Scientex to focus on affordable housing, stretch film production

Scientex Bhd (June 27, RM8.63)

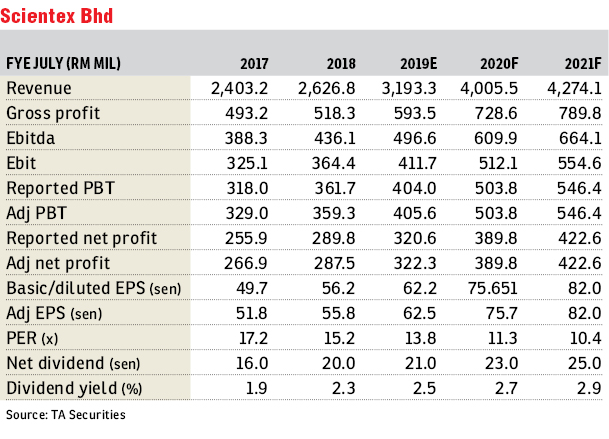

Maintain buy with an unchanged target price (TP) of RM9.80: Scientex Bhd recorded core earnings for the first nine months of financial year 2019 (9MFY19) of RM220.1 million (+17.6% year-on-year [y-o-y]). This represent 68% and 71% of our and consensus’ full year estimates, respectively. We deem the result largely within expectations as we expect lumpy contribution from property segment in the fourth quarter of financial year 2019 (4QFY19).

The group declared a first single-tier interim dividend of 10 sen/share, similar to the amount declared in 3QFY18.

Manufacturing: 9MFY19 revenue improved 25.4% y-o-y to RM1.73 billion driven by: i) newly acquired subsidiary, Daibochi Bhd and Klang Hock Plastic Industries (KHPI); and ii) increasing production of stretch film in Phoenix. The reported operating profit, however, improved by a lesser quantum of 7.5% y-o-y to RM108.1 million mainly due to foreign exchange loss of RM19.8 million against a foreign exchange gain of RM14.4 million in the 9MFY18 period.

Property: 9MFY19 revenue recorded a growth of 15.2% y-o-y to RM581.1 million driven by ongoing projects and new launches in Johor, Melaka, Ipoh and Selangor. Meanwhile, 9MFY19 operating profit improved to RM174.4 million (+12.1% y-o-y). Earnings before interest and tax margin remained steady at 30% (-0.8% y-o-y), in line with management guidance of 28-31%.

We make no changes to our earnings forecast.

Looking forward, management will focus on ramping up production of stretch film in Arizona via a third production line, and KHPI’s plants alongside extracting synergetic value from Daibochi. Note that the Arizona plant had turned profit before tax positive. In longer term, Scientex aims to achieve annual sales of RM8 billion from its manufacturing segment by 2028.

Management guided that the group will continue to focus on the affordable housing segment, which has been receiving good take-up rate. It remains committed to achieving RM1.1 billion worth of new property launches in FY19, with a significant amount of launches taking place in 4QFY19 (entail around 2,000 units across nine launches). Meanwhile, management also raised its FY20 targeted gross development value of new launches to RM1.3 billion (around 4,900 units) from RM1.2 billion (around 4,600 units), to capture the pent-up demand for affordable homes.

We maintain our “buy” call on Scientex with an unchanged TP of RM9.80/share based on sum-of-parts valuation. — TA Securities, June 27

This article first appeared in The Edge Financial Daily, on June 28, 2019.

Click here for more property stories.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.