ADVERTISEMENT

All Property News

Stay updated with the latest real estate and finance news, including property market trends, housing insights, and valuable information.

Loke says govt ramping up efforts to expedite LRT3 opening

18 hours ago

Wisma ELM structural framework intact—AmanahRaya REIT

19 hours ago

UEM Sunrise completes RM500 mil Islamic medium-term note issuance with 12-year tenure

21 hours ago

PR1MA appoints Brian Iskandar Zulkarim as group CEO

Yesterday

UDA hands over UDA Heights in Johor

Feb 13, 2026

Paramount’s FY2025 profit attributable up 16% to RM118.82 mil

Feb 13, 2026

S P Setia CNY Campaign 2026—Bag limited-time homeownership prosperity perks up to RM3,888 rebates!

Feb 11, 2026

How to reap Johor Bahru’s ripe opportunities without getting burned if the bubble bursts

Jan 9, 2026

The truth about GRR: Why you should run away from buying that “promised income” property

Dec 19, 2025

Shorts

View All

What made headlines this week from rental policy updates to major property developments.

Ancubic builds premium, design-led developments by identifying the high-demand 20%, delivering elevated commercial and lifestyle spaces where quality is missing but needed.

What agreements were inked and which projects progressed this week?

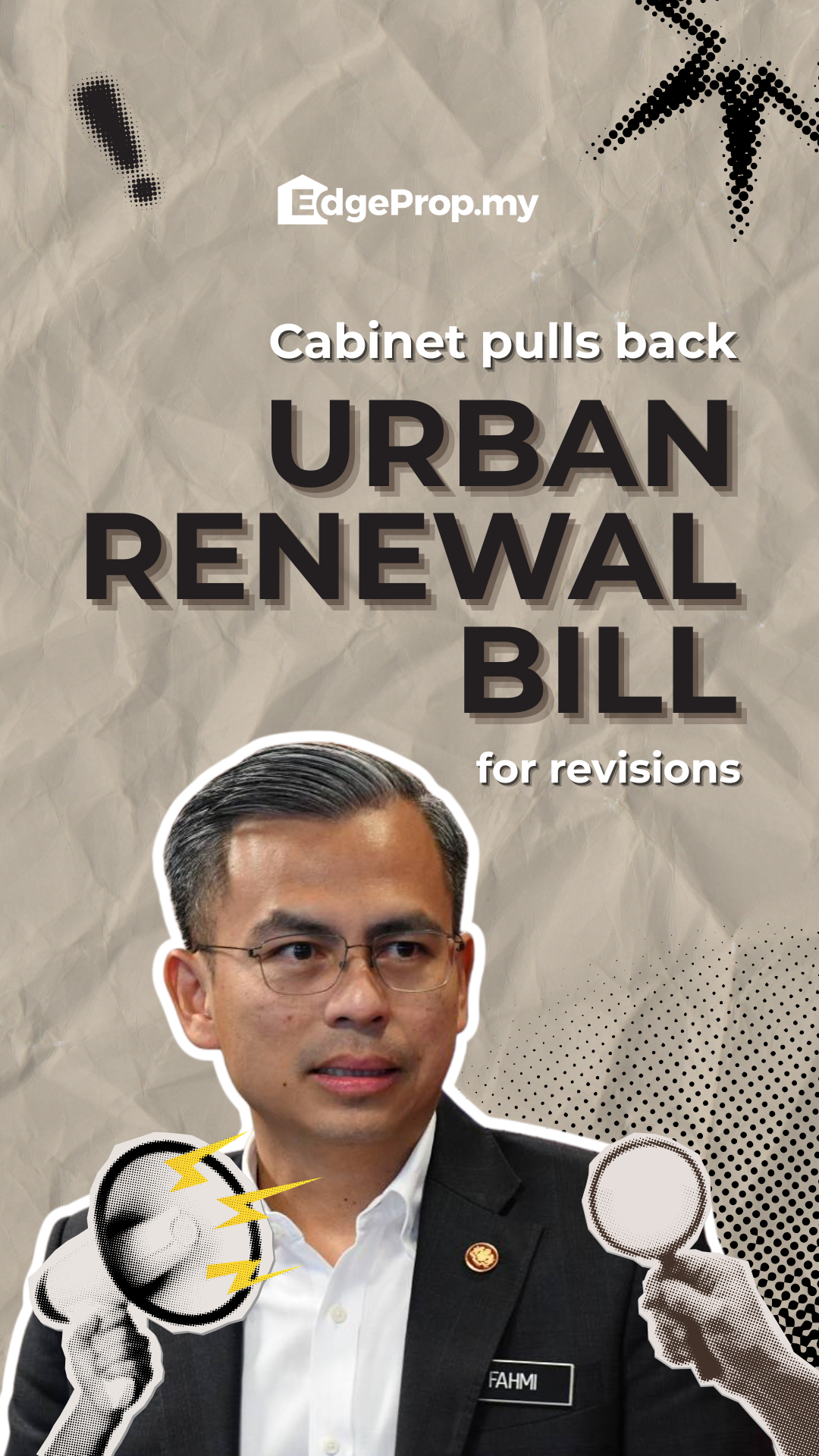

From Cabinet decisions to big-ticket projects, here’s a fast rundown of the headlines you need to know this week.

Curious what deals were sealed, and which developments took shape this week? Keep watching to find out.

Legally Speaking

Govt seeks to forfeit funds in Ilham Tower, individual accounts linked to Daim case

Guide to Homebuying

Find the best location for your home

Legally Speaking

KL High Court rules developer’s ‘contra arrangements’ with landowner invalid in K Residence condo case; Duta Yap’s son held personally liable

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.