Latest asset buy seen to have muted impact on Axis REIT’s earnings

Axis Real Estate Investment Trust (Aug 9, RM1.55)

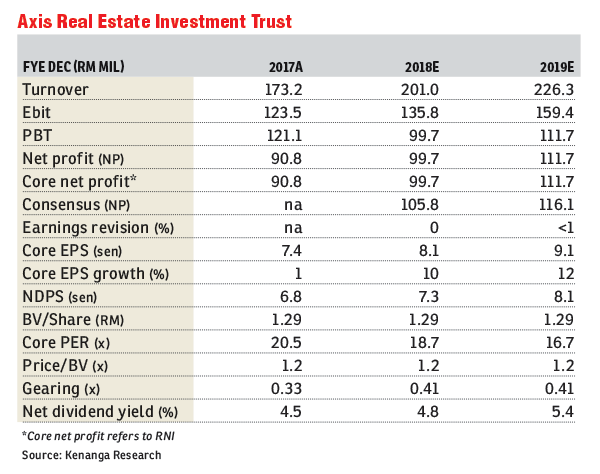

Maintain underperform with an unchanged target price of RM1.25: Axis Real Estate Investment Trust (REIT) via its trustee RHB Trustees Bhd has proposed to acquire an industrial development in Senawang Industrial Park, Negeri Sembilan from Gandour Malaysia Sdn Bhd for a cash consideration of RM18.5 million. The property consists of a three-storey office annexed with a 1.5-storey warehouse factory and other ancillary buildings, and will be tenanted out at 100% occupancy to Nippon Wiper Blade (M) Sdn Bhd for eight years up to 2026. The acquisition will be funded by bank financing and is expected to be completed by end-2018.

The acquisition was well within expectations as Axis REIT had already issued a letter of offer. The asset net yield is attractive at 7.7%, which is at the higher end of Axis REIT’s recent industrial asset acquisitions with net yields ranging from 7% to 7.5%, while Axis REIT’s portfolio net yield stands at 8.2%. We are neutral about this acquisition, as the impact on earnings is rather muted due to the small size of this asset as opposed to Axis REIT’s portfolio (<1% total investment properties of RM2.7 billion). That said, we do favour long-term lease structures on industrial assets versus multi-tenanted office spaces as it ensures long-term earnings stability with less risk of losing tenants, while occupancy is maximised.

On outlook, financial year 2018 (FY18) to FY19 will see minimal leases expiring at 15.4% to 21.3% of portfolio’s net lettable area. We believe the group will likely incur borrowings to fund these potential acquisitions with no plans for cash calls in the near term. FY18 to FY19 growth is expected to be driven by the inclusion of Axis Mega Distribution Centre Phase 1 from June 2018 and its second greenfield for Upeca Technologies Sdn Bhd in Subang by FY19.

Our “underperform” call is premised on our lacklustre outlook on the sector as we remain conservative on valuations, and as most foreseeable positives have already been priced in, while Axis REIT’s gross yield of 5.4% is below large-cap Malaysian REIT peers’ average of 6%. — Kenanga Research, Aug 9

This article first appeared in The Edge Financial Daily, on Aug 10, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.