Will M-REITs continue to beat the odds in 2017?

AFTER the lacklustre retail sales figures seen this year, retailers and analysts expect consumer spending to gradually recover next year. The immediate concern over the glut of retail space, however, remains a wild card in 2017.

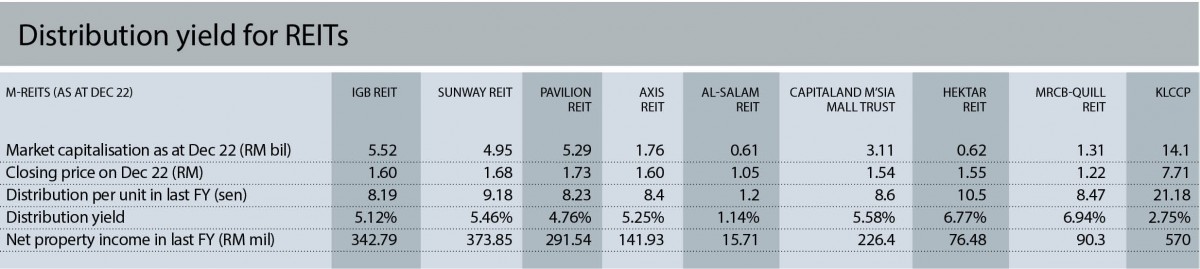

There is no doubt that Malaysia’s real estate investment trusts (M-REITs) were some of the top performers in the local equity market. Uncertainty in the global financial markets, coupled with the lower bank deposit interest rate, made M-REITs favourites among investors to stash their cash.

The sector’s performance remained resilient, despite the downturn in the real estate market. This could be mainly due to the defensive nature of the business.

“The outlook for the retail sector in Malaysia is expected to show marginal improvement in 2017 as we see that [poor] consumer sentiment should have bottomed out in 2015,” MIDF Research analyst Jessica Low Jze Tieng says in an email reply to The Edge.

“In this context, we expect a slightly better outlook for retail sales in Malaysia, which should underpin rental reversion for the retail segment to remain in positive territory,” adds Low, who continues to be bearish on the office space segment.

“We opine that the office segment will continue to be a tenants’ market due to the oversupply of space, which renders limited upside to rental reversion.” She is maintaining her “neutral” rating on the sector.

For the year ahead, Low says her top pick for the sector is Sunway REIT as she is positive about the performance of the Sunway Pyramid shopping mall going forward.

“Sunway Pyramid’s performance has remained fairly resilient due to the high footfall and occupancy rates. Hence, earnings from the retail division, which is [Sunway REIT’s] biggest earnings contributor, should continue to be supported by Sunway Pyramid,” Low states.

As for the REIT’s office division, the worst is over, she remarks. She expects that division to see an earnings recovery in the financial year ending June 30, 2017 (FY2017), as management is proactively seeking tenants to fill up its vacant space.

Sunway REIT CEO Datuk Jeffrey Ng Tiong Lip does not expect consumer sentiment to further deteriorate in view of the country’s low unemployment rate. But consumers are likely to remain prudent with their spending due to the higher cost of living, he says in an email reply.

Ng acknowledges that the shopping mall segment is currently facing an oversupply situation, with an estimated 17 million sq ft of retail space expected to enter the Klang Valley between now and 2019.

In view of the fierce competition from existing and upcoming players, Ng expects the rental reversion growth rates to moderate.

To address the slower and more challenging economic situation, Sunway REIT will continue to drive its business forward while exercising a higher level of prudence in its operation and ensuring continuous prudent cost management initiatives where necessary, says Ng.

“We believe in long-term business relationships where we are committed to weathering the tough times with our tenants and prospering together during the good times.

“In today’s environment, we support our tenants through continuous marketing activities to increase footfall in the mall,” he adds.

Ng says Sunway REIT also assists its tenants in promoting their products and services at the promotional areas and on social media.

“We believe that market dynamics have their ups and downs. By supporting our tenants in sustaining their businesses, it will be a win-win situation when the market recovers.”

According to Ng, the prevailing challenging landscape is likely to continue in the year ahead, hence Sunway REIT will continue to reassess and realign its strategies with increased agility to combat the headwinds.

“We have to exercise more prudence and vigilance, and ensure that all planned strategies are well executed,” says Ng, who is forecasting a dip in Sunway REIT’s distribution per unit (DPU) in FY2017 from FY2016.

This is mainly attributable to lower contribution from its hotel segment due to the closure of Sunway Pyramid Hotel for refurbishment as well as the cessation of payment of manager’s fees in units with effect from FY2017.

Having said that, Ng is optimistic that Sunway Pyramid Hotel will be in a good position to capture a different market segment after the refurbishment, which will contribute positively to the DPU and value enhancement to unitholders.

Komtar JBCC to drive Al-Salam’s growth

Al-Salam REIT, a diversified Islamic REIT with assets located strategically in Johor Bahru City Centre (JBCC), says retail sales will remain soft in the first half of next year due to the still-weak consumer confidence.

“Nevertheless, we expect Johor Baru’s retail property market to remain resilient going forward,” the trust manager for Komtar JBCC says in an email.

“Despite the high concentration of retail space, we believe the state capital will not suffer from oversaturation and cannibalisation of retail space as it currently lacks new, modern, well-managed and high-quality malls,” it adds.

Overall, Al-Salam says the sector is expected to remain resilient, boosted by the cut in the overnight policy rate (OPR) by Bank Negara Malaysia, which has led to a widening yield spread between Malaysian Government Securities (MGS) and REITs.

“Additionally, the defensive nature of the sector is another pull factor contributing to the increased interest in the sector, given the current market volatility and economic slowdown. Another OPR cut will surely provide another boost towards elevating the valuation of the sector,” says the REIT manager.

Moving forward, Al-Salam believes its main growth driver will be Komtar JBCC. The mall is expected to contribute more than 50% to the REIT’s total revenue in the next few years given that the mall is still in its infancy, having only commenced operations in 2014.

“As such, we believe there is a substantial upside potential for the mall in terms of a higher occupancy rate and strong rental rate reversion in the future. The percentage rent income (revenue sharing) from Komtar JBCC will also support better earnings in FY2017.”

On a different note, Al-Salam says it may be looking to acquire assets from third parties to achieve inorganic growth.

M-REITs’ performance in 2016

As at Nov 28, M-REITs had outperformed the FBM KLCI, with the former registering an average return of 9% versus a loss of 3.8% seen in the local benchmark index, MIDF Research’s Low says.

This could be due to market volatility and the surprise OPR cut by Bank Negara in July, which boosted demand for other yield assets such as REITs, she adds.

Among the M-REITs, the best performer is Al-‘Aqar Healthcare REIT (+17%), followed by Al-Salam (+15%), says Low.

The laggards, she continues, are Tower REIT — which saw a negative return of 3% — and Atrium REIT, which saw a flat return.

This article first appeared in The Edge Malaysia on Dec 26, 2016. Subscribe here for your personal copy.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.