Construction sector to be rerated on HSR

Construction sector

Maintain overweight: The tender for the project delivery partner (PDP) to undertake the Malaysian portion of the Kuala Lumpur-Singapore High-Speed Rail (HSR) infrastructure construction works was called on Nov 22, 2017, and will close on Jan 30, 2018. The tender for the AssetsCo public-private partnership project was jointly launched by MyHSR Corp Sdn Bhd and Singapore’s SG HSR Pte Ltd on Dec 20, 2017, and will be closed on June 29, 2018. We expect the potential news flow on contract awards for the RM60 billion HSR project will be a major upward rerating catalyst for the Malaysian construction sector.

The PDP tender is expected to see stiff competition since it is open to both foreign and local consortiums with HSR experience and have undertaken major railway projects in Malaysia. The Gamuda Bhd and Malaysian Resources Corp Bhd (MRCB) [Gamuda-MRCB] joint venture (JV) and IJM Corp Bhd-Sunway Construction Bhd (SunCon)-Jalinan Rejang Sdn Bhd-Maltimur Resources Sdn Bhd JV are among the strong contenders for the PDP role. We believe a local consortium has a better chance than a foreign one to bid for the PDP role. We believe the Gamuda-MRCB JV is in a strong position to win the PDP tender given Gamuda’s extensive experience in PDP projects (completed mass rapid transit [MRT] Line 1 and undertaking MRT Line 2) and undertaking railway projects (completed Ipoh-Padang Besar double- tracking). We believe MRCB has the political links, experience in developing railway transportation hubs and the backing of major shareholder Employees Provident Fund.

According to the tender documents, the AssetsCo is responsible for designing, financing, building and maintaining the rolling stock and rail assets, including track work, power, signalling and telecommunications. Malaysian companies have limited experience in HSR and the financing requirement is likely too high with the estimated cost at between RM15 billion and RM20 billion. They will have to team up with foreign companies to bid for the AssetsCo role. We gather that MMC Corp Bhd with Japanese partner(s), George Kent (M) Bhd partnering with Siemens and YTL Corp Bhd with Chinese partner(s) are interested to bid for the AssetsCo role. There is no requirement for the AssetsCo to have a Malaysian or Singaporean partner.

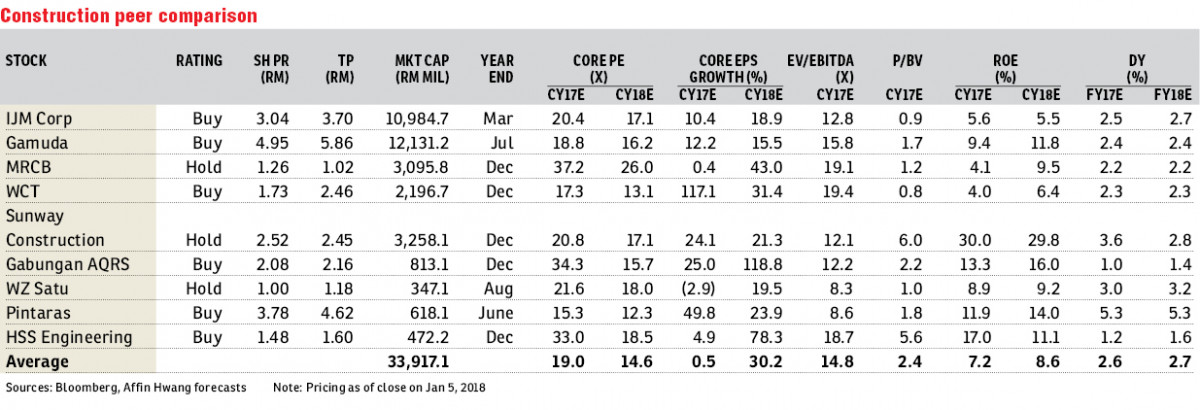

It was reported that a Chinese consortium, led by China Railway Corp, will bid for the AssetsCo role for the HSR. It is uncertain if there will be any Malaysian beneficiaries for the AssetsCo bid. We gather that the infrastructure works for the Malaysian portion of the HSR could be worth between RM35 and RM40 billion. The PDP fee for the MRT1, MRT2 and light rail transit Line 3 (LRT3) is based on 6% of the project cost. Based on the same fee structure, the Malaysian PDP for the HSR project will potentially earn net profit of RM1.60 billion to RM1.82 billion (applying a corporate tax rate of 24%) over the 2019 to 2026 construction period or RM200 million to RM228 million per annum (based on a straight-line recognition basis). Based on 50:50 JV shares in Gamuda and MRCB, we estimate the potential earnings lift if the JV secures the project is 21% to 24% and 63% to 72% respectively in estimated financial year 2019 (FY19E). Assuming IJM Corp and SunCon’s share of the PDP fee is 33% each, the potential earnings lift if the IJM Corp-SunCon-Jalinan Rejang-Maltimur Resources JV wins the PDP contract is 25% to 29% in FY20E for IJM Corp and 100% to 114% in FY19E for SunCon. — Affin Hwang Capital, Jan 8

This article first appeared in The Edge Financial Daily, on Jan 9, 2018.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.