Sunway’s medical unit seen to be a leader in Asean

Sunway Bhd (Dec 15, RM1.70)

Maintain buy with an unchanged target price of RM2.25: A recent visit to Sunway Medical Centre (SunMed) has further enlightened us on the plans and capabilities of its underappreciated healthcare business, which runs a medical centre, home nursing service and retail pharmacy.

It has embarked on a multi-year expansion, with a newly opened Tower C (new wing) called SunMed, which currently houses 620 beds (largest in Malaysia), from 373 just a year ago. Next in the pipeline would be a new medical centre in Velocity by the first half of 2019 (1H19). Sunway has set its target to achieve a total capacity of 2,000 beds in five years’ time.

Although the new wing has been up and running for less than a year, we understand that it is already generating a profit at operational level — bucking the trend of a long gestation period in the private healthcare business.

A seamless execution has been made possible thanks to its management’s experience and strong branding.

SunMed now operates 25 Centres of Excellence across an entire spectrum of healthcare needs. Housing 180 consultation suites, 200 specialist consultants, 12 operating theatres with new advance equipments and continuing medical education via various collaborations, SunMed aspires to become the leading medical centre in the Asean region.

The recent RM30 million allocation in Budget 2018 to the Malaysia Healthcare Travel Council and Visit Malaysia Year 2020 to promote Malaysia as a top destination for medical tourism is expected to benefit SunMed. Besides, we believe that SunMed is a front runner for a Flagship Hospital Programme, given its expertise and unmatched location.

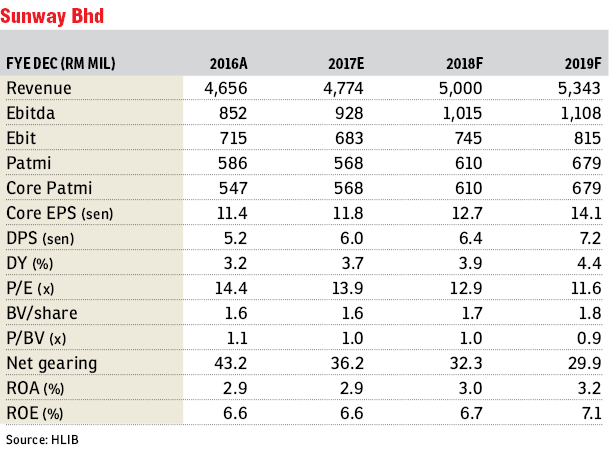

A cheaper entry into the healthcare business via Sunway Bhd is possible, which is trading at a forward price-earnings ratio (PER) of 13 times, compared with IHH Healthcare Bhd of 46 times and KPJ Healthcare Bhd of 23 times.

Using a price multiple of 25 times, its healthcare segment is estimated to fetch a valuation of more than RM1.3 billion considering that the expansion at SunMed is up and running. Besides, a spin-off of the healthcare business is also on the cards, along the shareholder value creation journey.

Risks include execution risk and a prolonged downturn in property capping growth in other segments.

Sunway is our top pick within the sector as we believe it should be rerated and that it should trade closer to its peers, such as IJM Corp Bhd and Gamuda Bhd — given its diversified income stream and declassification from the property sector.

At a forward PER of 13 times compared with peers, we opine that this is a deep-value stock with mature investment properties and an under-appreciated trading and healthcare businesses. — HLIB Research, Dec 15

This article first appeared in The Edge Financial Daily, on Dec 18, 2017.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.