Industrialisation 4.0: How Malaysia is re-engineering its manufacturing future

This article first appeared in the Industrial Special Report in November 2025.

For much of the last five decades, Malaysia grew by offering something very simple: land, affordable labour, and convenient access to global ports. Shah Alam in Selangor, and Bayan Lepas in Penang became the shorthand for industrial success. It worked well enough. Manufacturers came, set up assembly lines, exported at scale, and helped build the middle class.

The current environment, however, is far less forgiving. Supply chains are being redrawn. Semiconductors, new-energy vehicles, and digital infrastructure have become the new magnets of investment. For Malaysia, the old formula is being rewritten to align with strategic new priorities.

EdgeProp speaks to real estate, industrial and logistics development, and funds management advisory AREA Group chairman Datuk Stewart LaBrooy to find out more.

The veteran, decades in the industry, asserts: “We have to stop selling land as the core product. The winning model is to offer a complete operating environment”.

This view reflects a broader pattern. Industrial development is no longer simply about real estate. It behaves more like critical infrastructure that underpins national competitiveness, particularly in advanced electronics and data processing.

How we got here

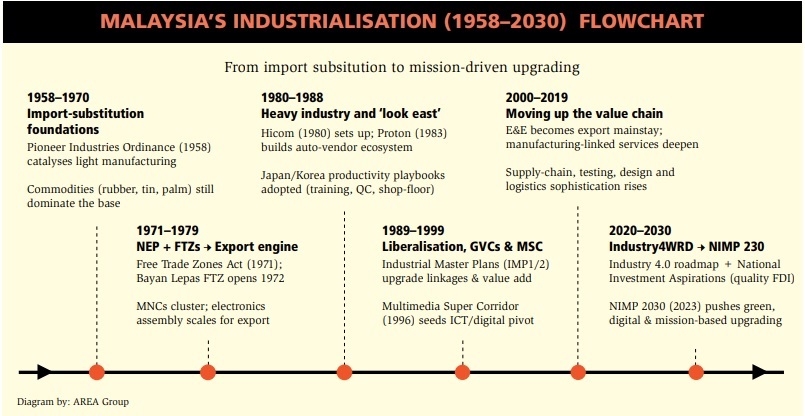

Malaysia’s industrial journey has not been linear. It began with import substitution in the 1960s before pivoting to export-led manufacturing in the 1970s.

The Free Trade Zones Act, which created sites like Bayan Lepas, Penang, brought multinational electronics firms, and hardened export discipline. The 1980s added depth when the national car programme pushed heavy manufacturing, and a transfer of shop-floor know-how from Japan, and Korea.

The next decade moved deeper into global value chains, and with the Multimedia Super Corridor, began a tentative digital turn. Later, however, China’s rapid rise pulled much of the low-end manufacturing away, prompting Malaysia to search for a new role.

Streamlined policies enacted in the 90s raised foreign direct investment levels for a while until the Asian financial crisis of 1997, he recalls.

In the wake of the crisis, electrical and electronics (E&E) emerged as an export mainstay, with integrated design, testing and logistics services raising the overall market value proposition.

Since the 2010s, though, industrial development has become more sophisticated. Professionalised logistics and e-commerce real estate investment trusts (REITs) spearheaded higher-spec warehouses that could handle volume, and automation.

More recently, the past three years have brought another turning point. Malaysia’s industrial focus is now shaped by geopolitics, sustainability, advanced manufacturing, and the rapid expansion of data-driven industries.

From parcels and premises to systems and structures

Modern industrial investment favours places that operate as functioning systems rather than loose collections of factories.

This new model relies on several essen tials such as reliable utilities, connectivity, a supply of trained workers, and a clear plan for future capacity.

LaBrooy describes this shift as a change from plots to ecosystems.

“It’s not just about providing land; we need to create integrated, intelligent ecosystems that attract long-term industrial leadership in the region.

“Execution excellence means you stop handing over empty shells. You deliver a full environment that can operate from day one,” he adds.

One lesson came from the early growth of logistics. Developers who built certified facilities with guaranteed utilities soon re alised they were attracting multinationals which valued certainty above all. An example was Malaysia’s first multi-storey free-trade warehouse, AREA Logistics @ Ampang, Selangor by AREA Group. Completed in 2019, it was the first of its kind to have a 3-level ramp that caters up to 40ft lorries.

Successes like this encouraged broad er experimentation with capital structures.

Developers began pairing local expertise with international funds. Malaysian, and even Canadian, and German institution al investors, he said, backed new industrial schemes.

This blended approach is central to how industrial estates are financed, as capital requirements are simply too big for developers to fund on their own, LaBrooy notes.

Where demand is moving

Interest is rising in areas that combine advanced manufacturing with complex services. Semiconductors remain central, with Malaysia targeting more than RM500 billion in semiconductor-linked investments across design, packaging, and equipment supply chains.

Clusters in Kulim, Kedah, and Batu Kawan, Penang are already pulling suppliers together. Meanwhile, electric-vehicle (EV) production is slowly converging around Tanjung Malim, Perak, where Malaysia’s Proton and international partners like China-based BYD are building capacity across the EV supply chain.

“The proposed Automotive Hi-Tech Valley in Tanjung Malim is a good example, where [local automotive conglomerate] DRB-HICOM and [Chinese multinational automotive company] Geely plan to consolidate the entire EV supply chain under one roof. Near by, KLK [Land Sdn Bhd] is collaborating with BYD in an adjacent precinct [KLK TechPark]. While both projects differ in approach, together they could transform Tanjung Malim into Malaysia’s next automotive hub, akin to the US’ Detroit,” LaBrooy says.

Another visible shift is happening in data infrastructure.

LaBrooy observes that investors underestimated the complexity of data centres, noting that operators demand ready infrastructure, and will not tolerate “five-year” lead times. Sites depending solely on fossil fuels are being rejected because of strict carbon targets.

“Data centre operators do not buy promises. They want power, water, and fibre in place before they sign anything. Some sites require two billion US dollars just to bring power in. That is not something private investors can carry alone.”

The appeal for investors is also straight forward, he adds. Most want a single contact point that handles permits, utilities, and infrastructure.

AREA’s view on the future of industrial REITs

AREA’s view is that Malaysia’s industrial REITs have matured, but still need scale to draw serious institutional capital. LaBrooy says the next step is to move beyond basic leasing, and operate more like service providers.

REITs that offer energy management, data insights, and green-certified buildings are already seeing stronger interest. The market also needs more high-spec assets, including automated warehouses, cold-chain facilities, and power-ready data centre sites. These products, he says, will shape the next stage of industrial REIT development in Malaysia.

Tomorrow’s industrial cities

The next generation of industrial estates will look and behave like managed urban systems rather than factories with fences. Power, water, and networks will be monitored centrally. Parks may buy bulk electricity from utilities, and resell to tenants. Data systems will track energy use, logistics flows, and worker access.

A few examples overseas hint at what this could look like.

China’s JD.com reportedly operates a highly automated warehouse that relies on robotics and artificial intelligence, with only minimal human staffing. Multi-storey logistics hubs are also becoming more common in dense locations where land is scarce.

Malaysia is moving in this direction. Besides the specialised semiconductor clusters forming in Kulim, and Batu Kawan, data centre districts are taking shape in Johor, and Negeri Sembilan.

According to LaBrooy, the strongest clusters tend to emerge when eco-systems form around shared needs.

“We have seen successful clusters like those driven by [German semiconductor company] Infineon and [American digital tech leader Advanced Micro Devices] AMD. But many developments are still happening ad hoc and not in a coordinated way. Industrial planning often happens in isolation. There are still parks created without a proper look at market dynamics, or they end up without sufficient power or connectivity to support modern industries.”

He believes the next generation of industrial parks must be designed with these requirements in mind: “They have to be future-ready, supported by green energy, efficient logistics, and a well-planned labour pool.

“We have seen examples of this in Johor, and Negeri Sembilan, where developers are now working with Tenaga Nasional [Bhd] and telecom operators at the planning stage, not after the park is built.”

From a regional perspective, Malaysia’s position remains attractive. It offers greater scalability than Singapore, more supply chain maturity than Vietnam, and fewer infrastructure hurdles than Indonesia.

Critical pressure points

Malaysia’s future as an industrial centre depends on two things above all others: power, and people.

While both areas are advancing, more capacity and coordination will be needed as the country attracts higher-value investments.

Rising interest from chipmakers and hyperscalers has brought new pressure on the grid. Capacity alone is no longer enough, LaBrooy says.

These industries rely on uninterrupted supply, secondary backup, and, increasingly, cleaner energy sources that satisfy corporate emissions targets.

This shift gives Malaysia room to improve. Grid upgrades, solar expansion, and new energy partnerships are advancing, although their pace will determine how Malaysia can convincingly compete for future capacity.

Talent is the second pillar.

Malaysia has long produced a steady stream of graduates, but too few in the specialisations needed for advanced manufacturing. These pressures are not unique to Malaysia. He explained that many countries are adjusting to the same competition, where demand is rising faster than the supply of qualified workers like electrical technicians, automation engineers, and semiconductor equipment specialists.

To address this, LaBrooy suggests a pragmatic way forward: The 60:40 STEM

(Science, Technology, Engineering, and Mathematics education) goal needs to match post-school reality. Right now, the gig economy offers quick cash and autonomy, while entry roles in engineering and tech can feel slow, underpaid and admin-heavy, he says.

These pipeline leakages from school, to university/Technical and Vocational Education and Training (TVET), to first jobs need to be plugged.

The brain drain needs to be addressed too: “Make staying (or returning) financially attractive. Build capacity where demand is exploding”.

He also notes that Malaysia’s most important asset is its human capital.

“Not just building local experts like architects, planners, and engineers who understand evolving technologies; but nurturing entrepreneurial talent is equally important”.

The question is how quickly Malaysia can align power infrastructure, training systems, and industrial strategy so that growth in new sectors can be sustained rather than sporadic.

The future is ecosystems, not just estates

The business is no longer about selling plots, and hoping tenants will fill them.

The next frontier lies in designing and operating environments that allow companies to perform at global standards from day one.

Success will depend on how quickly the country can bring policy, power, capital, and talent into alignment under a common purpose. The task is substantial, but industry players say the direction is clearer than it has been in years.

For investors watching the region, this is a sign that Malaysia’s industrial ambitions are not only taking shape, but gathering momentum.

Unlock Malaysia’s shifting industrial map. Track where new housing is emerging as talents converge around I4.0 industrial parks across Peninsular Malaysia. Download the Industrial Special Report now.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.