KIP REIT calls unitholder vote on RM435 mil Setapak mall buy

PETALING JAYA (July 9): KIP Real Estate Investment Trust (KIP REIT) has issued a circular to unitholders seeking approval for its proposed RM435 million acquisition of Setapak Central Mall in Kuala Lumpur and a concurrent private placement of up to 220 million new units, ahead of a July 23 unitholders’ meeting.

It said in a Bursa Malaysia filing yesterday that the circular formalises the structure first announced in April: Pacific Trustees Bhd, acting as trustee for KIP REIT, will acquire the three-storey shopping mall with basement car park from Festiva Mall Sdn Bhd (FMSB), and partly fund the purchase via a placement equal to about 22.95% of existing units.

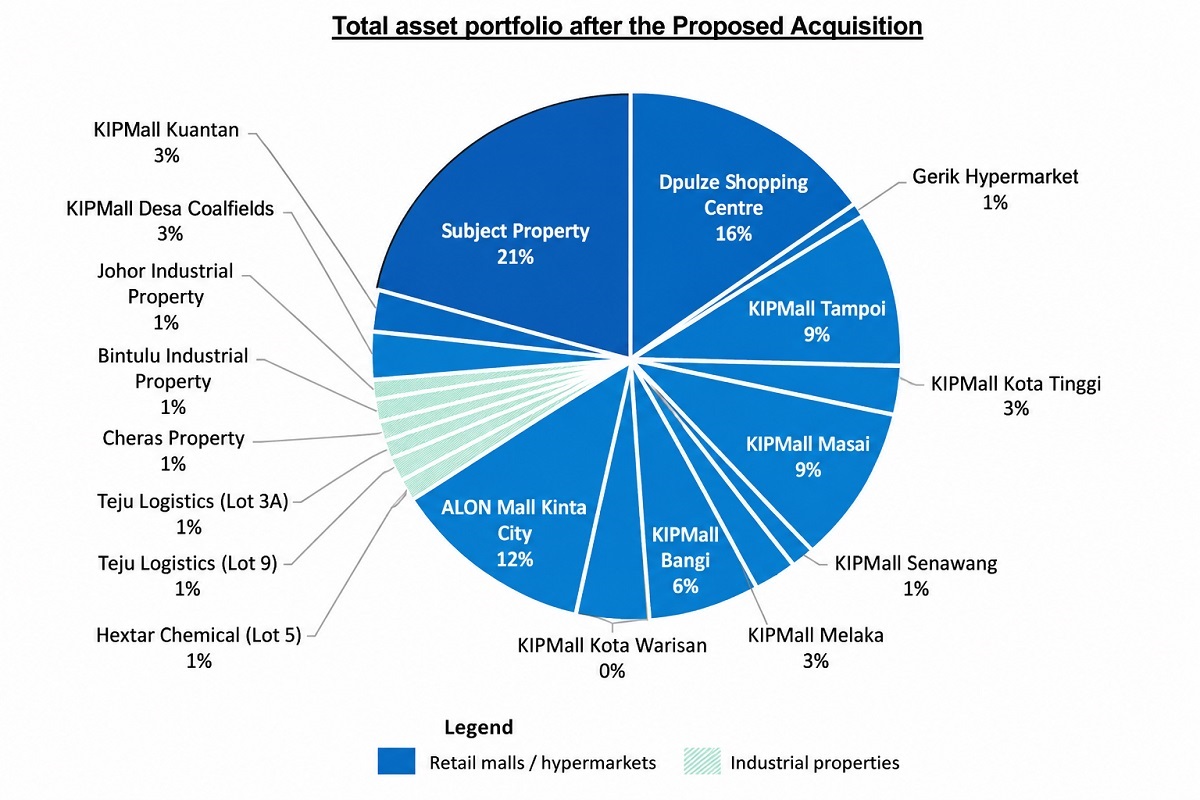

The mall: Setapak Central as a 21% portfolio anchor

The subject property comprises Setapak Central Mall, a purpose-built three-storey retail centre with a basement car park on Lot 30119, Mukim Setapak, held under a 99-year leasehold title expiring on Nov 20, 2106. Total strata floor area is about 100,967 sq m (1,086,798 sq ft), with gross floor area of 66,351 sq m (714,196 sq ft) and net lettable area (NLA) of 47,824 sq m (514,777 sq ft).

As at Feb 28 2026, the mall’s occupancy rate stands at 99.89%, with 228 tenancies across department store, F&B, fashion, leisure, houseware, beauty, supermarket and other trade categories. Based on the latest figures in the circular, the mall generated net property income of about RM31.3 million, implying a yield of around 7.2% on the RM435 million purchase price.

CBRE WTW has appraised the market value at RM435 million, using an income approach (investment method) as the primary valuation basis and a comparison approach as a cross-check. Post-acquisition, Setapak Central is expected to account for roughly 20.7% of KIP REIT’s property assets, lifting total portfolio value by about 26.1% from RM1.66 billion to RM2.10 billion.

Purchase terms and funding mix

Under the conditional sale and purchase agreement (SPA) dated 27 April 2026, FMSB agrees to sell and the trustee agrees to purchase the mall on an “as is where is” basis, free from encumbrances but subject to existing tenancy, occupancy and service agreements, with novation of tenancies to KIP REIT on completion.

Key settlement mechanics:

*Earnest and balance deposits totalling RM43.5 million (10% of the consideration) have been paid to FMSB’s solicitors as stakeholders.

*The remaining RM391.5 million will be settled within three months from the SPA’s unconditional date, including redemption sums payable directly to the chargee bank and any residual amount to the vendor’s solicitors.

The RM435 million consideration will be satisfied entirely in cash from:

*RM258.2 million in bank borrowings (about 59.4%).

*RM176.8 million in gross proceeds from the proposed placement (about 40.6%), based on the illustrative price of RM0.84 per unit.

Any shortfall in placement proceeds will be funded through a combination of borrowings, issuance of debt or hybrid instruments, and/or internally generated funds, having regard to future gearing and working capital needs.

Placement: Up to 220 million units, including undertakings

The proposed placement covers up to 220 million new units, representing approximately 22.95% of the 958.63 million units in issue as at 30 June 2026. Bursa Malaysia Securities has approved the listing and quotation of the placement units on the Main Market, subject to standard conditions.

Allocation framework:

*Up to 30,000,000 units to Datuk Ong Choo Meng.

*Up to 10,000,000 units to Datuk Ong Kook Liong.

*Up to 180,000,000 units to independent investors to be identified later, who must qualify under Schedules 6 and 7 of the Capital Markets and Services Act 2007.

Placement units will be priced via bookbuilding, at an issue price to be determined later. For illustration, the circular uses RM0.84 per unit, representing a 2.43% discount to the five-day VWAP of RM0.8609 up to the last trading day before SPA signing, which would raise gross proceeds of RM184.8 million.

Choo Meng and Kook Liong (the “Undertaking Parties”) have given irrevocable undertakings to subscribe for their respective allocations on the same pricing terms as independent investors. UOB Kay Hian, as principal adviser and placement agent, states in the circular that it is satisfied the Undertaking Parties have sufficient resources to fulfil these undertakings.

Proceeds are earmarked as follows (based on the RM0.84 illustration):

*RM176.8 million – partial settlement of the purchase consideration.

*RM8.0 million – estimated transaction expenses, including trustee and manager acquisition fees, professional and placement fees, regulatory charges and other costs.

Pending utilisation, proceeds will be placed in interest-bearing deposits or other permissible short-term instruments.

Advance distribution and ranking of new units

To preserve distribution entitlement for existing unitholders during the transition, the board intends to declare an “Advance Distribution” for a period up to a date before the placement units are allotted. Placement units will not participate in this advance distribution.

Once issued, the new units will rank pari passu with existing units in all respects, save that they will not be entitled to any distributions declared before their allotment date.

Accretion, risks and dispute safeguards

The manager expects the proposed acquisition to be accretive to distribution per unit (DPU) yield over the long term, in line with its objective to provide regular, stable and growing income distributions. Pro forma figures in the circular show portfolio enlargement and increased contribution from retail assets while maintaining gearing at a level the board views as prudent.

The circular outlines key risk factors, including:

*Conditionality and timing risks around completion of the acquisition.

*Funding and interest-rate risks.

*Tenant payment and non-renewal risks.

*Building defects, regulatory compliance issues and competition from other malls.

*Insurance risks and potential shortfalls.

*The illustrative nature of pro forma distributions and DPU.

*An ongoing dispute between FMSB and the joint management body (JMB Zetapark) over maintenance, the sinking fund and late payment charges.

*Compulsory acquisition risk by the government.

On the dispute, the SPA includes mechanisms such as retention sums, vendor indemnities and provisions addressing any judgment sums, aimed at limiting KIP REIT’s financial exposure. The circular notes that the dispute relates to charges and does not affect ownership of the subject property.

Interested parties and board view

The proposed acquisition is not categorised as a related party transaction; none of the directors, major shareholders or chief executive of the manager, major unitholders of KIP REIT or persons connected to them has any direct or indirect interest in the acquisition.

For the placement, Choo Meng, Kook Liong, Ong Tzu Chuen and Ong Pui Shan are deemed interested parties. They will abstain, and undertake to ensure persons connected to them also abstain, from voting on the placement resolutions at the unitholders’ meeting. Interested directors have abstained, and will continue to abstain, from deliberating and voting on the placement at board level.

The board recommends that unitholders vote in favour of both the proposed acquisition and the proposed placement.

Barring unforeseen circumstances, KIP REIT expects the proposals to be completed by the fourth quarter of 2026.

..........

Read about emerging trends, data-backed insights, growing subsectors, and expert commentaries in EdgeProp print. Subscribe now for your free copy!

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.