ADVERTISEMENT

All Property News

Stay updated with the latest real estate and finance news, including property market trends, housing insights, and valuable information.

PRG major shareholder Ng pushes back against ‘one-sided’ claims, highlights over RM89m financial support for group

7 hours ago

Mah Sing gets shareholders’ nod for RM2.26 bil MS Industrial Park @ Kulai project

7 hours ago

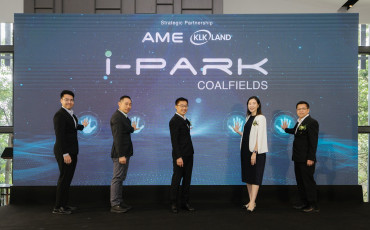

AME Elite, KLK Land unveil RM1.3 bil i-Park@Coalfields industrial park in Selangor

8 hours ago

TA Global partners Gaggenau, Gessi and Laufen for CloutHaus Residences

9 hours ago

The Troika, Kuala Lumpur SoHo unit rented for RM8,000 | DONE DEAL

10 hours ago

PRG rejects shareholders' requisition to convene EGM to revamp board

13 hours ago

![[Branded] Sabah’s next frontier: a prime window for resort investments in East Malaysia’s coastal belt](https://media.edgeprop.my/s3fs-public/styles/simplecrop/public/field/image/sempornawyndhambird'seye.jpg)

![[Branded] FAR Capital makes ‘impossible’ rental returns, with data dispelling critics’ disbelief](https://media.edgeprop.my/s3fs-public/styles/simplecrop/public/field/image/underconstruction_0.jpg)

.jpg?sCKFImEqUesBHXT_lIvjplKjBWFpqpUp)

Shorts

View All

Every award tells a story, and every member inspires the next. ???? Hear from our past award-winning members as they share how REALTORS' Roundtable Malaysia has opened doors, built lasting connections, and elevated their careers. Here's to excellence, growth, and celebrating the next generation of industry leaders this September, at #RRT2026. ???? #RealtorsRoundtable #RRTMalaysia #RealEstateExcellence #RealEstateCommunity

In an alternate universe this would've been their career!

A little throwback to EdgeProp Malaysia's Realtor's Roundtable Awards 2025✨️

Bangsar is still one of KL’s most desirable suburbs— but what’s driving demand today?

This central business district is redefining Kuala Lumpur's skyline and strengthening Malaysia's position as a leading business hub. With Grade A offices and premium retail spaces, this is where experts say the future of commercial real estate is taking shape.

.jpg)

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.