Uncertain outlook seen for Gamuda’s key divisions

Gamuda Bhd (May 30, RM3.18)

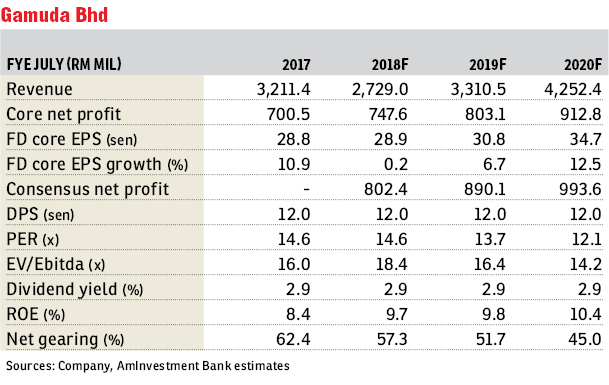

Downgrade to hold with a lower fair value (FV) of RM3.89: We maintain our forecasts for Gamuda Bhd but cut our FV by 35% to RM3.89 (from RM5.95 previously) and downgrade our call to “hold” from “buy”. Our revised FV is based on 12 times 2019 forecast fully diluted earnings per share of 32.4 sen (from sum-of-parts previously), in line with our reduced benchmark target forward price-earnings (PE) of 11 times to 13 times for large-cap construction stocks (from 14 times to 16 times previously).

Amid the uncertain outlook for Gamuda’s key divisions, namely construction (due to the review of megaprojects by the government), property (due to the prolonged sector slowdown) and infrastructure (due to the potential abolishment of highway tolls and the nationalisation of water assets), we believe that the market will derive greater comfort by valuing Gamuda in its entirety based on its near-term earnings potential, namely PE (versus a combination of PE, RNAV and discounted cash flow. This accords more generous valuations to long-term assets such as land bank and concessions that may not be realisable under the current environment).

Prime Minister Tun Dr Mahathir Mohamad told the media on Monday that the Kuala Lumpur-Singapore high-speed rail (HSR) will be scrapped. This means that the project delivery partner (PDP) contract awarded by MyHSR Corp to a 50:50 Gamuda-MRCB joint venture (JV) in April 2018 for Package 1 (North) from Kuala Lumpur to the Melaka/Johor border is now likely to be revoked. (The same goes for the PDP contract for Package 2 (South) from the Melaka/Johor border to the Johor/Singapore border awarded to a YTL-Tabung Haji JV.)

We are keeping our forecasts as we have yet to impute to our numbers any contribution from the project.

While the latest development is negative to Gamuda, it is not totally unexpected. We believe the prospects of the local construction sector have weakened, as the government reconsiders various mega infrastructure projects on grounds of fiscal prudence. Apart from the Kuala Lumpur-Singapore HSR, we believe more megaprojects could potentially be deferred, scaled down or cancelled. Also, the introduction of a more transparent public procurement system to plug leakages will translate into lower margins for players.

Not helping either is the prolonged downturn in the local property market that weighs down Gamuda’s property division, coupled with the uncertainty arising from the potential expropriation of Gamuda’s toll road and water concessions. — AmInvestment Bank, May 30

This article first appeared in The Edge Financial Daily, on May 31, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.