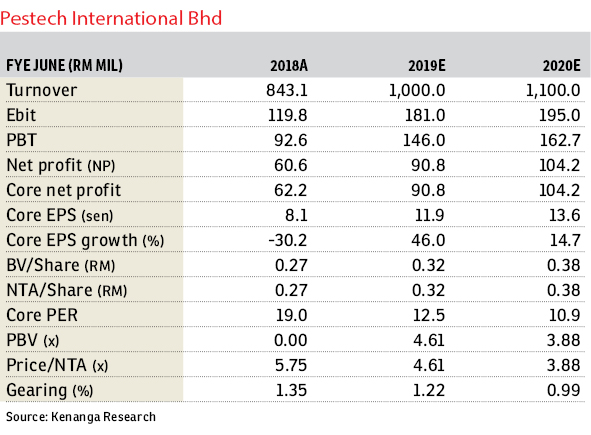

We keep our FY19 to FY20 estimates unchanged for now despite this new contract win as it is still within our contract win assumptions. We continue to like this niche utility infrastructure play for its earnings growth story. In fact, its valuation is no longer excessive following the lacklustre share price performance in the past two years while earnings momentum remains strong. Hence, with undemanding valuation at 11 times FY20 price-earnings ratio, we maintain our “outperform” rating with an unchanged TP of RM1.95. Risks to our call include failure to replenish its order book and cost overruns. — Kenanga Research, Oct 10

This article first appeared in The Edge Financial Daily, on Oct 11, 2018.

Click here for more property stories.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.