Taking a loan to renovate homes: A BAD IDEA?

Mr and Mrs B who were shopping for a 2-storey house in Kuala Lumpur narrowed their choices down to two units located just next to each other in an established housing estate.

The first unit was newly and extravagantly renovated. In contrast, the second was only renovated in moderation.

Ironically, the first unit was priced at 10% less than the other, yet, the couple had no qualms opting for the latter.

“I did not like the major renovations in the first unit that we visited. My husband and I knew we would need to spend substantially to hack down the renovations [in the first unit], cart away the debris and make good the place.

“On the other hand, although the second unit had less renovations done, we liked what we saw.

“Ultimately, I guess it is about taste and practicality. The lesson I have learnt here is to never assume that what we spend on renovating our property will enhance its value,” adds Mrs B.

Association of Valuers, Property Managers, Estate Agents and Property Consultants in the Private Sector Malaysia (PEPS) president Michael Kong Kok Kee says it is a common assumption among homeowners that the value of a property will rise in tandem with the cost of renovations.

“From a valuation point of view, fancy decorations or fittings will add little to the value [of the property]. Valuers will not take the full amount of the renovations into consideration. The simple fact of the matter is that [most home renovations] are a matter of personal preference.

“Valuers consider the market value — something which the market accepts as being tangible and practical. Take enlarging the living space of a home for instance, which is an acceptable form of renovation, compared to fancy fittings such as fountains,” explains Kong.

He adds that renovations must also comply with building by-laws, or else they will not be factored into the valuation.

Taking out a loan for home renovations — yes or no?

So, is taking out a loan to renovate our homes a good idea? President-elect of the Malaysian Institute of Estate Agents (MIEA) Lim Boon Ping discourages the practice. He believes that one should spend within one’s means.

“Your first house is never your dream house. For first-time buyers, opt for something affordable.

A few years later, you either sell or upgrade. I definitely do not encourage people to borrow money [for renovations],” stresses Lim.

He also reckons that home renovations are rather popular at present. “People have expectations — especially young people. The younger generation tends to fork out more on renovations. This could be due to peer pressure. It is quite common for first-time [home]buyers to spend about RM50,000 to RM100,000 on home renovations,” notes Lim.

Mortgage specialist Vincent Ching, who is the head of marketing for Ideal Mortgage Specialist Sdn Bhd opines that for personal financing, the banks do not restrict the actual use of the approved loans.

“The reason for the loan is mostly for [personal] consumption, which means borrowers are free to use the funds for whatever reason, and this includes home renovations,” says Ching.

Both Ching and Lim have seen their fair share of borrowers running into financial difficulties.

“I have seen people getting into financial trouble due to overspending on home renovations. I believe some of the reasons are due to the lack of planning, over-budgeting and engaging the wrong contractor.

“Some people might just rely on the interior designer or main contractor for the renovation of the house, who will usually delegate the work to subcontractors. If they [homeowners] are able to directly get the right person for the job, for example, getting an electrician yourself instead of relying on the contractor, this could save you some money,” explains Ching.

Meanwhile, Lim claims to have come across quite a few abandoned renovation projects, be it for interior or external (structural) renovations.

He agrees that “renovation cost does not equate to value”.

“Putting in RM100,000 will not net you returns of RM100,000 for your property,” he stresses.

To this, Ching adds: “This is not how you do the math when it comes to valuation. It is a very subjective matter. Some valuers may consider structural fittings as added value [to the property] but may disregard certain interior renovations.”

Lim advises people to be practical and not overspend on luxuries. “What is fashionable and trendy now may not be so years later,” he says.

Why borrow?

However, there are some people who feel that taking on a loan for home renovations is justified. Patrick Chin, a banker in his early 30s tells EdgeProp.my his rationale for taking out a loan to renovate his home.

“Ideally, I would not wish to take up a loan for this purpose as I do not like the idea of being in debt. However, as this will be a major renovation which will involve a significant sum of money and with marriage plans looming, I feel taking a loan is the most sensible choice.

“As long as the monthly instalment amount is comfortable, I believe taking a loan will greatly help to free up my finances for other equally important uses,” says Chin.

He adds that his home has never been renovated since he bought it as a sub-sale back in 2012. “I consider it a good time now to welcome a fresh home makeover in order to bring back a sense of newness,” says Chin.

He says he has no difficulty making repayments. “As long as you plan the right amount to borrow, the monthly instalment amount should be comfortable enough for repayment. Therefore, there is no [significant] change in my lifestyle.”

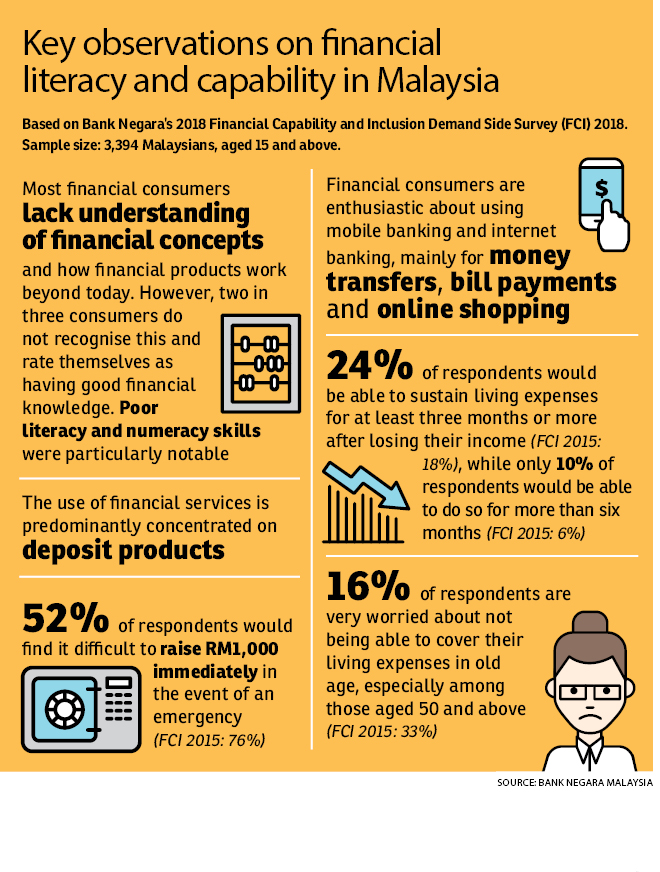

Ultimately, Bank Negara Malaysia notes that it boils down to being financially prudent. “Most financial consumers lack understanding of financial concepts and how financial products work beyond today. However, two in three consumers do not recognise this and rate themselves as having good financial knowledge. Poor literacy and numeracy skills were particularly notable,” the central bank states in their report.

Ching dishes out some advice for homeowners (especially first-time buyers): “I would

advise them to start planning for the renovation cost even before they purchase the property.

Start by surveying and researching and getting quotations from various contractors for comparison, in order to know what to expect financially.

“I believe renovation spending should be limited to 10% to 20% of the purchase price. One thing to avoid is buying fancy furniture and fittings. Focus on suitability and sustainability of the items,” says Ching.

Bank Negara: Bulk of personal financing utilised for home renovations

A high number of defaults in personal financing continues to be observed among borrowers who earn less than RM5,000 per month (the lower-income group) and among urbanites who have to deal with higher costs of living.

According to Bank Negara Malaysia’s Risk Developments and Assessment of Financial Stability in 2018 report, about half of outstanding personal loan borrowings are from the lower-income group. The share of personal financing to total borrowings in the lower-income group stood at 26.6%, almost double that of the average borrower (14.5%).

Bank Negara has observed that personal financing is used mainly for consumption purposes. More than one-third is for discretionary consumption expenditure to support lifestyle choices, which included the purchase of durable goods and expenses for weddings and festive seasons. This is similarly observed among distressed borrowers, which points to persisting behavior of spending beyond one’s means, said the central bank in the report.

Also, close to half of personal financing was taken to accumulate assets, mainly to make down payments for house purchases and for business purposes. Notably, among distressed borrowers, personal finance borrowings included a significant share utilised for home renovations.

“Given that the appreciation of home values from such an expenditure may not always correspond to amounts spent on renovation, highly-leveraged borrowers may find themselves in a negative equity position with debt burdens they cannot afford,” the report states.

This story first appeared in the EdgeProp.my pullout on May 17, 2019. You can access back issues here.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.