Sime Darby Property’s latest deal a fair entry to KL’s crowded prime market — analysts

KUALA LUMPUR (July 7): Sime Darby Property Bhd (KL:SIMEPROP) is getting a good deal from its latest acquisition even as the developer will be competing in an increasingly tough market.

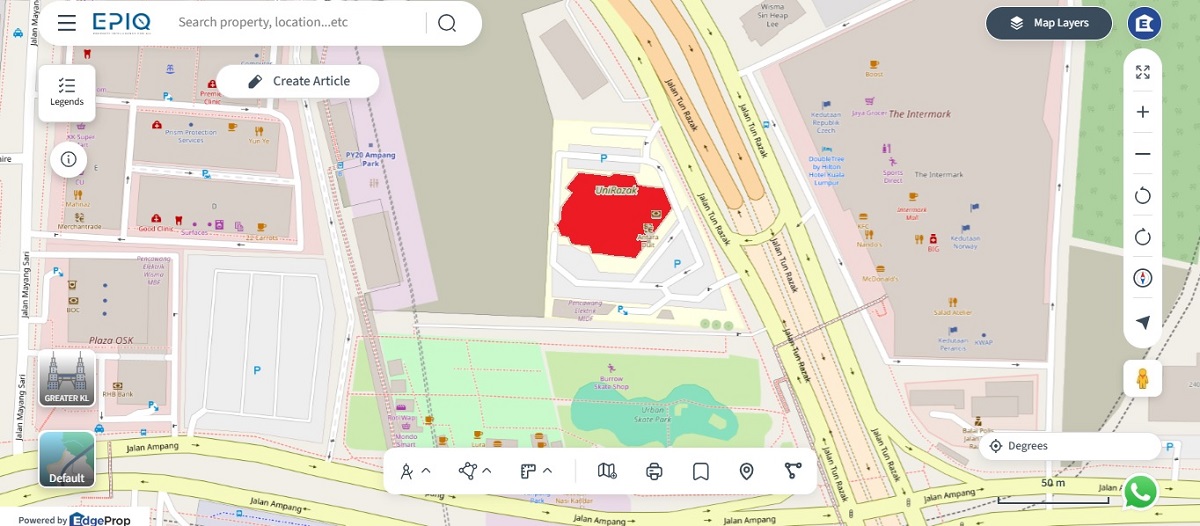

The price tag of RM160 million for the proposed acquisition of Wisma Unirazak in the heart of Kuala Lumpur city centre is “fair” and “reasonable” given the discount to independent market valuation and recent transactions, according to research houses including Maybank Investment Bank.

“However, we are cautious about the increasingly crowded KLCC market” given competition from high-rise projects nearby, Maybank Investment said.

On Monday, Sime Darby Property announced that it is buying the 15-storey office building located along Jalan Tun Razak from its majority shareholder and state-owned asset management company Permodalan Nasional Bhd. The plan is to redevelop the nearly five-decade-old site into a premium high-rise serviced apartment project with an estimated gross development value of RM900 million.

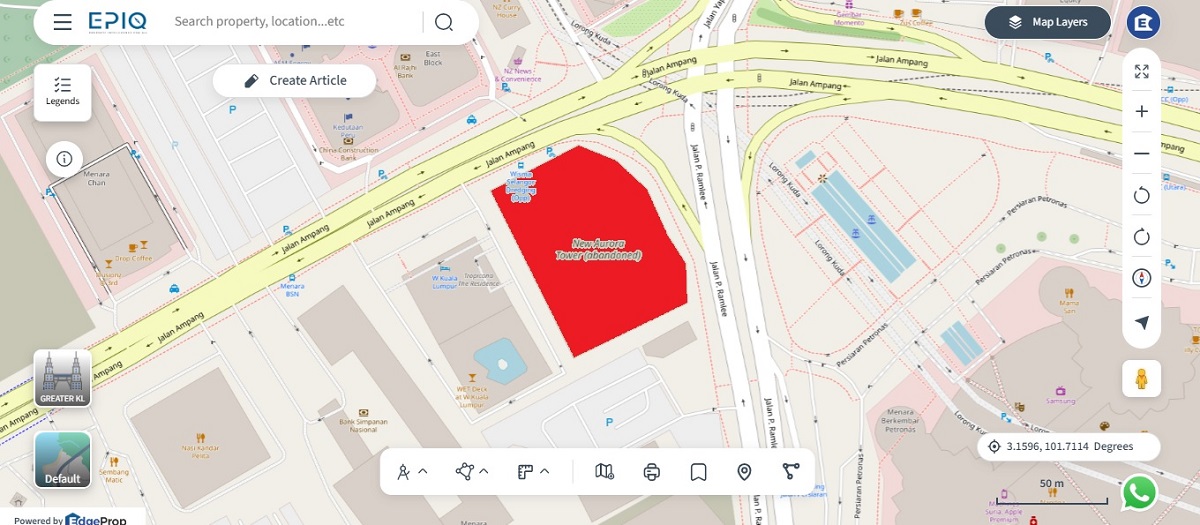

Days earlier, UEM Sunrise Bhd (KL:UEMS) announced the development of its 1.6-acre site at the junction of Jalan Ampang and Jalan P Ramlee into a mixed-use project comprising a hotel, residences and a retail mall.

TA Securities said the deal gives Sime Darby Property a rare freehold redevelopment site that is benefitting from direct access to the Ampang Park LRT and MRT interchange, as well as proximity to key commercial and lifestyle hubs.

“This should support a premium mixed-use product” and broaden Sime Darby Property’s exposure beyond township and industrial developments, the research house said. However, the take-up rate will depend on product differentiation, branding, unit sizes and overall lifestyle proposition, given the competition targeting a similar high-end buyer pool, the house warned.

Analysts tracked by Bloomberg are nearly unanimously bullish on Sime Darby Property, with 12 ‘buy’ calls and Maybank Investment having the sole ‘hold’ recommendation. The 12-month average target price is RM1.87.

AskEdge data shows Sime Darby Property trading at nearly 17 times its trailing earnings, which is higher than most peers but still at the lower end of its historical valuation in recent years.

Shares of Sime Darby Property were down by one sen or 0.72% to RM1.37 at 10am on Tuesday, giving the company a market value of about RM9 billion.

Read also:

Sime Darby Property buys Wisma Unirazak for RM160 mil, plans mixed-use project

UEM Sunrise secures RM415 mil entitlement in KLCC land pact with Exsim KLCC

..........

Read about emerging trends, data-backed insights, growing subsectors, and expert commentaries in EdgeProp print. Subscribe now for your free copy!

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.