Proposed Johor acquisitions expected to be yield-accretive for Axis REIT

Axis Real Estate Investment Trust (June 8, RM1.54)

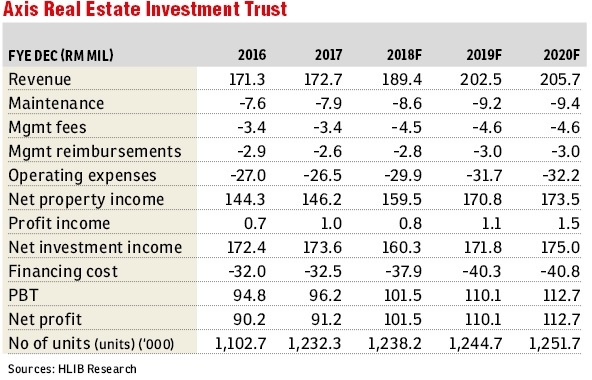

Maintain hold with an unchanged target price (TP) of RM1.44: Axis Real Estate Investment Trust (REIT) has proposed to acquire two industrial properties with a combined area of approximately 251,000 sq ft, situated within Kawasan Perindustrian i-Park, Bandar Indahpura, Kulai, Johor.

The properties are located strategically within one of the main development corridors under Iskandar Malaysia. Each of the property comprises a single-storey detached factory with mezzanine offices and other ancillary buildings. The proposed acquisitions will cost RM38.7 million, to be funded by existing bank facility. They are expected to be completed in the third quarter of 2018.

The properties have 100% occupancy rates as of last Thursday. Upon completion, both properties with a combined lettable area of 166,000 sq ft shall be leased to Beyonics Precision Malaysia Sdn Bhd (BPM) and Oerlikon Balzers Coating Malaysia Sdn Bhd (OBCM) respectively. BPM shall lease the property for a fixed period of 10 years (expiring in 2027) at an agreed monthly rental of RM186,000 for the first three years, while OBCM shall lease the property for a fixed period of seven years (expiring in 2024) at RM43,000 per month, both with options to renew for further terms.

We are positive on the proposed acquisitions as they are yield-accretive, given the net yield of 6.8% and 6.9%, respectively (before Islamic financing cost) versus its current yield of 5.4%. The properties will be fully tenanted under fixed long-lease terms of 10 years and seven years, respectively, which further minimise the risk to Axis REIT. The acquisition price works out to be RM154.40 per sq ft, which is fair for freehold industrial space in Kulai, Johor. Also, the acquisition price of RM38.7 million is lower than the market value of RM40million based on valuations by independent valuers.

Axis REIT intends to utilise debt facility of approximately RM38.7 million from its existing credit lines. Its gearing ratio is expected to increase to 34.1% from the current 33.1%. This is still comfortably below the gearing limit of 50%, leaving room for more future acquisitions.

We maintain our “hold” rating at a TP of RM1.44 based on financial year ending Dec 31, 2018 targeted yield of 5.7%, which is derived from two-year historical average yield spread of Axis REIT and 10-year Malaysian Government Securities. — Hong Leong Investment Bank Research, June 8

This article first appeared in The Edge Financial Daily, on June 11, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.