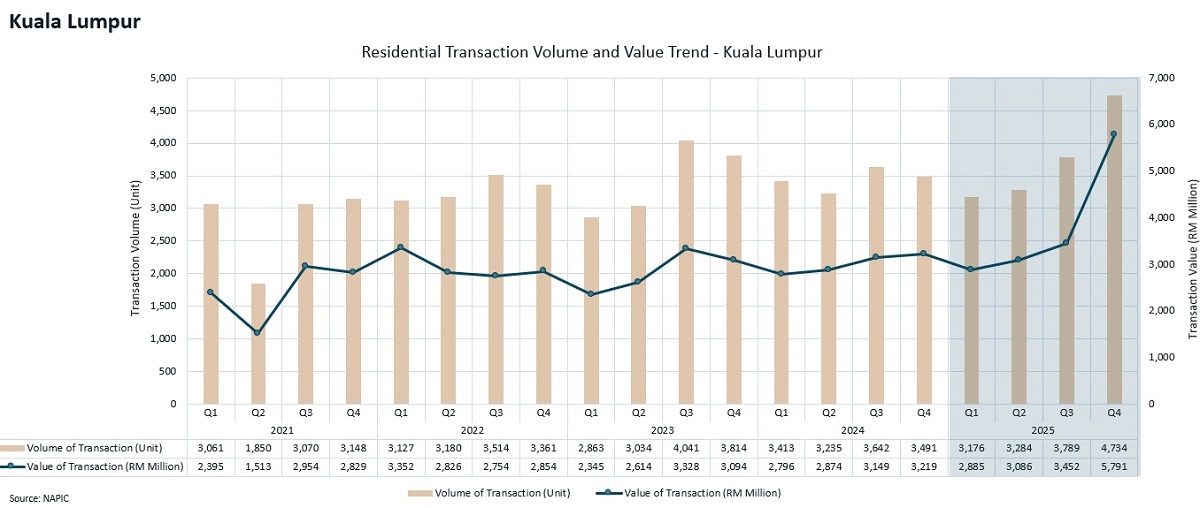

Kuala Lumpur residential market hits five-year high in 4Q — JLL

KUALA LUMPUR (April 29): Kuala Lumpur's residential property market recorded steady quarterly growth throughout 2025, with each successive quarter surpassing the previous, culminating in the strongest performance since 2021.

The fourth quarter registered 4,734 transactions — the highest quarterly volume recorded between 2021 and 2025 — while transaction value reached RM5.8 billion, also the highest level since 2021, indicating a firmer performance trajectory for the capital’s residential sector, JLL Malaysia managing director Jamie Tan said in their 2Q2026 press conference held here at Menara IQ @TRX on Tuesday, aimed at discussing Malaysia’s real estate markets latest trends and updates.

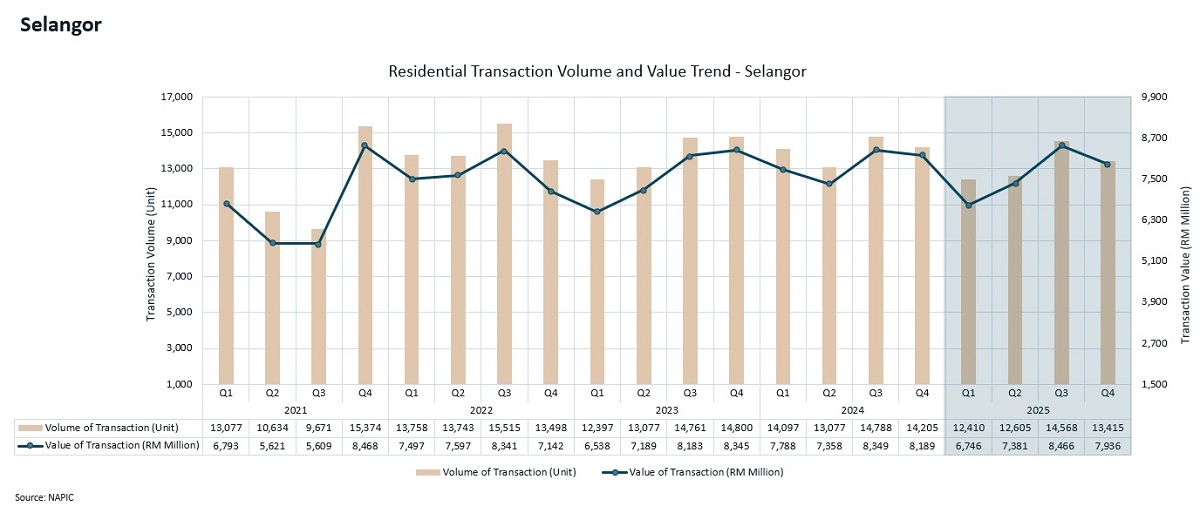

Meanwhile, in Selangor, the residential market recorded a marginal contraction of less than 1% in 2025 in both transaction volume and value compared to the previous year.

As the largest residential market in the country — accounting for approximately 21% of total transactions — Selangor encompasses a broad spectrum of housing, from affordable units to high-end residences, which may contribute to differing performance trends across sub-segments.

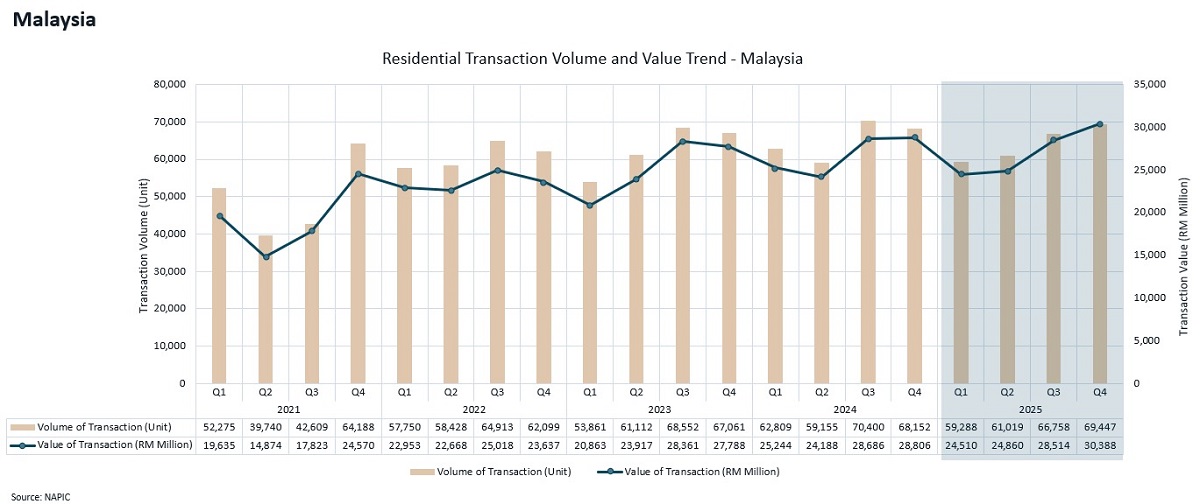

At the national level, the volume of residential property transactions in 2025 declined marginally by 1.5% year-on-year (y-o-y), while total transaction value recorded a modest increase of 1.3% compared to 2024.

Despite the slight dip in volume, each quarter in 2025 registered sequential growth, culminating in the strongest quarterly performance of RM30,888,000 in terms of value since 2021 — a trend that points to continued momentum underpinned by sustained buyer participation and stable underlying fundamentals, said Tan.

The data suggests that Malaysia’s residential property market remains on a steady footing, with transaction activity reflecting ongoing liquidity and demand.

However, Tan noted that performance is not uniform across all states and sub-segments.

JLL's 2026 outlook also flagged four key risks to watch:

1) rising energy prices driving up construction and building material costs;

2) geopolitical conflicts creating a wait-and-see environment among business owners and investors;

3) younger households preferring to rent amid geopolitical uncertainty and tightening bank financing; and

4) residential prices remain largely stable in the short to medium term due to the relative inelasticity of real estate, though prices could creep up over the longer term if global conditions worsen, as a shock to supply will bring prices up.

Southeast Asia resilience and flight to quality

JLL Singapore and Southeast Asia CEO Michael Glancy added that Southeast Asia’s real estate markets, including Malaysia, are demonstrating resilience despite ongoing global headwinds.

Malaysia, in particular, is seen as well positioned within the region, underpinned by a strong track record of institutional, developer and private-led investments across international markets such as Singapore, Australia and Europe — a positioning Glancy said could allow the country to take on a broader leadership role in both real estate and finance within Southeast Asia.

In the office sector, Glancy highlighted a continued “flight to quality” and “flight to green” trend, driven largely by occupier demand, and that is consistent in Malaysia.

“We are now sitting in a LEED and WELL Gold-accredited office with JLL, and we are seeing our occupier clients really driving that, and that is set to continue for the foreseeable future,” said Glancy.

Corporates are increasingly prioritising high-quality, sustainable buildings to attract and retain talent while meeting sustainability targets, supporting demand for Grade A office space — particularly as return-to-office rates across Asean remain high.

At the same time, the market is experiencing a growing bifurcation, with premium-grade assets achieving stronger rents and occupancy levels while older Grade B and C buildings face mounting pressure.

Asset enhancement initiatives — including upgrades to meet green building standards — are expected to become a key strategy to maintain competitiveness and avoid obsolescence.

In Greater KL specifically, the office market data as at 1Q2026 showed KL city stock at 34.47 million sq ft with an occupancy rate of 82.5%, while KL fringe recorded a higher occupancy of 93.5% across 17.83 million sq ft, and the decentralised submarket stood at 78.3% across 11.71 million sq ft.

Average achievable monthly rents were RM7.45 psf in KL city, RM6.75 psf in KL fringe and RM5.26 psf in the decentralised submarket.

A total of 4.33 million sq ft of new office supply is in the pipeline for 2026 to 2030, with notable upcoming completions including The Capitol (25% pre-committed) and Menara Ethos @ TRX (25% pre-committed from global professional services network PricewaterhouseCoopers (PwC)).

Data centres, industrials, and the China+X effect

On the data centre segment, Glancy said Asean is expected to remain one of the most active hubs globally, supported by rising demand linked to artificial intelligence and digital infrastructure.

Malaysia is seen as uniquely positioned in this space because of its availability of power, water and land, as well as its strategic location, with government efforts to support AI development and colocation leasing emerging as a growing area of activity.

JLL's data centre growth rate data shows Malaysia's operational capacity stood at approximately 900MW at end-2025, expected to more than double to 2,055MW by end-2026 — an addition of 1,155MW — with a further pipeline of 3,500MW planned beyond 2027.

In Greater KL, completed data centre capacity stands at 182MW with 615MW under construction and a 765MW pipeline, with key locations in Cyberjaya, Bukit Jalil, Petaling Jaya, KL city centre, and northern KL.

Johor remains Malaysia's largest data centre hub, with 850MW completed, 1,800MW under construction and a 2,700MW pipeline, anchored by clusters in Sedenak Tech Park, YTL Green DC Park, Quantum Edge Business Park, Nusajaya, and Johor Bahru city centre.

In the industrial and logistics sector, Southeast Asia is moving up the value chain, particularly in sectors such as automotive and semiconductors, supported by more advanced logistics infrastructure.

Glancy noted that evolving “China +X” strategies are driving outbound investment into multiple Asean markets, benefiting countries including Malaysia, Thailand, Indonesia, and Vietnam.

Malaysia, in particular, is experiencing increased investment from Taiwan and Japan in advanced technology manufacturing, reflecting the country's strengthening role within regional and global supply chains.

In Greater KL's industrial and logistics market, prime stock stood at 36.8 million sq ft in 1Q2026 with average rents of RM2.18 psf per month and a vacancy rate of 6.6%.

Shah Alam remains the highest-priced industrial submarket at RM248 psf (9.7% CAGR since 2019), while Bukit Raja offers stable institutional-grade space at RM139 psf (2.7% CAGR), and Port Klang remains the most affordable at RM102 psf (3.3% CAGR).

In Johor, prime industrial and logistics stock stands at approximately 13 million sq ft with average rents of RM1.90–RM2.50 psf per month and a vacancy rate of 2%–8%, driven by key sectors including electrical and electronics, logistics, life sciences, medical, and oil and gas.

Industrial land prices in Johor reached RM86 psf in 2025, an 8.4% y-o-y increase, while Seberang Perai in Penang reached RM93 psf, a 5.0% y-o-y increase.

..........

EdgeProp's monthly print edition is out! Free delivery is available for selected regions. Subscribe now.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.