Gamuda’s 1Q results within expectations

Gamuda Bhd (Dec 16, RM3.89)

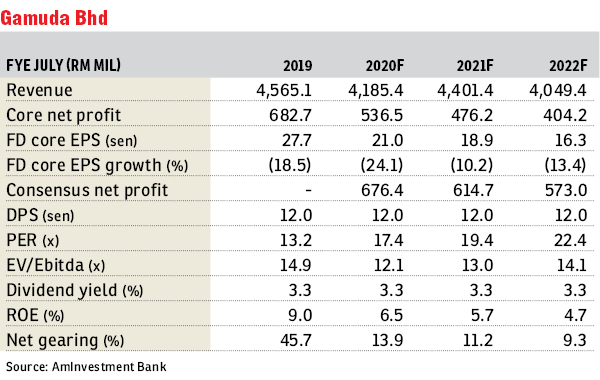

Maintain underweight with an unchanged fair value of RM2.84: Gamuda Bhd’s first quarter of financial year 2020 (1QFY20) results came in at 32% and 26% for our full-year forecast and the full-year consensus estimates. However, we consider the results within expectations as we expect a weaker second half (2H) in the absence of toll road profits assuming the disposal is to be completed by then.

Its 1QFY20 core net profit only grew 1% year-on-year, as better showing from property (strong sales and firm margins in Vietnam) was offset by weaker performance from construction (the downsized Mass Rapid Transit Line 2 [MRT2] contract) and concessions (the absence of contribution from Syarikat Pengeluar Air Sungai Selangor Sdn Bhd [Splash] following its disposal).

Gamuda recorded only RM500 million property sales in 1QFY20, with overseas projects (largely in Vietnam) contributing about 60% of the total with the balance coming from its local township projects comprising largely Gamuda Gardens (near Rawang), Gamuda Cove (near Nilai) and twentyfive.7 (near Kota Kemuning). It is reviewing its FY20 property sales target of RM4 billion for a possible downward revision, largely due to the soft local property market.

Gamuda is hopeful that the “definitive agreements” pertaining to the disposal of its equity in various toll roads to the government for RM2.36 billion will be signed in January 2020, paving the way for extraordinary general meetings in March 2020 and completion of the deal in April/May 2020.

This is conditional upon the deal being consistent with the government’s policy framework with regard to the toll road ownership in Malaysia. The government is at present still trying to decide if it should own toll roads. If the government decides to sell the North-South Expressway (partly owned by Khazanah Nasional Bhd) to the private sector, it then does not make sense for the government to take over Gamuda toll roads.

For the Penang Transport Master Plan (PTMP) project, Gamuda reiterated its guidance for physical work to start in 2H of 2020. It is working on the basis that the Penang state government has secured federal government guarantee to issue “Light Rail Transit (LRT) bonds” (a statement made by Penang Chief Minister Chow Kon Yeow recently). Gamuda also reiterated that it is providing “assistance” to the Penang state government to secure funding for the Penang South Reclamation (PSR) project (the reclamation of three man-made islands with a total area of 4,200 acres [1699.68ha] at the southern tip of Penang Island).

For a start, about RM3.5–RM4 billion funding is required to finance the reclamation of the 790-acre Smart Industrial Park on the 2,300-acre Island A. Once completed, the industrial park will be sold and the cash flow and profit will be ploughed back to fund the LRT, Pan Island Link highway and further reclamation works under the PSR project.

Gamuda, via a 45%-owned entity, has won an open tender from the Land Transport Authority of Singapore for the construction of a bus depot worth S$260 million (RM794.89 million) in Singapore. While Gamuda’s share of works is worth about RM400 million, we understand that the expected profits are marginal given the highly competitive nature of public works in Singapore.

We remain cautious about the outlook for the local construction sector. Given the still elevated national debt, we believe the government has very limited room for fiscal manoeuvre which means that it is unlikely to roll out new public infrastructure projects in a major way over the short term, including the MRT Line 3 project.

Zooming in on Gamuda, we sense high “concentration risk” in the PTMP project in the event the project fails to get off the ground timely (2H of 2020 as guided) or Gamuda being given a reduced role in the project (as the project delivery partner [PDP] model is no longer favoured by the federal government as manifested in the cancellation of the PDP model in the construction of LRT Line 3, MRT2 and Pan Borneo Highway Sarawak). We are also mindful of the potential hefty initial “school fees” Gamuda may have to pay in order to gain a foothold in the Australian construction market. — AmInvestment Bank, Dec 16

This article first appeared in The Edge Financial Daily, on Dec 17, 2019.

Click here for more property stories.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.