Savills: Millennials are changing the face of retail

Millennial shoppers are poised to become the future mainstream spenders in Malaysia, says Savills Malaysia.

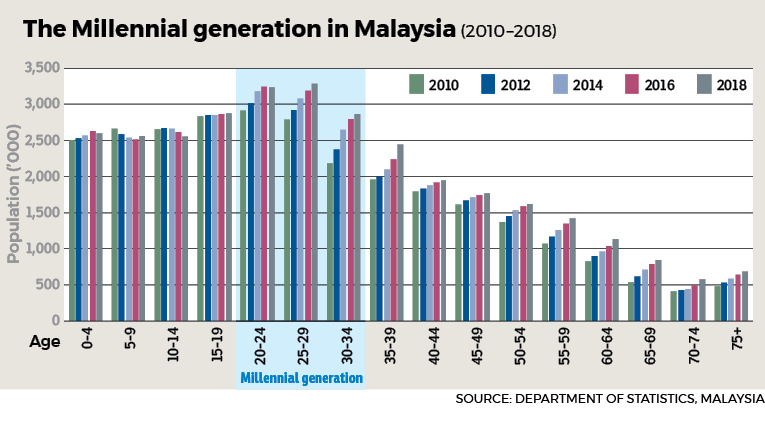

In its “Asian Cities Reports — Kuala Lumpur Retail 1H 2019”, Savills Malaysia points out that the millennial population (aged between 19 and 35 years), who are in their prime spending years, is

estimated to make up 29% or 9.4 million of the total population in Malaysia.

To cater to this emerging consumer group, retail pattern has slowly shifted into a combination of both e-commerce and physical stores. “It is a combination of both, providing millennials with in-store experiences along with the ease of shopping online,” the real estate consultancy notes.

Gone are the good old days, it says, when a mall could depend on big and popular brands to attract shoppers. Instead, food and beverage offerings will remain the main crowd-pullers, providing venues for social as well as economic interaction.

Intense competition

More incoming malls are anticipated to further dilute the market in Greater KL (comprising KL city and Klang Valley suburbs) as most malls will be offering similar goods and services. “This means that retailers will continue operating their businesses in a challenging environment,” the report states.

In fact, intense competition from new malls has already led to some older malls suffering drops in footfall due to their limited choice of retailers and product offerings, and in some cases, poor management and maintenance.

The large number of retail spaces in the pipeline, says Savills, have forced mall operators to re-think the key factors that affect attractiveness of a mall to shoppers, including location, connectivity, concept, target market, tenant mix, car park spaces, security and cleanliness.

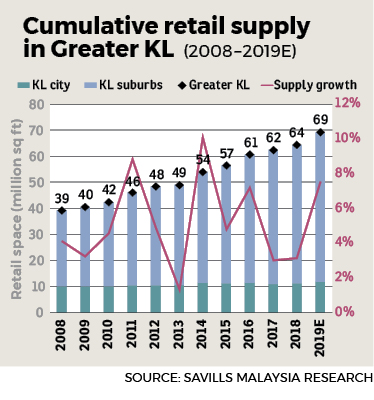

In 2018, the total retail supply grew by 3.1% y-o-y overall in Greater KL, pushing total retail stock up to 64.3 million sq ft of which suburban areas have the highest share of 82%.

Greater KL saw 2 million sq ft of new retail space supply last year bolstered by seven new completions, two of which are in the city centre while the remaining five are in the suburbs.

The seven new malls include Parkson M Square, Puchong (350,000 sq ft); Evo Mall, Bandar Baru Bangi (240,000 sq ft); KL Eco City Mall, Jalan Bangsar (250,000 sq ft); Eko Cheras, Jalan Cheras (600,000 sq ft); Kiara 163, Mont Kiara (300,000 sq ft); Shoppes at Four Season Place, Jalan Ampang (200,000 sq ft); and GMBB, Jalan Robertson (109,000 sq ft).

More malls to come

And it looks like new mall openings will continue unabated despite consumers’ cautious approach to retail spending. Incoming mall supply in Greater KL is projected to increase at a compounded annual growth rate (CAGR) of 7.6% from 2018 to 2022. A total 4.8 million sq ft of lettable retail spaces are projected to be completed this year in Greater KL, according to Savills Research. Major projects include Tropicana Gardens Mall in Kota Damansara and Central i-City in Shah Alam, which was opened in April.

By end-2022, Savills Malaysia estimates that retail space stock will balloon to 78.4 million sq ft if all 18 projects currently under construction are completed on schedule.

These future malls including Lendlease’s The Exchange Mall at Jalan Tun Razak,

Pavilion Damansara Heights, Mitsui Shopping Park Lalaport at Pudu and Pavilion Bukit Jalil will likely hugely impact the performance of the older and less trendy retail malls.

Second line malls struggle

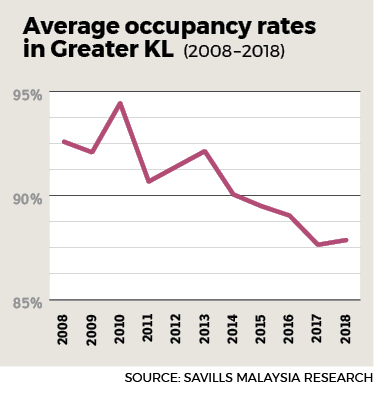

Average occupancy rate of retail malls in Greater KL edged up by 0.2% y-o-y to 87.8% in 2018. Well-established, prime regional malls and megamalls continued to enjoy an average occupancy of over 90%.

In contrast, neighbourhood malls and some recently opened malls have struggled to achieve high occupancy rates, mainly due to the many location choices for retailers to select from. Retailers are taking this opportunity to carefully assess suitable timings and locations for new stores.

Most of the new retail malls opened since 2017 have been slow in attracting sufficient number of retailers, resulting in an average occupancy of less than 80%.

However, the Savills report states that the issue of retail oversupply is usually location-specific, and does not affect less-affluent suburbs.

Small and mid-sized neighbourhood malls of over 20 years old have been able to maintain solid occupancy of above 85%. Their strength lies in their locations, which are all in densely populated areas. Some examples are Ampang Point, Cheras Leisure Mall, Bangsar Shopping Centre, IOI Mall Puchong, Subang Parade, Amcorp Mall and Plaza Alam Sentral.

Meanwhile, tired-looking retail malls are stepping up by undergoing refurbishment and repositioning to meet consumer and retailer requirements.

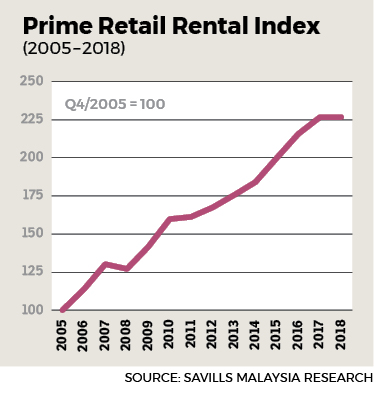

Due to the large amount of retail supply, rental growth in non-prime areas have been limited. Nevertheless, rental levels across all prime retail segments are expected to remain stable despite the challenging environment.

The prime retail index remained flat at 227 points in 2018. Prime rents for malls in KL’s Golden Triangle such as Suria KLCC and Pavilion KL are said to have reached a high range of RM220 psf per month and RM110 psf per month, respectively.

In the suburbs, 1Utama and Sunway Pyramid recorded the highest average prime rent of RM55 psf per month, while Mid Valley Megamall commanded rents as high as RM80 psf per month.

This story first appeared in the EdgeProp.my pullout on June 21, 2019. You can access back issues here.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.