Higher EPF withdrawals do not solve affordability issues

MOST Malaysians want to own a home, and buying real estate has traditionally been a good inflation hedge. First-time homebuyers might welcome being able to withdraw more money from their Employees Provident Fund (EPF) retirement nest egg to buy a home — if indeed the government raises the withdrawal ceiling (Account 2) to 40% from 30% come Oct 21 when Budget 2017 is tabled in Parliament.

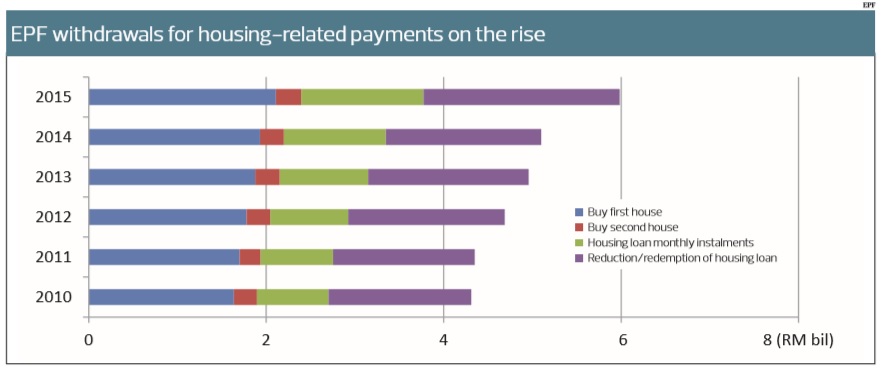

After all, 1.8 million EPF members withdrew nearly RM6 billion in savings from Account 2 in 2015 to buy their first home, second house, service their monthly mortgage payments or pay off their home loans, EPF data show.

At present, 70% of EPF savings (Account 1) can only be withdrawn at age 55, while the remaining 30% in Account 2 can be withdrawn for things that can enhance one’s retirement well-being.

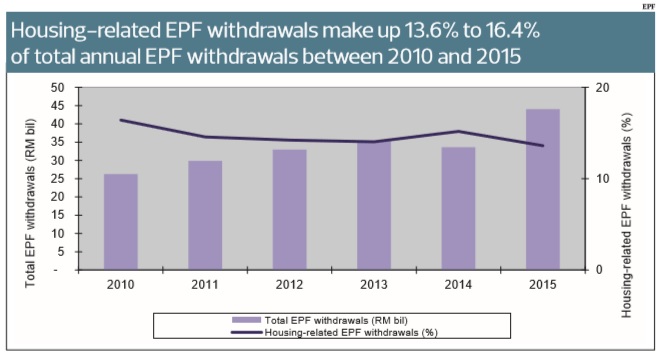

The reliance on EPF money to help with the purchase of one’s first and second house has increased an average of 6.8% a year in the past five years from 2010, when 1.4 million members withdrew RM4.3 billion. The RM5.98 billion in withdrawals last year to buy houses made up 13.6% of the RM44 billion withdrawn by 3.3 million EPF members. Withdrawals to purchase homes made up 13.6% to 16.4% of total annual withdrawals between 2010 and 2015, EPF data show.

Lim Chee Sing, RHB Research Institute executive chairman and chief economist, offers a positive view on the added flexibility: “Allowing higher EPF withdrawals to enable potential house buyers to own a house indirectly forces him or her to commit and save more money for monthly instalments and this asset (house) would likely appreciate in value over time. This, in my view, may not be such a bad thing. Otherwise, he or she may have to incur rental expense on a monthly basis,” Lim says, adding that the asset can be an investment that can be used later as a source of retirement funding.

He is right, but there are potential dangers considering how home prices have increased faster than wages on the back of easy monetary policy globally. Then there is the possibility of income shocks should economic conditions deteriorate significantly.

Lim concurs that allowing higher EPF withdrawals in itself does not address the issue of providing enough affordable homes — which is defined by the World Bank as homes priced at three times annual median household income or less.

For Malaysia, that means house prices need to be below RM165,060, with half of Malaysian households earning RM4,585 a month in 2014. “However, only 21% of new housing launches in Malaysia were priced below RM250,000 in 2014, Bank Negara Malaysia said in its 2015 annual report. In contrast, data points to an oversupply of higher-end properties priced above RM500,000 (36% of total new launches) when these houses are only within the reach of 5.4% of the population, using the affordability threshold.

“To my mind, the idea of bigger withdrawals for house buying is tantamount to treating the symptom rather than the disease. The symptom here is the rising cost of home ownership, while the disease is the artificial shortage of affordable homes,” says Prof Emeritus Datuk Mohamed Ariff, Professor of Economics and Governance at the International Centre for Education in Islamic Finance (INCEIF).

“No doubt, large EPF withdrawals can help potential house buyers, but the price to pay for this facility is huge — namely, eroding the funds meant for old age. The importance of provisions for old age can hardly be exaggerated now that life expectancy is growing with an ageing population. Evidently, the existing EPF arrangements are inadequate, with many retirees reportedly ending up destitute after five years. Additional EPF withdrawals for home buying would only make the situation worse, not better,” adds Mohamed Ariff, who is also a Malaysian Institute Of Economic Research (MIER) distinguished fellow.

He asks that the government “reconsider” the idea of allowing larger EPF withdrawals as a means to solve the country’s housing woes. “This can only provide relief, like Panadol for pain, without addressing the cause of the pain itself. Like the side effects of painkillers, larger EPF withdrawals would take a huge toll on old age provisions later on,” he adds.

Prof Yeah Kim Leng, Professor of Economics at Sunway University Business School, is for home ownership and the buying of property for investment but offers a word of caution on the need for prudent decision-making and financial management.

“Home ownership affects not only current and long-term spending and savings behaviour but also the individual’s future wealth as the property is also an investment... In a rising house price environment, they are expected to be better off if they are able to set aside more of their future income to make up for the EPF withdrawal,” says Yeah, adding that a higher withdrawal threshold would likely “benefit those at the margin” who need the extra amount to make the downpayment and qualify for financing.

“To be better off, the catch is that they do not overspend and get into financial distress as they will have minimal savings in the early part of their career. It is good to allow the individuals to make the decision, but financial risk as well as the ability to manage with a tight budget after paying for the mortgage, will have to be clearly understood,” he says.

In deciding, Yeah reckons that the prospective homebuyer would need to consider expectations on housing supply and demand and price trends: “Owning a house early is advantageous if house prices are on an upward trend. On the other hand, it is an illiquid asset and you may be better off renting in a soft market as a quick or forced sale may result in substantial losses for the owner.”

Whether one should make that EPF withdrawal “depends on the value one places on holding cash”, UOB Malaysia economist Julia Goh says, pointing out that the Bank of England’s chief economist Andy Haldane recently reportedly said property is a better investment for retirement than a pension due to the complicated system in the UK.

Back home, “most people feel that due to inflation, cash shrinks in value so withdrawing from the EPF for the purchase of property is not a bad thing. However, this measure may not be able to assist the broad public given that a large number of people probably would not have sufficient Account 2 savings in the first place,” Goh says.

The central bank put in a word for the man in the street just last month: “Access to financing is not the main problem confronting potential buyers of affordable houses. The fundamental issues that require solutions are affordability and the shortage of supply of reasonably priced houses,” Bank Negara said in a Sept 20 statement to address questions on the extension of housing loan payment periods from 35 to 40 years, which the central bank sees as a measure that “will further add to the total cost of financing without significant improvements in the affordability of one’s monthly instalments”.

RHB’s Lim offers another way to aid housing affordability: “Land cost is usually the single largest component of the cost of a house, so, perhaps the government can also look into providing land at reasonable prices to build affordable houses.”

Reducing other regulatory and compliance costs, such as land conversion fees, land development taxes, stamp duties and permits can also help bring down home prices in the affordable housing segment, Lim adds.

It is also worth noting that EPF dividend rates were above 6% a year between 2011 and 2015 — easily above the prevailing effective lending rates of 4.2% to 5.1% as at Aug 18 this year. Excluding the 4.5% paid in 2008, annual dividends declared ranged from 5% in 2005 to 6.75% in 2014. Presumably, the potential loss of dividend income is expected to be made up by asset value appreciation.

As it stands, more than 78% of the 6.7 million active EPF contributors do not have the minimum recommended savings of RM196,800 for retirement, the EPF’s strategy management head Balqais Yusoff reportedly said in May this year. The RM196,800 is assuming one needs RM820 a month for 20 years, given that the average Malaysian will live to about 75 years old, but most had only about RM50,000, which would run out in five years. While some of these members could well have other assets outside their EPF savings, the adequacy of retirement savings will only become an increasingly important issue as Malaysia is expected to reach the 7% threshold the World Bank defines as an ageing society in just five years in 2021. By 2035, one in 10 Malaysians will be aged 65 and above, official projections show.

Given these demographics, policy action to deliver the one million units of affordable housing promised to reach the market by 2018 to alleviate supply shortage for first-time homebuyers — plus measures to ensure an increased supply of affordable housing by the private sector — would better address the issue at its core.

This article first appeared in The Edge Malaysia on Oct 10, 2016. Subscribe here for your personal copy.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.