Malaysia emerges as world's No 2 digital FDI destination — and property markets in KL, Johor and Penang are set to feel it, says report

PETALING JAYA (May 4): Malaysia has quietly cemented its position as the second-largest developing-economy recipient of digital foreign direct investment (FDI) globally, trailing only India — a milestone that carries significant implications for Grade A office demand, industrial land values and data centre real estate across the country's three primary digital investment hubs.

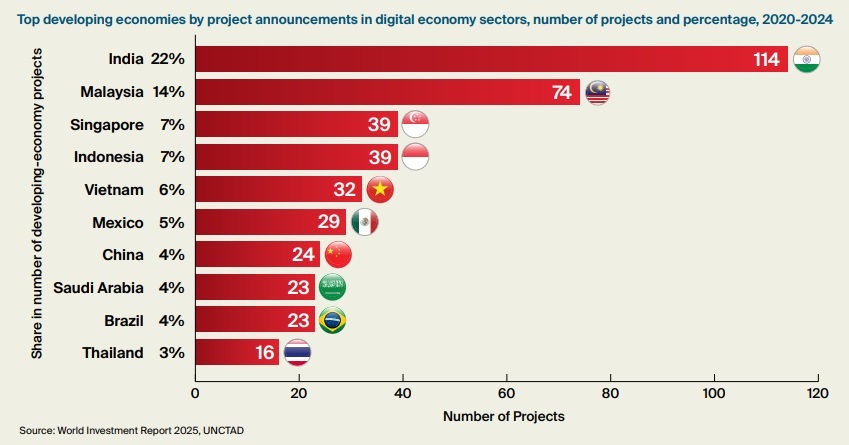

According to a whitepaper jointly published recently by Knight Frank Malaysia and the Malaysia Digital Economy Corp (MDEC), Malaysia attracted 14% of all digital greenfield investment projects among developing economies between 2020 and 2024, recording 74 project announcements — ahead of Singapore (7%), Indonesia (7%), Vietnam (6%) and Thailand (3%), based on UNCTAD's World Investment Report 2025.

The broader context is striking: global digital greenfield investments nearly tripled from US$131 billion in 2020 to US$360 billion in 2024, accounting for close to a third of total global greenfield projects.

Read also:

Malaysia has a certified office supply problem — and RM342b in digital investments is about to expose it

Merdeka 118 is Malaysia's first MD Nexus building — here is what it means for rents, tenants and the race to stay relevant

Malaysia's positioning within this surge — second only to India at 22% — reflects a combination of infrastructure readiness, a pro-investment policy environment and competitive real estate fundamentals that regional peers have struggled to replicate at the same scale.

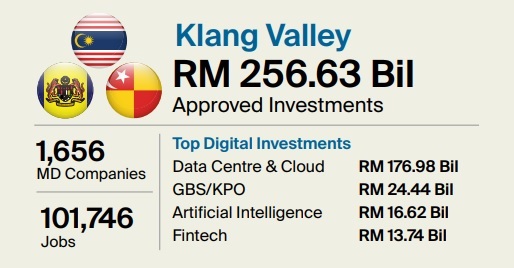

Between the second half of 2022 and the second half of 2025, Malaysia approved RM342.58 billion in digital investments across 1,969 Malaysia Digital (MD) status companies, projected to generate 114,854 jobs — of which 97% are knowledge-worker roles.

Foreign investments accounted for 67.7% or RM231.91 billion of the total, concentrated overwhelmingly in infrastructure-led segments, particularly hyperscale data centres.

What it means for Grade A office demand

The jobs story is where the real estate implications become most visible.

With 97% of projected digital economy employment classified as knowledge-based roles, demand for high-quality, digitally enabled office space is structurally underpinned — and growing.

The Knight Frank/MDEC report released in February notes that foreign digital companies strongly favour purpose-built offices (PBOs), with 55% of foreign MD firms operating from such premises.

Yet supply of certified space remains constrained.

Only 13% of MD companies currently operate from MD-certified premises, and just 15% are in green-certified buildings — with a mere 10% in both.

Critically, only 35% of existing PBO stock in Malaysia is MD-certified, and green-certified buildings account for just 21% of PBO stock in Klang Valley.

This gap between the quality demanded by global digital occupiers and the quality currently available is, in the Knight Frank/MDEC assessment, a supply problem rather than a demand problem — and one that is beginning to be addressed.

New office supply coming onstream in the Klang Valley, Johor and Penang is increasingly designed to be tech-ready and ESG-aligned, with the new Malaysia Digital Location Recognition (MDLR) framework — effective January 1, this year — providing a clearer building-level certification standard for developers and landlords to target.

The flagship example is Merdeka 118, which was named the first office building recognised under the MD Nexus category of the MDLR framework, reflecting its digital infrastructure readiness and operational resilience.

In Greater KL's office market, KL Fringe — which recorded a notably high occupancy rate of 93.5% as at 1Q2026, significantly above KL City's 82.5% — is emerging as the submarket of choice for digital economy occupiers, driven by a cluster of newer, greener, more digitally enabled buildings at competitive rents relative to the city core.

Concurrently, the paper highlights that Malaysia’s most established digital segments — artificial intelligence, Global Business Services (GBS) / Knowledge Process Outsourcing (KPO), and fintech — show the highest concentration within PBOs across all digital activity categories.

As these sectors expand, their demand for office space is expected to scale in tandem. GBS/KPO alone accounts for 39,428 projected jobs from RM26.16 billion in approved investments — the strongest employment multiplier among digital segments—supporting sustained, recurring office demand rather than the one-off land and utility usage typically associated with data centres.

What it means for industrial land and data centre real estate

The data centre investment story is where the numbers become most dramatic.

Data Centres & Cloud account for 74.6% or RM255.51 billion of total approved digital investments — yet generate only 11,978 direct jobs, the fewest per ringgit invested of any digital segment.

The implication for property markets is clear: data centres reshape industrial land values and utility infrastructure at scale, without generating commensurate office demand.

In the Klang Valley, Cyberjaya remains the highest-density data centre location, while Northern Kuala Lumpur has emerged as a focus area for a major US hyperscale provider pursuing an aggressive market-entry strategy through built-to-lease and direct land acquisitions.

Completed data centre capacity in Greater KL stood at 182MW as at 1Q2026, with 615MW under construction and a 765MW pipeline.

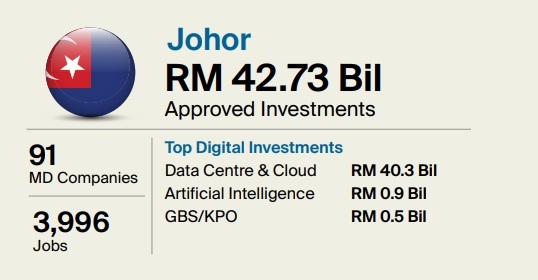

Johor, however, remains Malaysia's dominant data centre geography.

The state accounts for RM40.3 billion of data centre and cloud investment — virtually all of Johor's RM42.73 billion in total approved digital investments — with completed capacity at 850MW, 1,800MW under construction and a 2,700MW pipeline.

The concentration of hyperscale campuses in Sedenak Tech Park, YTL Green DC Park and Nusajaya has placed unprecedented pressure on industrial land supply in Johor, with average industrial land prices rising to RM86 psf in 2025, an 8.4% year-on-year increase from RM79.35/sq ft a year earlier, according to JLL Research.

Penang tells a structurally different story.

The state attracted RM41.33 billion in approved digital investments, but with zero data centre facility construction — all of its data centre and cloud investment is services-driven, focused on cloud provision and integrated circuit (IC) design in support of the semiconductor ecosystem.

Industrial land in Seberang Perai reached RM93 psf in 2025, a 5.0% year-on-year increase, reflecting sustained demand from electronics and semiconductor-adjacent manufacturing.

The outlook

Malaysia's digital investment trajectory points to continued and accelerating demand for both premium office space and industrial land across its three primary hubs.

The challenge — and the opportunity — lies in closing the certification gap.

With the MDLR framework now in place and new office supply increasingly aligned to MD Nexus and green building standards, developers and landlords who move early to achieve certification stand to benefit disproportionately from what is, by any measure, one of Southeast Asia's most structurally supported property demand stories.

Sources: Knight Frank Malaysia and Malaysia Digital Economy Corp (MDEC), "Malaysia as a Regional Digital Economy Gateway" (February 2026); JLL Malaysia 1Q2026 press conference data.

..........

EdgeProp's monthly print edition is out! Free delivery is available for selected regions. Subscribe now.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.