Ajinomoto Malaysia’s property pivot from urban KL to Seremban industrial

PETALING JAYA (July 10): Ajinomoto (Malaysia) Bhd’s proposed RM20 per share privatisation plan in a recent Bursa Malaysia filing has drawn attention to a transformation that began years before the offer itself. Over the past several years, the company has reshaped the real estate underpinning its business, exchanging a mature urban industrial property in Kuala Lumpur for a purpose-built manufacturing campus in Bandar Enstek, Seremban, Negeri Sembilan. The proposal has therefore become not only a corporate exercise, but also a question of how the market values a business whose principal property asset has fundamentally changed.

The RM408 million monetisation

For decades, its site in Jalan Kuchai Lama represented Ajinomoto Malaysia’s principal real estate asset: a sizeable leasehold tract hosting its factory and head office in a city-fringe industrial pocket of KL.

As the city expanded and transit links improved, the property increasingly became more valuable for its redevelopment potential than for its continuing use as a seasoning factory, and the company ultimately chose to realise that value.

In 2023, the company disposed of six contiguous parcels on the Kuchai Lama site for RM408 million in cash, and subsequently declared a special single-tier dividend of RM2.12 per share, returning part of the proceeds directly to shareholders.

The disposal effectively marked the point at which the accumulated land value embedded in that legacy industrial holding was realised, and it coincided with the company’s broader transition towards its new manufacturing base in Bandar Enstek, a modern, fast-growing township located in the Labu sub-district.

The Enstek smart factory

The result is a shift in the nature of the assets underpinning the business. Property value has migrated from land whose value increasingly reflected redevelopment potential to manufacturing infrastructure designed to generate operating returns.

The replacement for Kuchai Lama is not another landbank, but a different kind of property altogether. If the KL site derived much of its later value from location, the Bandar Enstek campus derives its value from production infrastructure. It is an operating asset whose economic purpose is to manufacture, store and distribute products efficiently, rather than to capture future redevelopment gains.

Ajinomoto’s new facility sits within the Bandar Enstek Halal Hub on approximately 18.6 hectares of freehold land. The campus combines manufacturing lines, warehousing, logistics and administrative operations in a single integrated environment. Ajinomoto describes the facility as incorporating automation, digitalisation and green-building features to improve operational efficiency and meet halal standards.

Ajinomoto Malaysia’s Bursa financial results filing dated May 26 shows property, plant and equipment of just over RM450 million as at March 31, together with modest right‑of‑use assets, reflecting the new factory and associated infrastructure as the centrepiece of the company’s physical asset base. Outside Bandar Enstek, the group owns only a small legacy shophouse in Batu Pahat; other sales branches and depots operate from leased premises.

New infrastructure begins to earn its keep

The first full financial year following the completion of the manufacturing transition suggests that the reshaped asset base has begun translating into stronger operating performance.

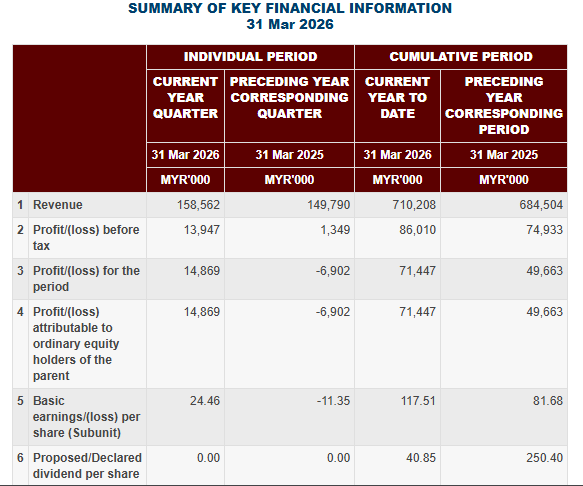

According to its results up to March 31, revenue increased to about RM710 million from RM684 million a year earlier, while operating profit rose nearly 18% to around RM79 million from RM67 million. Profit before tax climbed to RM86 million from RM75 million, and profit after tax increased about 44% to RM71 million, with basic earnings per share rising from roughly 82 sen to about 118 sen, as announced in a Bursa filing dated May 26.

In its segment commentary, the company highlighted higher domestic sales of AJI‑NO‑MOTO®, Tumix and Seri‑Aji on the consumer side, and stronger volumes of industrial seasoning products on the industrial side. It also noted that export revenue was negatively affected by a weaker US dollar against the ringgit, but that operating profit improved on higher sales and lower key raw material, selling and administrative costs.

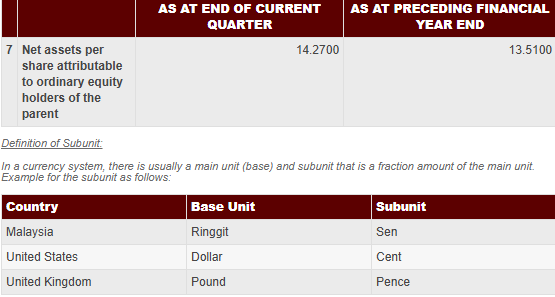

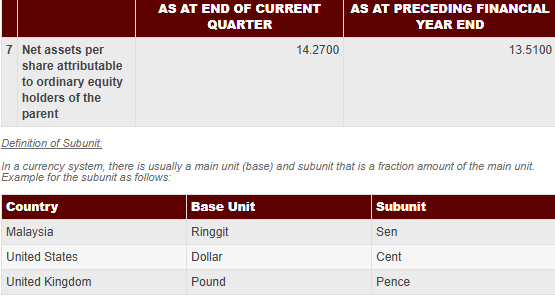

On the cash-flow side, Ajinomoto Malaysia generated more than RM90 million of net cash from operating activities in FY2026. It continued to invest in property, plant and equipment and intangible assets, while disclosing RM11.2 million of contracted but unprovided capital commitments for plant and equipment. At the same time, it reported no borrowings or issued debt securities, and carried around RM274 million in liquid investments and RM74 million in cash and bank balances, for total cash and equivalents of roughly RM348 million. Net assets per share stood at RM14.27, up from RM13.51.

Viewed together, these figures are consistent with a company that has moved beyond the peak of its investment cycle and is beginning to harvest returns from a modern, largely built‑out manufacturing campus. Earnings are higher, operating cash flow is strong, capital commitments are modest, and there is no leverage on the balance sheet.

RM20 offer price implies equity value of RM1.22 billion

On June 22, Ajinomoto Co Inc formally proposed privatising Ajinomoto Malaysia via a selective capital reduction (SCR) and repayment exercise at RM20 per share for all shares not held by the parent. The Malaysian board has acknowledged the proposal, appointed a principal adviser, and engaged an independent adviser to opine for non‑interested directors and disinterested shareholders. The transaction will require the usual SCR thresholds: strong approval from minorities and limited opposition.

At RM20, the offer price implies an equity value of about RM1.22 billion. Once Ajinomoto Malaysia’s net cash of roughly RM348 million is stripped out, the implied enterprise value sits around RM870 million. On FY2026 numbers, that translates into an EV/Ebitda (enterprise value divided by earnings before interest, taxes, depreciation and amortisation) multiple in the high single digits and a price of roughly 1.4 times net assets per share.

The valuation can be viewed in different ways. Some investors may regard it as relatively modest for a debt-free consumer business with a newly configured production base and substantial cash reserves, while others may focus on the premium to historical trading levels and the undisturbed share price. For property-focused investors, however, the valuation debate is inseparable from the transformation of the company’s underlying asset base.

Timing of bid follows structural asset overhaul

The proposed privatisation comes after that shift has largely been completed and after the first full year in which the new infrastructure’s benefits are visible in earnings, cash flow and a strengthened, debt‑free balance sheet.

For minority shareholders, the decision is therefore not simply whether RM20 per share represents an attractive premium, but whether it appropriately reflects a business whose principal property asset has already evolved.

The Kuchai Lama site was, by the end, an urban industrial property whose rising worth reflected its location and redevelopment potential, and whose value was ultimately realised through a RM408 million sale and a special dividend. The Bandar Enstek campus is a different proposition — an integrated manufacturing platform on freehold land within a halal hub, designed to generate long‑term operating returns rather than speculative land gains.

..........

Read about emerging trends, data-backed insights, growing subsectors, and expert commentaries in EdgeProp print. Subscribe now for your free copy!

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.