S P Setia earnings prospects expected to remain intact

S P Setia Bhd (Nov 20, RM3.39)

Maintain buy call with an unchanged target price (TP) of RM4: Bandar Setia Alam Sdn Bhd, a wholly-owned subsidiary of S P Setia Bhd, was served by the Inland Revenue Board with notices of additional assessment for an additional income tax of RM52 million and a penalty of RM23 million, totalling RM75 million.

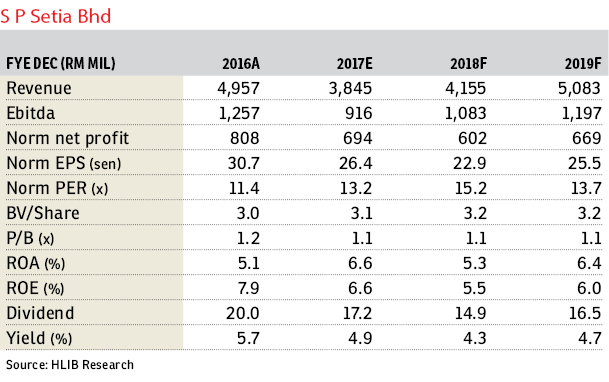

The retrospective tax claim of RM75 million is expected to negatively impact our financial year 2018 (FY18) bottom line by 12%.

However, we do not take into account the potential negative impact as it is considered non-recurring in nature as well as on the notion that S P Setia is ready to challenge both the notices and penalty.

The above-mentioned additional income tax and penalty were imposed in the view that gains from the disposal of land and property held under investment property were chargeable under the Income Tax Act 1967 instead of the Real Property Gains Tax Act 1976 (RPGTA).

However, S P Setia is of the view that there are reasonable grounds to challenge the basis and validity as the sales of the investment property are capital transactions, which fall under the purview of the RPGTA.

Apart from the tax issue, we also clarified the outlook for S P Setia following the completion of Phase 1 of Battersea on Oct 17. We understand that subsequent phases are expected to contribute only from FY20, which leads us to revise downward our earnings forecasts for FY18 and FY19.

Moving forward, the focus is to ramp up local sales with launches in the group flagship townships, where underlying demand is still favourable, such as Setia Alam, Setia EcoHill, Setia Eco Templer and KL Eco City.

The overall earnings prospects remain intact, underpinned by total unbilled sales of RM7.1 billion (with a cover ratio of 1.7 times), which will sustain its earnings visibility for the coming years.

We remain positive on the proposed synergistic acquisition of I&P Group, which is expected to be completed by Dec 17.

However, more guidance is warranted before we impute the full impact of the enlarged entity with 9,400 acres (3,804ha) of land bank and a gross development value of more than RM100 billion post merger exercise.

We adjust our FY18 and FY19 bottom-line forecasts downwards, taking the completion of Battersea Phase 1 into consideration and impute the contribution of Sapphire by the Gardens into our revalued net asset value (RNAV).

We believe investor sentiment towards S P Setia would improve as the proposed acquisition of I&P Group is RNAV-accretive, and it will potentially drive them to become the largest pure property player in the market.

Additionally, its consistently high dividend yield is another positive point.

We maintain “buy” with an unchanged TP of RM4, based on an unchanged 30% discount to RNAV of RM5.71, given the accretive major corporate exercise which has long-run synergy. — Hong Leong Investment Bank Research, Nov 20

This article first appeared in The Edge Financial Daily, on Nov 21, 2017.

For more stories, download EdgeProp.my pullout here for free.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.