Paramount Corp Bhd (March 4, RM1.53)

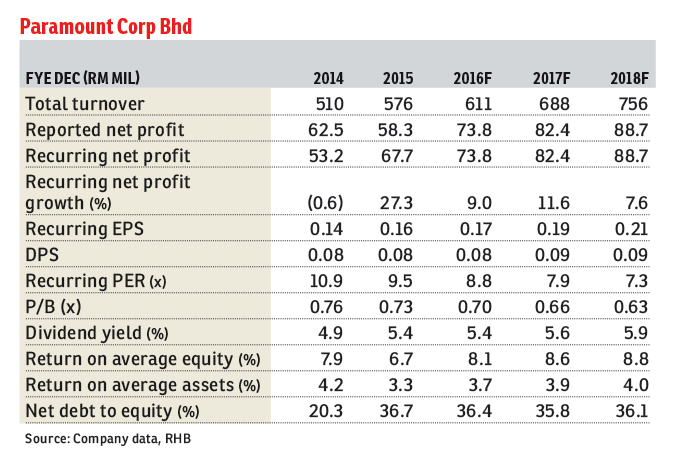

Maintain buy with an unchanged target price (TP) of RM2.32: At last Thursday’s briefing, management remained committed to achieving more than 10% growth in new sales and earnings. Paramount Corp Bhd’s sales prospects seem more promising amid the weak property market, given the more exciting product launches in the pipeline. We maintain “buy” and a TP of RM2.32 (52% upside). While the potential asset monetisation exercise may take some time, its share price would be supported by a higher than 5% dividend yield.

Financial year 2015 (FY15) core earnings growth of 27% marks the new chief executive officer Jeffrey Chew’s first report card as he joined the company in July 2014. For FY16, management expects to achieve RM480 million sales (from RM432 million in FY15) and double-digit earnings growth, on the back of RM770 million worth of new launches.

Despite the challenging property market environment, Paramount’s pipeline launches are carefully chosen to ensure more sustainable sales. New projects include Phase 1 of the Section 13 Petaling Jaya project (gross development value (GDV): RM300 million) and Phase 1 of the Batu Kawan university metropolis development (GDV: RM106 million), a concept similar to the highly successful Utropolis Glenmarie. Both projects were delayed from last year due to the Strata Titles Act amendment, but should be ready for the second-half launch. While Section 13 mainly targets the young population in the established neighbourhood, the Batu Kawan development is in a new growth area. Another developer, Aspen Group, which is the joint-venture partner of the new Ikea store there, fully sold all its retail shops (451 units) last year. As Paramount’s development is located just opposite Aspen Group’s land, it should similarly be saleable.

Acknowledging the market challenges, management has also set a target for at least 30% of annual launches to be landed residential properties. Paramount rolled out the first phase of the Salak Perdana project (GDV: RM58 million) late last year. Priced at RM450,000 to RM500,000 per unit, the take-up rate of the terraced units improved to about 40% from 18% in December 2015.

A new K12 school in Klang has been set up. After conducting various research and studies, management believes that demand for international schools in Klang should be strong, given the lack of reputable private education institutions there. A licence for a new primary and secondary school has already been obtained from the education ministry. Earthworks for the new campus in Klang will start in June this year, and construction will take about two years. We expect the school to commence operations in 2019, and this should add 1,500 students to the current total of 3,141 in the K12 segment.

While the potential asset monetisation exercise, i.e. the key share price catalyst, may take time, decent earnings growth underpinned by RM367 million in unbilled sales and the resilient education segment should help to sustain the higher than 5% dividend yield. Key risks are delays in launches and worse-than-expected market conditions. — RHB Research, March 4

This article first appeared in The Edge Financial Daily, on March 7, 2016. Subscribe to The Edge Financial Daily here.

TOP PICKS BY EDGEPROP

Mayfair Residences @ Pavilion Embassy

Keramat, Kuala Lumpur

The Canal Garden South, Horizon Hills

Iskandar Puteri, Johor

The Astaka @ 1 Bukit Senyum

Johor Bahru, Johor

Teega Residences, Puteri Harbour

Kota Iskandar, Johor

{kind=link}