Tiong Nam expected to face tough competition in Johor

Tiong Nam Logistics Holdings Bhd (July 10, 49.5 sen)

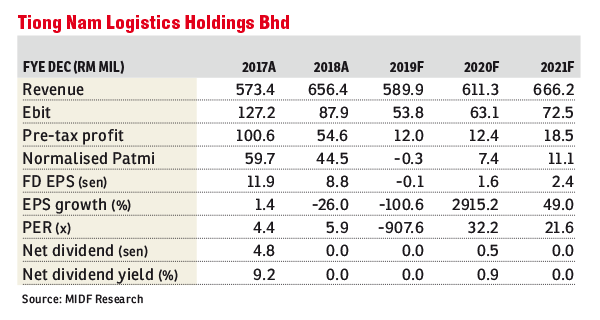

Maintain sell with an unchanged target price (TP) of 41 sen: The contribution of the property development segment to Tiong Nam Logistics Holdings Bhd’s profit before tax (PBT) was more than 45% from financial year 2014 (FY14) to FY18.

However, the property development segment performed poorly in FY19, dragging down the PBT to RM210,000, resulting in the PBT margin for the segment to decline substantially to 0.4% compared with 46% a year ago. This was mainly due to the absence of unbilled sales as of March 31 (versus RM2.2 million during the same period last year) following the completion of the majority of its property development projects.

In the first quarter of 2019, more than 51,000 units of properties were unsold in Johor with an estimated value of RM36.8 million. Johor Bahru, the district in which Tiong Nam’s industrial parks are mostly located in, recorded the highest number of unsold properties with 10,892 residential units, 30,025 serviced apartment units, 1,685 shoplot units and 598 industrial building units.

We believe that Tiong Nam would face tough competition given the expectation of a stagnant property market in Johor. This is due to the fact that other property developers will also have to clear their unsold properties. To give context, Tiong Nam’s total gross development value (GDV) is more than RM400 million.

With no new property development projects in the pipeline except Kota Masai, with a GDV of RM150 million, earnings visibility is clouded. According to the National Property Information Centre and EdgeProp.my, Kota Masai and Pasir Gudang are areas in Johor with low transaction volumes; not more than 1,500 transactions annually in 2018, suggesting low demand for these areas and its surrounding vicinity.

The low number of transaction volumes in both said areas could possibly shelve the launch of Tiong Nam’s Kota Masai project beyond the second half of FY20 as it is located between Kota Masai and Pasir Gudang.

Moreover, the location of Kota Masai which is approximately within 15km from Sungai Kim Kim might be affected by the negative sentiment of environmental pollution there.

The logistics and warehousing segment returned to the black after recording a PBT of RM22.5 million in FY19 compared to the loss before tax of RM1.7 million a year ago with a commendable occupancy rate of 80% for its warehouses. Room for margin expansion exists for the segment due to the addition of new multinational corporation customers and expansion of existing ones which will increase occupancy rate to around 90% in FY20.

Nevertheless, despite our revenue growth assumption of 3% for logistics and warehousing segment in FY20 following the increased client base, we believe it will not be able to boost Tiong Nam’s total PBT to the levels seen in FY14 to FY18.

We are making no changes to our FY20 and FY21 forecasts at this juncture. We opine that the company lacks rerating catalyst in the immediate term, especially in the property segment with a remaining RM400 million of unsold GDV as of March 31. We believe that Tiong Nam will face difficulty in clearing its unsold inventory given that the majority of its property projects are located in Johor.

Moreover its hotel and dormitory segment is still expected to be in the red for FY20. Recall that Johor has the most unsold properties in Malaysia over the last two years. Regarding its plan to list its logistics assets into a real estate investment trust (REIT), maximum yield threshold acceptable by Tiong Nam to list its warehouse assets into a REIT is 6% compared with other REITs which can fetch a yield of around 7% (such as CapitaLand Malaysia Mall Trust and AmanahRaya REIT).

All in, we maintain our “sell” call on Tiong Nam with an unchanged TP of 41 sen per share based on our sum-of-the-parts valuation. A rerating catalyst would be: i) the inclusion of Tiong Nam into the Securities Commission’s list of syariah-compliant securities; and ii) the relocation of companies from China to Southeast Asia if the trade war prolongs. — MIDF Research, July 10

This article first appeared in The Edge Financial Daily, on July 11, 2019.

Click here for more property stories.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.