Axis REIT’s first-half core net income within expectations

Axis Real Estate Investment Trust (Aug 7, RM1.50)

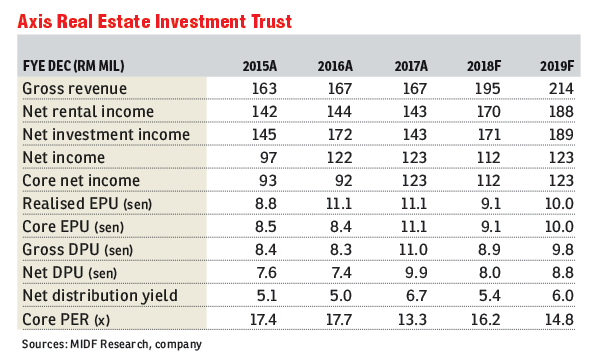

Maintain neutral with an unchanged target price of RM1.55: Core net income (CNI) for the first half of financial year 2018 (1HFY18) was within expectations as Axis Real Estate Investment Trust’s (REIT) core net income (CNI) of RM50.9 million makes up 45.5% of our and 48.4% of the consensus full-year estimates. A gross distribution per unit of two sen was announced for the quarter, which is broadly within expectations.

Its 1HFY18 earnings were up by 10% year-on-year (y-o-y) to RM50.9 million as revenue increased by 10% to RM92.5 million respectively. This was attributed to rental proceeds from the newly purchased assets, namely the Kerry Warehouse and the Wasco facility in Kuantan, as well as a positive rental reversion of its portfolio. Meanwhile, property expenses, non-property expenses and borrowing costs were higher y-o-y by 10.3%, 37.5% and 19.7% respectively.

Second quarter ended June 30, 2018 CNI rose 12% quarter-on-quarter to RM26.9 million on the back of revenue that increased by 5% to RM47.5 million, mainly due to higher non-property expenses in the previous corresponding quarter.

There is a pipeline of potential new assets to sustain mid-term growth. During 1HFY18, Axis REIT completed the acquisition of the Section 28, Shah Alam factory worth RM87 million. Earlier in the year, it also handed over Phase 1 of the Axis Mega Distribution Centre to Nestle Products Sdn Bhd.

Going forward, Axis REIT may see the addition of new assets, including the Senawang factory in Negeri Sembilan that comes with a price tag of RM18.5 million and manufacturing facilities in Indahpura, Johor, worth RM38.7 million in 2HFY18. We have not factored in contributions from these acquisitions. Besides that, Axis REIT is evaluating potential acquisition targets worth a combined value of RM180 million. It also targets to hand over the Axis Aerotech Centre in Subang, which is currently under development, to Upeca in December this year.

Axis REIT’s dividend yield is estimated at 5.4%. We are neutral on the REIT at this point as we expect higher borrowing costs and expenses to offset higher income from new assets. — MIDF Research, Aug 7

This article first appeared in The Edge Financial Daily, on Aug 8, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.