Is there more upside for REITs on expectation of another rate cut?

CONTRARY to the expectation of most economists, Bank Negara Malaysia cut the overnight policy rate (OPR) by 25 basis points to 3% last Wednesday, following its counterparts from Indonesia, Singapore and Taiwan. It was the central bank’s first rate cut since 2009, after the global financial crisis. Its readiness to support short-term growth via monetary easing has been viewed positively by the market — the ringgit has since appreciated 0.6% to 3.957 against the US dollar.

CONTRARY to the expectation of most economists, Bank Negara Malaysia cut the overnight policy rate (OPR) by 25 basis points to 3% last Wednesday, following its counterparts from Indonesia, Singapore and Taiwan. It was the central bank’s first rate cut since 2009, after the global financial crisis. Its readiness to support short-term growth via monetary easing has been viewed positively by the market — the ringgit has since appreciated 0.6% to 3.957 against the US dollar.The surprise rate cut has prompted Hong Leong Investment Bank Research and UOB Kay Hian to upgrade Malaysian real estate investment trusts (M-REITs) to “overweight”, citing a wider spread between the yields of REITs and Malaysian Government Securities (MGS). Furthermore, both research houses believe there could be more easing, either through a further rate cut or the relaxation of property cooling measures.

As most M-REITs have a significant portion of their borrowings locked in at fixed rates, analysts do not expect the rate cut to translate into significant interest savings for them and thus, have kept their earnings estimates unchanged. Instead, the analysts have adjusted the sector’s valuation upwards by reducing the MGS yield assumption from 4% to 3.5%, resulting in target prices that are 4% to 14% higher.

Kenanga Research, which has a “neutral” call on the sector, increased the target prices of M-REITs under its coverage by between 3.6% and 17.6%, and upgraded KLCCP Stapled Group to “outperform” for its asset stability and low gearing.

“We have lowered our 10-year MGS target to 3.60% from 3.80% as the OPR rate cut has materialised, while a US Fed rate hike may be postponed to 4Q2016 or highly likely by CY2017. Going forward, our in-house view is that there may be another rate cut by 2017, depending on Bank Negara’s economic assessment,” it says in a July 14 note.

In a report to its clients last week, UOB Kay Hian says, “The last time Bank Negara cut the OPR in February 2009, MGS yields took a dive from the peak of 4.1% to a low of 3.7%. Recently, MGS yields experienced another collapse from 4.2% at the beginning of the year to 3.6% after Brexit and the OPR cut. We opine that the decline in MGS yield will create a wider spread between REIT and MGS yields, and hence make REITs more appealing.”

It is worth noting that the day after the OPR cut, Bank Negara governor Datuk Muhammad Ibrahim said there are no plans for more cuts over the next few meetings. But he stressed that the Monetary Policy Committee would look at data objectively before deciding.

Safe haven in uncertain times

After the Brexit vote on June 23, there was a growing belief that Bank Negara could resort to lowering the OPR as expectations of an interest rate hike by the US Federal Reserve had eased. Anticipating a rate cut in July as the external environment had become less adverse for a cut, JP Morgan was among the first houses to upgrade M-REITs to “overweight”.

“The trigger for a change in tone in Bank Negara in July would be Brexit and weak April credit data, as these shocks would likely create downside pressure for the 4.0% to 4.5% GDP (gross domestic product) growth target for this year. We upgrade M-REITs to ‘overweight’ as we expect investors to seek resilience amidst a risk-off trade. [M-REITs] offer decent yields of 5.0% to 5.5% for CY2016 and CY2017, with up to mid-single-digit rental revisions after taking into account consumption weakness,” says JP Morgan in a June 28 note.

RHB Research, which also upgraded M-REITs to “overweight” in early June after 1Q results were released, believes there are still downside risks of domestic economic growth slowing more than expected, which may prompt an interest rate cut in the second half of this year. The research house opines that a rate cut would be a strong catalyst for investors to switch to REITs.

“In tandem with the changing expectation on interest rate hikes in the US, and as more countries are moving into new negative interest rate frontiers, high dividend yield stocks are poised to benefit from the expected widening yield spread. Given the relatively lower risk profile compared with high dividend yield stocks, the REITs have the advantage of offering less price volatility and consistent dividend payments,” RHB Research says.

“Currently, the average dividend yield for M-REITs is around 6.0% to 6.5%, compared with 5.3% during its peak valuations in 2012 and 2013. Hence, we believe there is still upside potential for price appreciation of the M-REITs in the coming months. The large-cap REITs that we cover have recorded consistent dividend yields of 5% to 6% since their listing, and we expect the yield to be sustained even if rental reversions were to slow down,” it adds.

REITs with strong sponsors preferred

“Given the challenging domestic economic growth outlook, we anticipate that acquisition opportunities for REITs will be limited due to the scarcity of quality property assets in the market. The situation is not helped by the looming supply of new retail malls in Malaysia, especially within the Klang Valley. Therefore, in this market, we would prefer malls with strong sponsors, which would give more visibility to future asset injections into the respective REITs and ensure sustainable portfolio growth.”

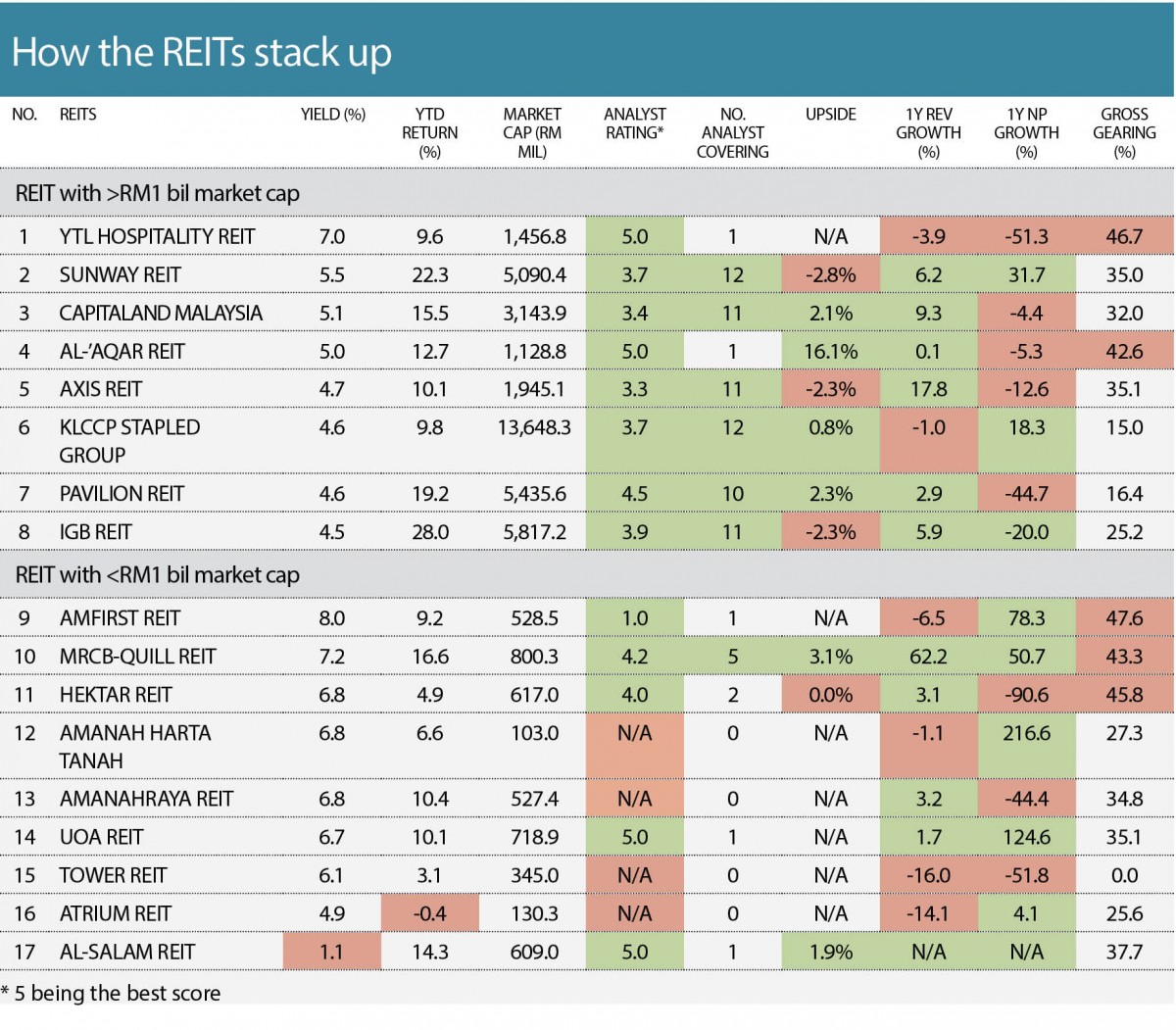

RHB Research says REITs that are backed by solid sponsors include Sunway REIT, Pavilion REIT, KLCCP Stapled Group and MRCB-Quill REIT. It highlights that Sunway REIT has the most visibility in terms of potential asset injections given its strong pipeline of assets with an estimated value of between RM2 billion and RM3 billion, which could be injected over the next two to three years.

“As for Pavilion REIT, its pipeline of assets over the medium term include Elite Pavilion mall, Fahrenheit 88 and possibly Pavilion Bukit Jalil City and Pavilion Damansara Heights. As for KLCCP Stapled Group, its sponsor KLCC Holdings is currently developing Lots 91, 185, 176 and 167 (K) in the KLCC area into an office tower, luxury hotel and retail podium. The development is expected to be completed by the end of 2019.

“MRCB-Quill REIT, meanwhile, should stand out as an office REIT, given its dual-sponsor structure and the strong backing of Malaysian Resources Corp Bhd and Quill Group. It is currently in the process of acquiring Menara Shell from MRCB for RM460 million, which would increase the total property value of the REIT by 41% to RM2.2 billion,” the research house says.

For UOB Kay Hian, IGB REIT remains its top pick as it has the lowest earnings risk due to solid rental reversion and the highest retail sales. In the longer term, the sponsor of IGB REIT is constructing Mid Valley SouthKey Megamall, which is expected to be completed in 2018 and, eventually, be injected into IGB REIT.

However, not every research house is positive about the sector. CIMB Research is of the view that M-REITs’ share prices have largely priced in the yield-seeking sentiment of investors and lower interest rate expectations (an average year-to-date return of 17%) as yields have already compressed to an average of 5.0% to 5.3%.

This article first appeared in The Edge Malaysia on July 18, 2016. Subscribe here for your personal copy.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.