High household debt the elephant in the room

THERE is a big elephant in the room and it is Malaysia’s household debt — among the highest in Asia. And this could get worse if property developers start offering housing loans to homebuyers who have difficulty obtaining a mortgage from banks.

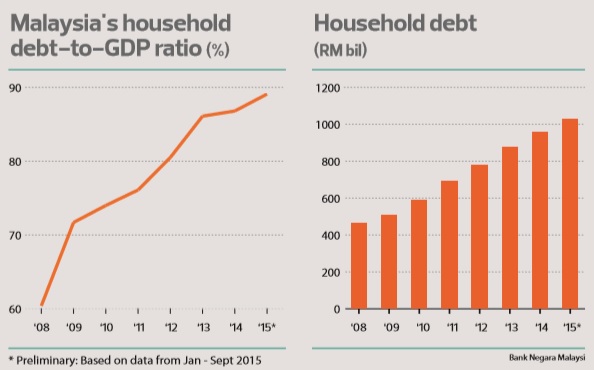

A frightening fact is that Malaysia’s household debt-to-GDP ratio stood at 89.1% last year.

Already, there are concerns that individuals with low creditworthiness will take up more loans, increasing the threat of ballooning subprime mortgages — which reached crisis level in the US in 2008.

On complaints that a tighter lending policy has affected property sales, Bank Negara Malaysia has made its stance clear. It said in July that there are more fundamental issues confronting potential homebuyers than limited access to funding. These include affordability and a shortage of reasonably priced houses, the central bank pointed out.

It maintained that first-time homebuyers continued to have access to financing and it had the facts and figures to prove its claim: Outstanding housing loans recorded a growth of 10.6% as at end May 31, while about 1.5 million borrowers, or 75% of borrowers with housing loans, were first-time homebuyers.

The central bank reiterated that all loan applicants who fulfilled the credit criteria and could afford to repay the debt would have access to credit.

Having property developers offer housing loans could potentially increase household debt, opine industry observers and bankers.

Bank Negara started implementing pre-emptive macro and micro-prudential measures more than five years ago, when the household debt-to-GDP ratio started creeping up and housing prices were soaring.

Reaction to the measures was mixed. Some lauded the move as the central bank ensuring that the country’s banking system was stable while others said the measures were too strict.

“[Loans extended by developers] won’t be counted as a bank loan but, effectively, they create room for higher debt. Any increase in the current household debt level would be a concern,” says a head of research.

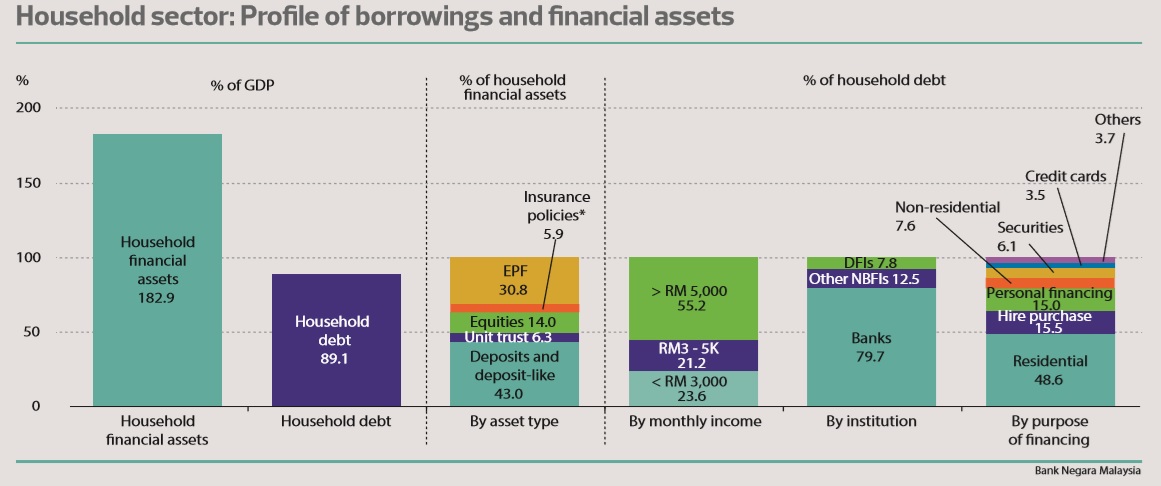

In its financial report for 2Q2016, Bank Negara points out that highly leveraged borrowers in the lower-income group are “beginning to show weaker repayment capacity” in the challenging economic environment.

It notes that banks’ exposure to such borrowers has declined over the years to now account for 19.5% of total bank lending to households (2013: 25.1%).

As for non-bank lending, Bank Negara says lending standards have further reduced the overall proportion of vulnerable household borrowers to 22.6% (2013: 28.4%) of total household debt from banks and non-banks.

Still, the banks and non-bank institutions could be dealt a blow should these loans turn sour, and have a ripple effect on the whole system.

Nonetheless, the central bank adds that “most household borrowers have some flexibility to respond to income shocks and rising living expenses”.

Interestingly, in 1Q2016, the ratio of impaired household loans rose to 1.7% of total household loans by banks and non-banks from 1.6% in 4Q2015.

According to Bank Negara’s financial report for 1Q2016, the increase in impaired household loans was due to the weaker repayment capacity of borrowers who were reliant on cyclical income sources, such as commissions.

“Risks of a broader deterioration in the performance of household loans appear contained as overall household delinquencies improved to 1.4% of total household borrowings (4Q2015: 1.5%),” the central bank states in its 1Q2016 quarterly bulletin.

In 2Q2016, household delinquencies remained unchanged at 1.4% while impairment improved to 1.6% of total household debt from 1.7% in 1Q2016.

The central bank’s statistics also reveal that the growth of household debt slowed at the end of 2Q2016, increasing by 6.2% compared with 8.3% in 2Q2015. The main driver of household debt continued to be house financing, states the central bank. Home loans made up the largest component of household debt at some 49%.

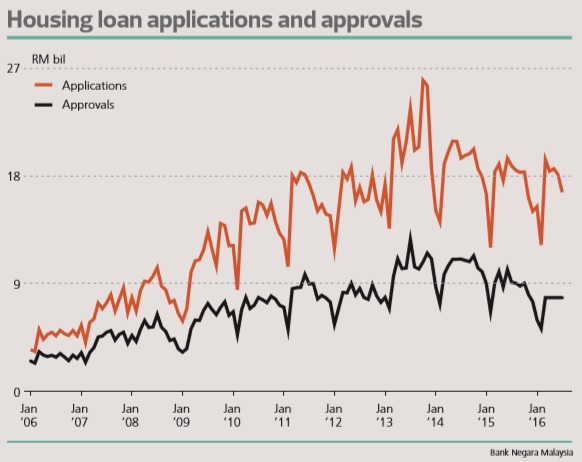

According to Bank Negara’s statistics, loan approval remained weak, contracting 19.4% year on year in July. The data also shows the approval for household loans continued to contract — down 20.8% y-o-y in July.

UOB Kay Hian Research in a Sept 1 note says that was the 18th consecutive month of approval contraction for household loans with -21.5% y-o-y for residential properties and -24.9% for automotive loans.

But it is not just the approval rate that is coming down but also the application rate. Bank Negara data shows that the application for the purchase of residential property dropped 11.8% y-o-y in July.

The statistics show nascent signs of improvement in household debt. Should the efforts to rein in household debt continue?

This article first appeared in The Edge Malaysia on Sept 12, 2016. Subscribe here for your personal copy.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.