MRCB close to clinching RM700m DASH contract

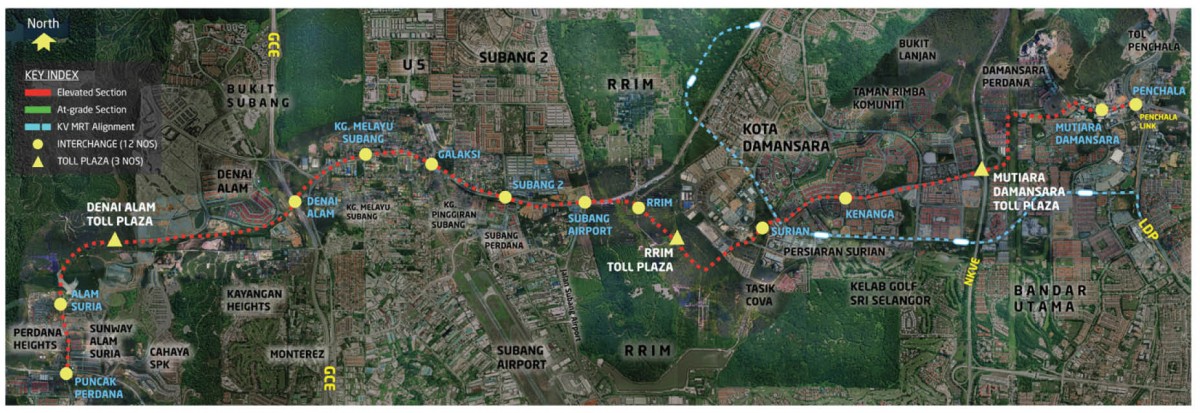

DASH is a 20.1km three-lane dual carriageway connecting Puncak Perdana in Shah Alam to Damansara Perdana in Petaling Jaya. The cost of the project, which is being developed by Permodalan Nasional Bhd’s wholly-owned subsidiary Projek Lintasan Kota Sdn Bhd, is about RM4.2 billion, including land acquisition costs of RM880 million.

If MRCB bags the contract, it will lift the group’s external construction order book, which currently stands at RM6.4 billion, by 11%. This could be a pick-me-up for the group following lacklustre first-quarter earnings due to slower-than-expected property sales.

The group’s share price has fallen 26.8% in less than eight months from a high of RM1.50. The stock closed at RM1.06 last Thursday, giving the company a market capitalisation of RM1.98 billion.

Moving forward, MRCB may become increasingly reliant on its construction arm to prop up earnings, given the growing negative outlook for the property sector. Hence, consistently winning job awards, such as the RM700 million DASH package, will be key to maintaining earnings visibility for the group.

Stripping out the disposal of Nu Tower 2 office tower in Kuala Lumpur for RM31 million, the group posted a core net loss of RM18.9 million for its first quarter ended March 31, 2016 (1QFY2016), which is below consensus expectations of a RM75.8 million profit. Revenue, however, rose to RM436.02 million from RM404.19 million a year ago.

An analyst tells The Edge that it might not be fair to treat MRCB’s asset disposals as mere one-off gains. After all, MRCB is in the business of developing properties, “grooming” them and lastly, disposing of the mature assets. Subsequently, the cash is reinvested in future developments.

While the income may be lumpy and the cycle rather lengthy, it could be seen as MRCB’s business model in the long term, the analyst adds.

Note that the construction of DASH will not start anytime soon, although the award for the work package is expected to be announced in a week or two.

According to one source, MRCB’s portion of the works will run alongside the Rubber Research Institute Malaysia land that is being developed by Kwasa Land Sdn Bhd.

“Of the packages [of the DASH project], this is one of the more attractive ones. The highway is mostly elevated and with the vacant Kwasa Land parcel situated adjacent to the project, construction will be relatively straightforward from a logistics perspective,” says the source, comparing it with work in congested urban areas.

Last week, MRCB announced the disposal of Menara Shell in Kuala Lumpur for RM640 million cash to MRCB-Quill REIT (MQ REIT). The group expects to realise a pro forma net gain of RM138.97 million. Recall that the heads of agreement for the deal was first announced late last year.

Note that MRCB has a 31.25% stake in MQ REIT and that the acquisition by MQ REIT will involve a placement of up to 406.67 million new units by the trust. MRCB will use between RM110 million and RM153 million of the cash from the disposal to acquire some of MQ REIT’s new units.

Overall, the disposal and the subscription for new units are expected to reduce MRCB’s borrowings from RM3.4 billion to RM2.94 billion. The disposal is only likely to be concluded in the fourth quarter of this year.

In a note to clients last Friday, Kenanga Research sees the disposal as positive and estimates that MRCB’s net debt will be reduced to 0.9 times by the end of the year, compared with 1.27 times as at March 31, 2016.

However, the research house reduced its target price for MRCB from RM1.32 to RM1.20 due to the dilutive effect of a proposed share placement by MRCB, which is expected to be completed towards the end of the year. Recall that MRCB last year proposed a share placement of up to 20%. The remaining 257 million shares are to be placed by the end of the year.

“Downside risks to our call include weaker-than-expected property sales, lower-than-expected sales and administrative costs, negative real estate policies and a tighter lending environment,” says Kenanga, maintaining a “market perform” call on MRCB.

At its closing price of RM1.06 last Thursday, MRCB was valued at 18.9 times earnings and 0.84 times net asset value.

Looking ahead, the real rerating catalyst for MRCB will be the long-awaited disposal (entirely or partially) of the Eastern Dispersal Link in Johor Baru, which carries with it the bulk of MRCB’s debt.

This article first appeared in The Edge Malaysia on July 4, 2016. Subscribe here for your personal copy.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.