Reprice or reset? What pipeline properties tell us about market trends ahead

This article appeared in the March 12, 2026 issue of the monthly print edition. Subscribe now.

Despite witnessing a strong rebound over the past two years, the Malaysian property market continues to vie for firmer footing in a partially-rejuvenated, but still-cautious landscape.

Uncertainties persist because of ongoing concerns about oversupply, affordability, and external global economic influences, which could adversely impact progress and the gains thus far made in a recovering market.

Propagators of economic health prescribe nurturing an environment of gradual stabilisation and measured growth, while the government has indicated with Budget 2026 that it firmly intends to address the affordability gap, and refocus the market towards serving realistic demand. The drumbeat for transformative change seems to be growing louder.

In this climate, a pertinent question about house prices arises: Are we heading for a period of market repricing, or are we poised for a more fundamental shift in the form of a market reset?

For clarity, a reprice is a tactical and immediate revision strategy whereby vendors adjust the asking price of properties to address stagnant sales, meet the current market sentiment, or clear inventories.

A reset is a reformative change, brought about by government policies, economic shifts, or affordability pressures, which pushes the property sector to recalibrate median prices to a level that better serves national objectives.

Key industry observers point out that the market in 2026 is showing signs of both: repricing in the short term to reflect immediate affordability and sentiment adjustments, while leaning towards a reset in the mid- to long-term to achieve deeper structural reforms that reflect evolving buyer priorities.

In its recent Market Dynamics Report, JLL Malaysia head of research and consultancy Yulia Nikulicheva framed Budget 2026 as an “explicit statement” by the government about its intent to steer the property market towards a reset—leveraging fiscal and policy tools to tackle long-standing structural imbalances. (See story below for more.)

Nikulicheva noted that repricing is happening naturally in certain segments (luxury condos, oversupplied areas), but the official stance is that Malaysia’s property market needs a deeper recalibration to ensure long-term stability and affordability.

CBRE|WTW Malaysia’s Real Estate Market Outlook 2026 report highlighted a shifting stance from “resilience to relevance”, stressing that the property market is evolving beyond cyclical survival into a structural repositioning.

However, Knight Frank Malaysia’s commentary about the 2026 outlook emphasised that while policy support provides the backdrop, the differentiator will be clarity of demand and disciplined execution.

In short, the government’s fiscal stance will have tremendous influence on enabling a reset, but the speed and effectiveness of actual transformation also depends on market participation.

From that context, we take a close look at EdgeProp EPIQ’s latest data on residential properties in the pipeline over the next three years to track price movements of future properties, and identify possible shifting trends. Examining the figures will also offer insight into how developers are reacting to a potentially changing landscape.

Pipeline projects comprise over 80% high-rise in prime regions

According to EPIQ, there are currently 2,477 new private sector-led residential projects across the country at various stages of construction in the next three years.

Focusing our attention on the key regions that host the bulk of economic activity in the country, the Klang Valley, Johor, and Penang will account for 393,381 residential units coming onstream between 2026 and 2029. This will be made up of 63,393 landed properties, while the other 84% will be non-landed residences in these high-population regions.

It is worth noting that the development of non-landed homes in all three regions will far outpace landed homes in the foreseeable future.

And as high-rises continue to be the dominant residential stock in the years ahead, it will have a profound impact on median prices.

Selangor and Kuala Lumpur will see the highest number of pipeline residential projects coming into play in the next few years, with 889 developments providing 34,082 landed, and 245,575 non-landed units by 2029.

Ongoing economic expansion in Johor has pushed it to the second highest number of new projects in the country at 422, contributing 20,480 landed, and 46,664 non-landed units.

Limited land in Penang will see just 175 new projects making its way into the market, representing 8,831 landed, and 37,749 non-landed units.

Outside the key regions, Pahang is witnessing robust growth; seeing 268 new residential projects come into play in the next few years.

Enhanced development in the state is being largely driven by a mixture of industrial growth (Kuantan Port and the Malaysia-China Kuantan Industrial Park), tourism, and ongoing government housing initiatives.

Taking a look at price trends, however, a focus on the traditionally established economic hubs in the northern, central, and southern regions offer a better comparative view of movement and notable changes.

On this front, EPIQ identifies that there is a visible change in the lower end of price brackets of future supply across all the three key regions, with properties priced in the below RM250,000 bracket (<RM250k), and the RM250,000–RM499,999 (RM250k–499k) now representing a larger share of the stock compared with 2025.

In Johor and Penang, there seems to be a distinct growth trend for affordable and mid-priced property offerings over the next three years, especially in the high-rise segment. In the Klang Valley, however, this trend fluctuates from year to year, indicating that developers continue to back sustained demand for higher priced properties in the capital and surrounding districts.

On aggregate, the RM250k–499k looks poised to be a dominant price bracket for future property in key regions. While there is also clear growth in the <RM250 bracket, this seems more pronounced outside the Klang Valley, with periodic gains occurring within it as time progresses.

Klang Valley—demand for location, provision, transportation holds up

A wide spectrum of suburban residential developments has expanded the availability of housing and investment options within the Klang Valley. Despite an increasing supply of residential units, especially in the high-rise segment, demand for well-situated, lifestyle-driven, and transit-oriented developments is expected to remain sustained, encompassing both the city centre offerings as well as those in emerging affluent suburban corridors.

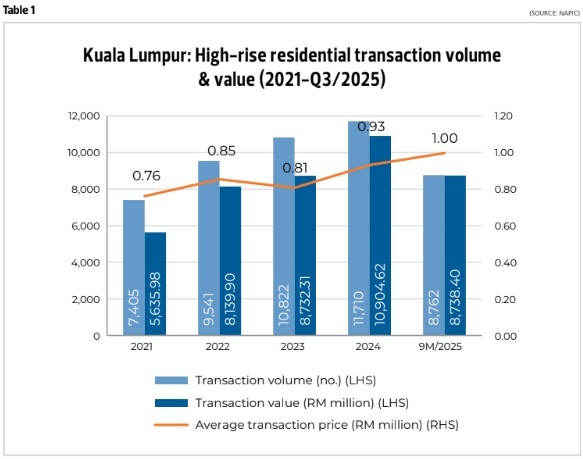

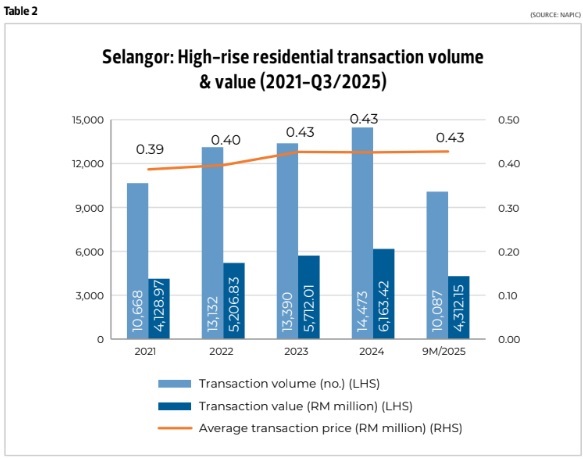

On the landed property front, the Klang Valley currently hosts a cumulative supply of 1.04 million houses (Selangor: 938,160, KL: 105,645).

EPIQ data shows that the average transaction price (as at 3Q2025) was RM1.44 million for KL, and RM730,000 for Selangor. Meanwhile, there is a cumulative supply of approximately 1.11 million high-rise units in the Klang Valley with average transaction prices of RM997,300 for KL and RM427,490 for Selangor (Table 1 & Table 2).

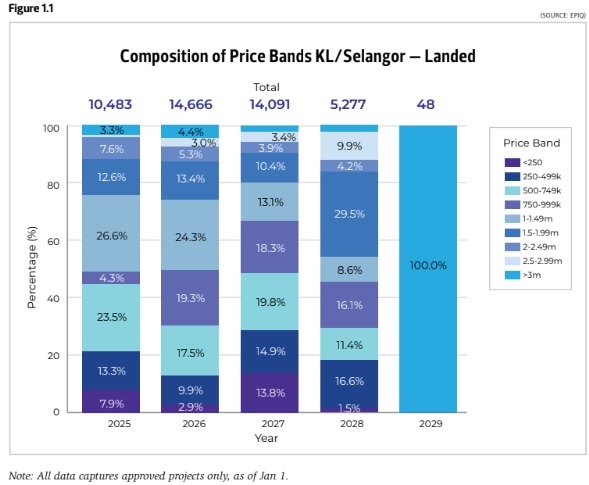

Looking ahead, the future supply of landed properties continues to lean in favour of higher-price brackets, as urban density drives land prices upwards, making landed homes the upmarket choice, and high-rise living the more affordable choice. As such, landed homes will continue to primarily target upper middle-income and high-income earners in the years ahead.

In 2026, the RM1 million–RM1,499,999 (RM1m–1.49m) range continues to represent the largest bracket at 24.3%, albeit a slight contraction from 26.6% registered in the previous year. Meanwhile, the RM750,000–RM999,999 (RM750k–999k) bracket grew substantially from 4.3% in 2025 to 19.3% in 2026 (Figure 1.1).

The future supply of landed homes in both the RM500–749k and RM250–499k brackets reduced in 2026, to 17.5% and 9.9% respectively.

In the below <RM250k, it is important to note EPIQ only tracks projects by private developers, so the figure does not include fully-funded government projects. The data shows the private developers’ focus in this segment shrunk from 7.9% in 2025 to 2.9% in 2026.

Beyond 2026, however, we see a marked increase in the <RM250k bracket (13.8%) in 2027, before dipping again in 2028 (1.6%). The RM250-499k will see a gradual increase to 14.9% in 2027, and 16.6% in 2028, targeting more landed homes at mid-income earners.

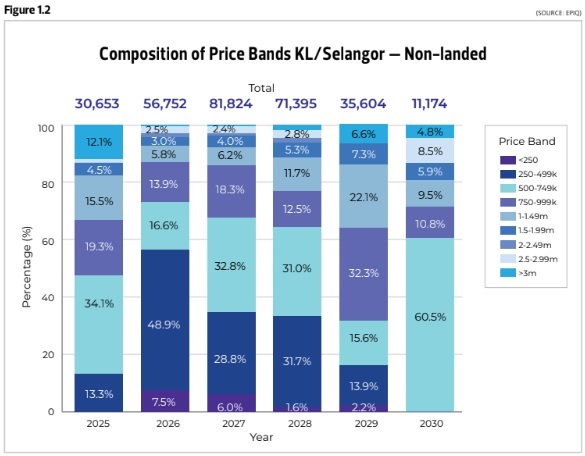

Price trends seem clearer for Klang Valley’s non-landed segment. The RM250-499k price bracket will see the largest expansion, moving from 13.3% in 2025 to 48.9% this year. Over the following two years, the supply will even out to 28.8% in 2027, and 31.7% in 2028 (Figure 1.2).

High-rise units in the RM500–749k bracket will also see an increase beyond 2026, going from 16.6% in the current year to 32.8% in 2027, and 31% in 2028.

Notably, developers are beginning to contribute to the <RM250k bracket following a 2025 that saw little involvement, albeit on a small scale. In 2026, units in this price bracket will represent 7.4% of incoming stock, and in 2027, it will represent 6%.

Overall, there seems to be some gradual movement towards lower-priced properties in the Klang Valley, with more options available in the mid-price segment. However, there does not seem to be a fundamental pivot towards affordably-priced offerings in the near future, as a considerable amount of pipeline properties are still within higher price segments.

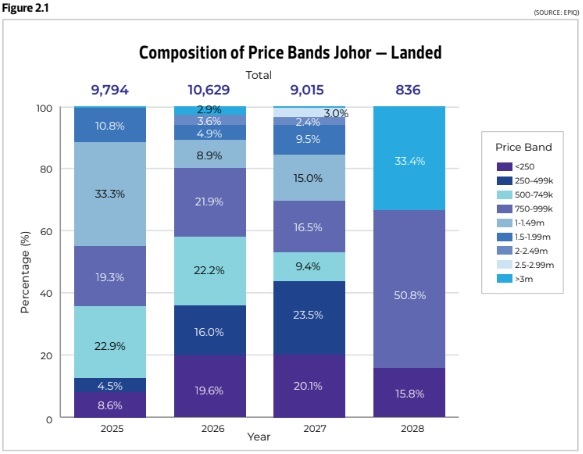

Johor—non-landed oversupply slips

In Johor, the story is a little different. Ongoing oversupply issues continue to plague the landscape, although the situation has seen gradual improvement in recent years.

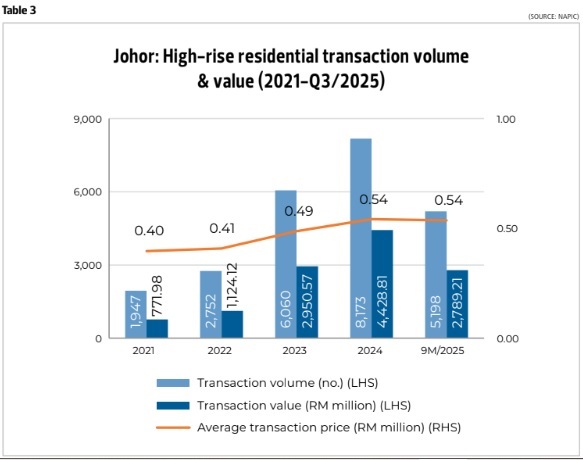

Of particular concern is the high volume of unsold high-rise units, mostly comprising serviced apartments and SoHos, although the National Property Information Centre (Napic) reports that this has dipped from 8.6% (18,015 units) in 3Q2024 to 7.5% (16,743 units) in 3Q2025.

Napic also highlights that supply reduced by about 25% from 16,000+ units in 3Q2024 to 12,000+ units in 3Q2025. Despite this, Johor’s unsold inventory remains the highest among Malaysia’s major markets.

As such, developers are progressing very judiciously and this has begun to reflect on the state’s pipeline supply, where prices are adjusting to balance growth with a more accurate perspective on realistic demand.

Currently, Johor has a cumulative supply of approximately 634,700 landed houses, and the average transacted price was around the RM610,000 mark in 3Q2025.

EPIQ data show the next few years see a very evident contraction of landed properties priced over the RM1 million mark. The RM1m–1.49m bracket, for example, has shrunk from 33.3% in 2025, to 8.9% in 2026 and amounts to 15% by 2027 (Figure 2.1).

At the opposite end of the scale, landed properties priced in the <RM250k bracket will grow to 19.6% of the stock in 2026, and expand to 20.1% in 2027, before settling at 15.8% by 2028.

Similarly, houses in the RM250–499k bracket represent 16% of incoming supply in 2026, and this will grow to 23.5% in 2027.

In the non-landed segment, high-rises have a cumulative supply of 185,831 units in Johor. As at 3Q2025, the average transaction price was in the region of RM536,590 (Table 3).

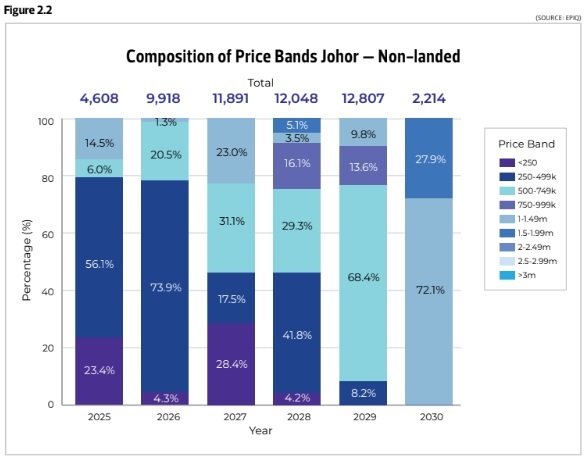

High-rises in the RM250–499k bracket continue to dominate the skyline, growing from an already high margin of 56.1% in 2025 to 73.9% in 2026. This will readjust in 2027, contracting to 17.5%, before expanding to 41.8% in 2028.

High-rise units in the <RM250 bracket will initially contract in 2026 to 4.3%, after representing 23.4% of the stock in 2025. However, data shows that it will rise again to 28.4% in 2027 before another contraction to 4.2% in 2028 (Figure 2.2).

In general, the Johor market seems to be steering itself firmly towards affordably-priced properties, with the non-landed segment poised to offer a high volume of options to mid-income buyers. In fact, of the three key regions, Johor has also shown the strongest focus towards the <RM250 price bracket thus far.

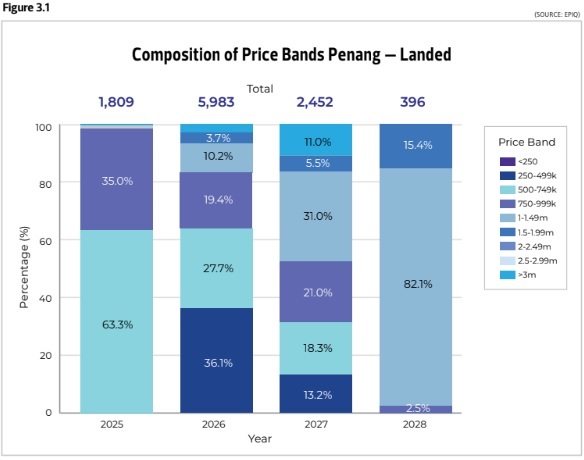

Penang—land scarcity limits transaction activity

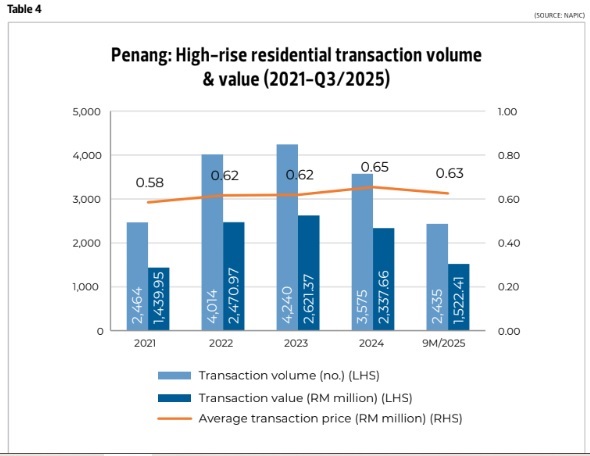

The Penang property market is proving to be a challenging one, amidst increasing supply, and high unsold rates. Transaction activity also dipped significantly by 7.8% in volume (9,800 units to 9,030 units), and 11.8% in value (RM5.1 billion to RM4.5 billion) between 3Q2024 and 3Q2025.

Space limitations in Penang, specifically in or close to the main urban nucleus of the island, limits the opportunity to own landed properties in the state. Despite this, there continue to be landed offerings on a small scale, though very little in the <RM250 bracket due to land scarcity.

Most new landed property projects are midrange offerings taking shape on the mainland in the Seberang Perai and Bukit Mertajam areas, while a limited supply of upmarket landed homes are situated within the Bayan Lepas and Free Trade Zone on the island.

Penang has a cumulative supply of 249,640 landed homes on its landscape, and average transaction prices have been around the RM500,000 mark.

In 2026, landed properties in the RM250– 499k bracket represent 36.1% of incoming supply. This is due to shrink to just 13.2% of the total supply by 2027. This trend is similar in the RM500–749k price bracket, where this year’s incoming supply represents 27.1%, but is due to contract to 18.3% in 2027 (Figure 3.1).

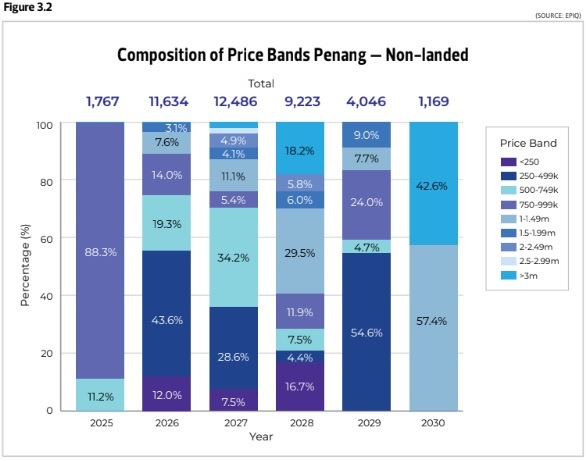

Looking at non-landed units, as at 3Q2025, over 76% of the units transacted ranged up to RM500k, indicating high demand for affordable and mid-range products.

Penang currently has a cumulative supply of about 137,840 high-rise units. On average, most transactions have been around the RM625,220 mark (Table 4).

Looking ahead, future high-rise properties are poised to offer more in terms of affordable home options. The <RM250k will account for 12% of incoming supply, with future 2027 stock dipping to 7.5%, before rebounding to 16.7% in 2028.

High-rises in the RM250–499k price bracket represents a sizeable 43.6% of incoming supply in 2026. However, this will trend downwards with future supply to 28.6% of the total in 2027, and just 4.3% in 2028 (Figure 3.2).

By contrast, the volume of higher priced non-landed units will see growth over the next two years. There will be a noticeable jump in the RM500–749k bracket from 19.3% to 34.2% between 2027 and 2028. Meanwhile, the RM1m– 1.49m will grow from 7.6% in 2026 to 11.1% in 2027, and to 29.5% in 2028.

Overall, while Penang properties continue to be concentrated in higher price brackets, there has been an observable effort to incorporate more affordable properties in future incoming stock. This is especially evident in the pipeline supply of non-landed units, where lower priced residential options can be best accommodated.

Which way is the market headed?

EPIQ data reveals that while there are noticeable shifts in price trends occurring across the three main economic regions in Malaysia, the changes captured depict either gradual or fluctuating movement—not drastic changes that signal a price reset is currently underway.

It is important to note many of the projects that make up the current pipeline supply were planned and approved prior to Budget 2026 announcements, so newly approved projects beyond this point could still shift the dial on prices in the longer term.

Currently, the price adjustments we are already witnessing suggest that some developers are attuned to shifting market dynamics, and have organically recalibrated their products and pricing to fit. However, the data also shows that there is no wholesale buy-in for a dynamic shift in prices as of yet.

As time progresses, new project approvals and the execution of government initiatives aimed at driving a reset, will give us a better picture of how effectively, or how rapidly, government intervention will influence price trends going forward.

For now, the market can still expect to see an increase in housing options for the mid- and lower-priced brackets, as developers slowly steer their products towards prevailing demand.

What buyers can expect in the 2026 property environment

While it may yet take time for government directives to impact developer perspective, changing consumer sentiments have already begun to make an impact.

Napic reported that overall transaction volumes dipped in 2025, while transaction value rose—meaning fewer deals, but at higher average prices. This suggests a trend of selective buying rather than broad-based growth.

Market analysts generally agree that the market has shifted to “value over hype”, and that buyers are becoming increasingly pragmatic; focusing on location and functional space rather than speculative gains. Affordability hurdles, demographic shifts, and changes in lifestyle preferences (smaller households or suburban locations) are already reshaping demand.

The takeaway is that 2026 will reward clarity of demand and location, not sheer volume.

Developers too are observably bracing for tighter margins, and the prospect of more discerning buyers.

In the short term, certain urban hotspots such as KL, Damansara, and Petaling Jaya are likely to experience some repricing, as developers trim their expectations, and buyers negotiate harder.

The overall forecast is for steady growth, not an explosive one. The market is expected to expand moderately, with transaction values that will rise in tandem with economic growth.

The positive news for home purchasers is that interest rates are stabilising at 2.75% overnight policy rate (OPR). Combined with a strengthening ringgit, this will improve loan affordability, especially for first-time buyers.

However, the government’s determination to reset the market looms, and it has made it clear that the era of speculative “easy money” is over. As such, property investors should prepare for a reset mindset, and place greater focus on long-term fundamentals rather than shortterm price swings.

FACTORS NECESSITATING A RESET, GOVERNMENT MEASURES DRIVING IT

Budget 2026 is being touted as a defining moment for Malaysia’s housing sector, potentially delivering a reset that market observers say is necessary to effectively address overhang issues, affordability challenges, and legislative shifts.

Some of the main factors driving the government’s desire to reset the property market include:

*Housing overhang: Malaysia has faced a persistent oversupply of unsold units, especially in high-rise urban developments. This imbalance distorts prices, and leaves developers with excess inventory.

*Affordability crisis: Property prices have outpaced income growth, making homeownership difficult for younger Malaysians. Reset policies aim to prioritise affordable homeownership and financing access.

*Speculation vs sustainability: Past incentives encouraged speculative buying, inflating values without matching real demand. The government now wants a market that rewards genuine demand, sustainable development, and asset repurposing (converting underused commercial spaces).

*Urban imbalance: Kuala Lumpur and surrounding areas have seen saturation, while suburban and secondary cities need more balanced growth. Reset measures encourage decentralisation and infrastructure-led expansion.

To achieve these goals, the government has taken the following action:

*Budget 2026 (Madani Economy Framework): A RM419.2 billion allocation framed this as “The Rakyat’s Budget”. It emphasises affordability, sustainability, and strategic housing supply rather than speculative growth.

*Consequential shift in policy approach: Instead of broad incentives, the government stressed that the property sector must mature—focusing on affordability, sustainability, and asset repurposing. This marks a deliberate move away from speculation-driven cycles.

Some of the implications of a reset include:

*Affordability first: Policies are designed to make housing more accessible, aligning with the 13th Malaysia Plan’s target of one million affordable homes by 2035.

*Better market discipline: Developers are expected to pivot toward realistic demand, smaller unit sizes, and sustainable designs.

*Reduced speculation: The government is signaling that property investment must now be grounded in fundamentals, not quick flips.

WHAT THE EXPERTS SAY

Why are developers still focused on high-rise residential projects despite the surplus?

Evon Heng, PropNex Malaysia chief operating officer

“To maintain feasibility and optimise land yield, developers need density. High-rise becomes a financial necessity rather than just a preference. Escalating land cost in prime urban areas is a major factor behind the continued focus on high-rise development, and sustained demand for it.”

Jamie Tan, JLL Malaysia managing director

“At the more affordable end of the market, high-rise developments are also the most viable form of housing. As land becomes increasingly scarce and expensive, it is no longer economically feasible to build landed homes at affordable price points within urban areas. High-rise apartments therefore provide a more accessible entry point for homeownership.”

Long Shi Chuen, Henry Butcher Malaysia director of corporate real estate

“Transit-oriented developments (TOD) are a driving factor because land around these areas are allowed a higher plot ratio. The MRT3 Circle Line in Kuala Lumpur, Penang LRT Mutiara Line, and Johor Bahru–Singapore RTS Link create TOD opportunities favouring high-density projects. Strong capital appreciation potential for properties located close to transport nodes will continue to propel buyer demand.”

..........

EdgeProp's inaugural monthly print edition is fresh off the press! Free delivery is available for selected regions. Subscribe now.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.