Evolving with the tide: How real estate family offices can navigate the shift from developer to institutional investor

According to a recent Knight Frank report, Malaysia’s private wealth deployment landscape is undergoing a structural transformation. The shift is increasingly visible in the growing role of private capital alongside traditional financing channels, including large‑ticket transactions and the emergence of structured family office frameworks such as Johor’s Single‑Family Office (SFO) regime in the Forest City Special Financial Zone.

For patriarchs who built fortunes in bricks and mortar, this shift demands a recalibration of financial philosophy. Traditional property development is a linear, highly concentrated game built on leverage and binary project outcomes. A modern family office, by contrast, operates in a diversified, liquidity‑aware environment where performance is measured on a risk‑adjusted basis. Moving from developer to investor is increasingly becoming a practical consideration for long‑term wealth preservation.

Unpacking the real estate family office: The Sdn Bhd reality

To grasp the scale of this pivot, it helps to strip away institutional jargon and examine a typical Malaysian real estate family office (REFO) as it actually exists.

Legally, such vehicles may, for certain proprietary investment activities involving family capital, rely on exemptions under Schedule 3 of the Capital Markets and Services Act 2007 (CMSA). Most real estate family offices begin life as privately held Sdn Bhds operating as boutique or mid‑sized developers.

Instead of allocating capital into liquid global markets, this Sdn Bhd developer behaves like an operating company. It pools family cash to anchor raw land banks, fund heavy capex, and carry illiquid, unlisted real estate on its balance sheet. This hands‑on builder mindset, coupled with a standard corporate structure, can create structural vulnerability when the family attempts to preserve wealth across generations.

The developer’s dilemma: Why status quo threatens wealth preservation

In today’s environment, three embedded vulnerabilities stand out for Sdn Bhd families:

1) Hyper‑concentration risk

A developer may lock up 80–90% of the family’s net worth in one land parcel or a handful of active sites. Any serious delay, dispute or regulatory bottleneck can effectively immobilise the entire balance sheet.

2) Leverage as an amplifier

The development model leans heavily on bridging loans, term loans and large facilities. In a world of shifting rates and tighter credit, heavy leverage amplifies the impact of any project‑level disruption on the family’s capital base.

3) Binary, disrupted cash flow

Projects consume capital upfront and only generate cash years later—if sell‑through succeeds. This binary, cyclical cash pattern clashes with the family office’s need for predictable liquidity to fund operations, lifestyles and multi‑generational liabilities.

By shifting towards a multi‑asset investor stance, a family moves from absorbing localised, binary project risks to allocating diversified global growth risk. Done properly, this evolution strips away systemic vulnerabilities of debt and illiquidity, aimed at reducing the risk that volatile development profits undermine a more resilient wealth structure.

To cross this operational chasm, a transforming developer must anchor its transition on three pillars of strategic maturity: redefining valuation around liquidity, building a disciplined capital architecture, and using proprietary capital to build market credibility and track record.

Pillar 1 – Rejecting the illusion of paper valuation

In property, a land bank “valued” at RM20 million can still take 12–24 months to sell in a downturn — often at distressed discounts. In broader markets, valuation remains theoretical until backed by systematic liquidity.

Modern family offices often treat liquidity as an active risk‑mitigation tool, not mere cash drag. Many secured SFOs maintain a defined allocation to T+3 exit‑ready instruments, such as wholesale corporate money market funds or institutional fixed income. This liquid anchor generates immediate cash yields to fund overheads, aimed at reducing the risk that the company faces an existential cash squeeze or is forced to liquidate long‑term assets prematurely.

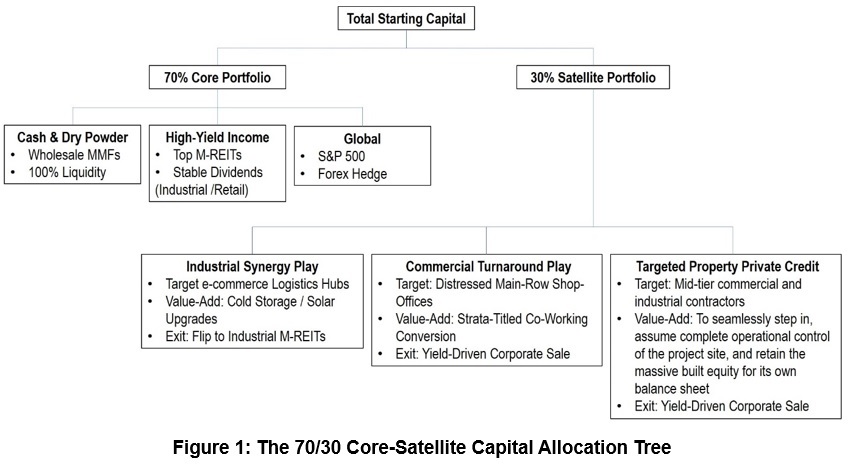

Pillar 2 – Leveraging the ‘circle of competence’ with a 70/30 blueprint

A common trap in transition is either abandoning real estate entirely for fashionable, unfamiliar assets, or falling back into overpaying for low‑yield physical property out of comfort.

Here is one possible framework illustrated using a strict 70/30 core–satellite discipline:

a) The core portfolio (70%) focuses on liquidity, capital preservation and predictable yield. Its purpose is to fund operations reliably and protect generational capital.

b) The satellite portfolio (30%) leverages the firm’s specific edge in construction and development to generate higher‑risk, higher‑alpha returns.

Core portfolio – low‑to‑medium risk ‘dry powder’

This bucket might include:

c) Tactical asset‑backed income (Malaysian REITs)

Exposure to industrial, logistics and prime retail REITs (for example, selected Malaysian industrial, logistics and retail REIT vehicles) with illustrative annual distribution ranges of around 5.5–7.0%, without direct management or tenant friction.

d) Global macro and currency hedge (US/Singapore ETFs)

Systematic allocation (often via Singapore corporate accounts) to low‑cost ETFs tracking broad indices such as the S&P 500 or MSCI World to hedge ringgit risk and participate in global growth.

e) High‑yield cash engine (wholesale MMFs)

A permanent 15–20% core allocation to wholesale money market funds managed by selected domestic asset managers, with illustrative yields of around 3.5% and T+1 liquidity as ready ‘dry powder’.

Satellite portfolio – leveraging real estate edge

Within the 30% satellite bucket, the SFO intentionally plays where it has informational and operational advantages:

f) Industrial synergy play

Target older single‑storey factories or warehouses in mature zones (Shah Alam, Bukit Raja, Nilai, Pasir Gudang) at or near land value. Use internal construction capability to upgrade clearances, add solar or cold‑storage, stabilise under long corporate leases, with the contributor targeting stabilised yield ranges of around 7.0–8.5% per annum prior to a potential exit to institutional buyers.

g) Commercial shop‑office turnaround play

Acquire distressed, street‑front commercial blocks in dense townships (Subang Jaya, Petaling Jaya, Bukit Jalil, Johor Bahru), then rehabilitate structures, modernise façades and strata‑title into corporate suites, medical clinics or co‑working space. The aim is to lift yields from around 3% to illustrative ranges of about 6.5–8.0% per annum, with valuations reflecting improved income and asset quality.

h) Targeted private credit (bridge loans for builders)

Provide short‑term, asset‑backed bridge financing (RM2–5 million per ticket) to vetted contractors at illustrative returns of around 10–12% per annum, secured by first‑party legal charges. If a borrower defaults, the SFO’s construction competency allows it to step in, complete the project and potentially preserve or recover value through completed equity creation rather than leaving a stranded site.

Pillar 3 – The track record paradox: ‘skin in the game’

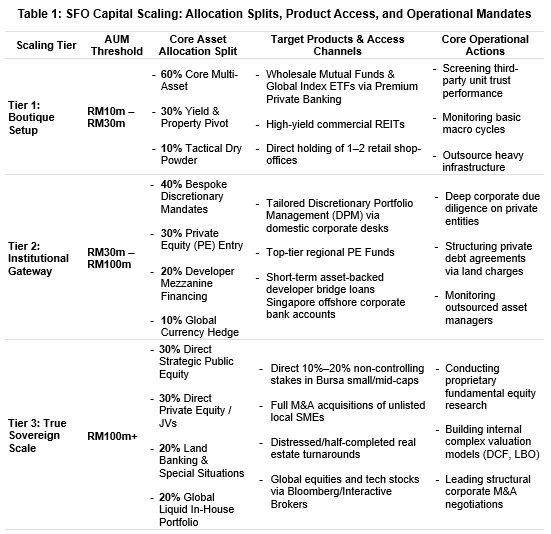

For any SFO seeking to evolve into a licensed fund manager, size and track record become key determinants of reputation.

Institutional allocators and sophisticated investors almost universally expect a demonstrable history of disciplined capital deployment. Crucially, the scale of initial proprietary capital shapes product access, horizons and credibility across three practical tiers:

i) Tier 1 – Boutique setup (RM10–30 million AUM)

Functions like an advanced private holding company. Heavy infrastructure is outsourced; allocation might be ~60% core multi‑asset (wholesale mutual funds, global ETFs via private banking), 30% yield/property pivot (REITs, one or two long‑lease commercial assets) and 10% tactical MMF buffer.

j) Tier 2 – Institutional gateway (RM30–100 million AUM)

At this range, the SFO can negotiate bespoke discretionary mandates with domestic asset managers, access regional private equity funds, deploy 20% into developer mezzanine financing at illustrative asset‑backed returns in the 10–12% range, and maintain a 10% global currency hedge via Singapore offshore accounts.

k) Tier 3 – Institutional scale (RM100 million+ AUM)

At this level the SFO begins to resemble an institutional investment platform, with capacity to acquire direct stakes in Bursa small‑ and mid‑caps, engage in full M&A of private companies, run distressed land‑banking and special situations, and operate an internal global liquid portfolio using professional terminals.

If an SFO launches with too small a capital base, the market may perceive it more as a sophisticated private investment vehicle than as a fully institutional platform, creating operational challenges in scaling. By deploying RM30–100 million of proprietary capital from day one, the firm can iterate its research process and build an audited portfolio before seeking external mandates. When licensing occurs, the SFO presents a concrete track record, not a purely theoretical strategy.

Navigating the regulatory horizons: a three‑phase roadmap

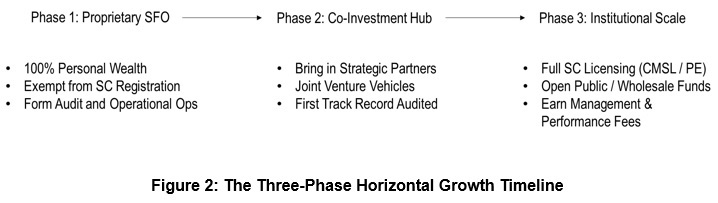

It must be emphasised that the evolution from property developer to sophisticated asset manager cannot be rushed. To manage compliance expectations, limit premature overheads and align institutional infrastructure with AUM, successful firms map growth across three phases:

i) Phase 1 – Proprietary foundation

The SFO may operate as a proprietary investment vehicle relying on applicable exemptions under the CMSA, deploying family capital without raising external public funds. Focus is on building audit systems, research frameworks and governance, and on constructing a verifiable multi‑year track record.

ii) Phase 2 – Co‑investment club

Once operations are stable, the firm invites close high‑net‑worth partners to co‑invest in specific deals via joint ventures or special purpose vehicles. This may involve registration or licensing with the SC under an appropriate category, with the family acting as general partner and typically anchoring 30–50% of each deal to ensure meaningful “skin in the game” while learning third‑party capital management in controlled settings.

iii) Phase 3 – Institutional scale

The firm may pursue a Capital Markets Services Licence (CMSL) or other relevant licensing or registered fund structures, depending on strategy and regulatory requirements, opening the door to corporate treasuries, endowments and other wholesale funds. At this stage, the investment team is operationally separated from dedicated compliance and risk units, and the business model shifts to an institutional fee architecture (for example, around 2% management fee and 20% performance fee), enabling scalable, recurring revenue.

Final outlook

Ultimately, the move from developer to institutional investor is not about abandoning entrepreneurial agility; it is about surrounding that agility with institutional discipline.

Where a developer mindset is driven by project cycles and site‑level execution, an allocator mindset is shaped by portfolio construction, liquidity and governance. By pivoting away from single‑site, high‑intensity project execution and towards systematic, multi‑asset allocation, real estate families can help convert cyclical development profits into a more diversified and potentially compounding wealth base. For Malaysia’s modern property pioneers, survival in the new financial landscape depends less on how aggressively they build—and more on how intelligently they institutionalise the fortunes they have already created.

Editor’s note: Yield ranges and portfolio illustrations cited in this article represent the contributor’s observations and hypothetical frameworks based on market conditions and should not be construed as guaranteed returns or personalised investment advice.

Foo Chee Hung holds a PhD in Urban Engineering from The University of Tokyo, and is the principal researcher of MKH Bhd.

The views expressed are the writer’s and do not necessarily reflect EdgeProp's.

..........

Read about emerging trends, data-backed insights, growing subsectors, and expert commentaries in EdgeProp print. Subscribe now for your free copy!

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.