Homeownership could be made more affordable if we opened our minds

- "If we can unstaple the two characteristics, we can make homeownership affordable to people who are currently renting a landed home — you pay the same rent AND own the home. In fact, it will also reduce overall rents, making the housing market a more efficient asset for all. How? By introducing a perpetual mortgage.”

PETALING JAYA (Oct 31): There are understandably growing worries over the high level of indebtedness the world over, and especially so given the current environment of rapidly rising interest rates. The recent market meltdown in the UK underscores the rising risks of a broader global financial crisis. The excesses of the past decade, the borrowing binge fuelled by ultra-low interest rates and liquidity, are coming back to bite us, no doubt.

As we wrote a couple of weeks back, governments — especially in developed countries — have been the biggest culprits, using cheap debt to finance massive fiscal spending. Public debt has risen at nearly double the pace of private debt, by 142% in the 13 years from the global financial crisis to 2020. This addiction to debt is particularly difficult for democratically elected governments to reverse. The International Monetary Fund (IMF) recently warned that 60% of low-income countries and about 30% of emerging markets are either in, or at the edge of, a debt crisis. Some of these countries are now spending more on debt servicing (interest payments) than on critical needs such as education and healthcare, and surging yields make it even harder to refinance maturing debts. (That no single developed country is pointed out as facing a similar debt crisis — even though some have among the world’s highest debt-to-GDP ratios — is just a further reflection of the biases and hypocrisies of global institutions, which are increasingly losing credibility.)

This week, we turn to household debt. Globally, household debt too has grown, albeit at a much slower pace compared to public and corporate debt. As we explained previously, there are some safeguards against excessive borrowings as banks are more vigilant in assessing the credibility of households, who themselves are more cautious due to the direct consequences if they cannot service their debts, including bankruptcy.

Even so, many highly indebted households will struggle with rising monthly repayments, given the steep increase in borrowing costs, on top of surging living costs. Switzerland (132%), Canada (104%) and Australia (123%) have the highest household debt-to-GDP ratios in the world, while Malaysia too ranks near the top, at 89%, on a par with the UK and above the US (67%). Some households will almost certainly run into serious financial troubles. But how risky is this high household indebtedness to the global financial system and economy?

We think there are reasons to be optimistic — in that the headline figures may be exaggerating the risks. Why? Because the mortgage typically accounts for the biggest chunk of household debts. For instance, the mortgage makes up more than 66% of total household debts in the US and a slightly lower 62% in Malaysia. The lower ratio in Malaysia is mainly due to comparatively higher car prices and thus, hire purchase loans, which account for 15% of household debts as compared to 9% in the US. And the home is an asset. (We will argue in a future article that it is the ownership of cars we must dissuade or that car prices must fall for the livelihoods of most Malaysians to improve.)

High household debt not as risky as it appears — the home is an asset, not an expense

Globally, house prices have outpaced income — and GDP — growth in the last two decades. Yes, there were property slumps, some worse than others, but prices inevitably recovered higher, save for some exceptional circumstances. The latter mainly occurs in countries/regions where population ageing is so acute that negative population growth becomes secular and no action is taken to reverse it.

It is this longer-term uptrend in property values that has driven household debt higher — because homeowners have to take out larger and larger mortgages in absolute dollar amounts. Hence, household debt-to-GDP and relative to incomes go up. But it also means that household wealth is growing over time. And this, we say without reservation, is good. Yes, there are negative consequences, which we will elaborate on a bit later in this article, along with our solution.

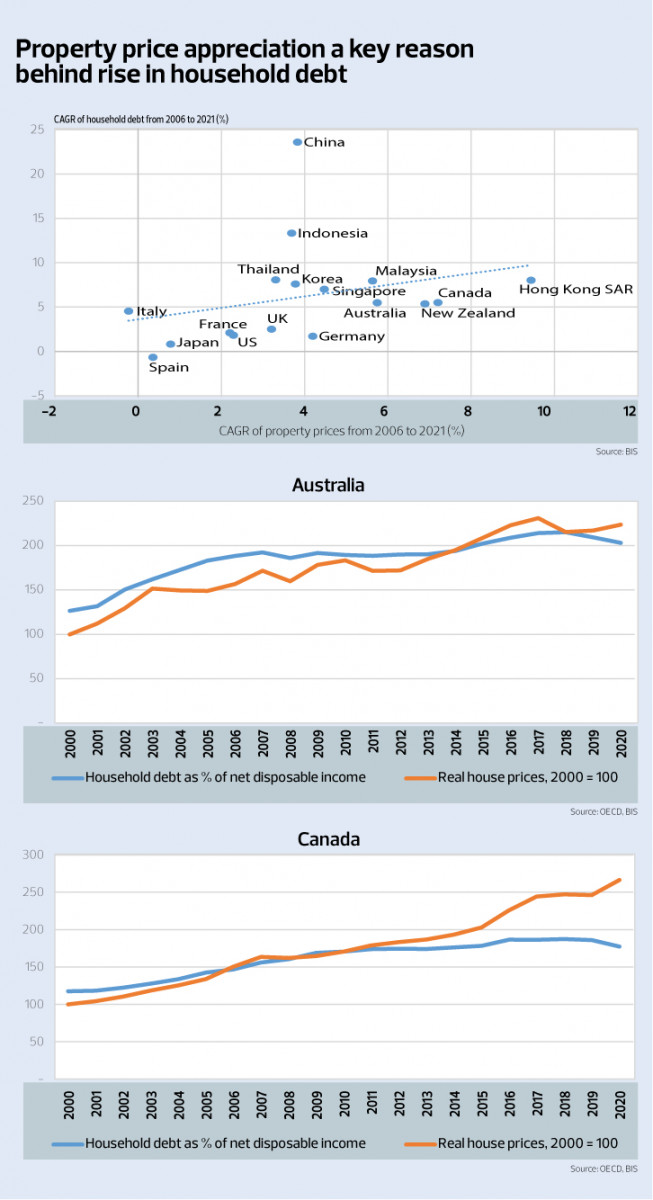

Take the case of Australia and Canada. As noted above, both countries have seen some of the steepest rises in household debts — as a percentage of GDP and disposable incomes — on the back of rising property prices, that is in part due to a huge influx of overseas money into the sector (see Chart 1). This would be worrying IF we only looked at household debts in isolation and debt servicing as an expense item. But we must also take into account the other side of the equation, which is the matching appreciation in wealth, principally the value of houses and, to a lesser extent, other financial assets. The statistics show that household wealth gains in both countries have far outpaced the increases in debts. In other words, household net wealth (assets minus debts) has risen significantly over time — and the people are richer!

In fact, this is no different from how we assess the indebtedness of companies — it is often a balance sheet comparison, borrowings against assets (cash, property, plant and machinery and so on). For example, the current ratio and debt-to-equity or debt-to-net-asset ratio.

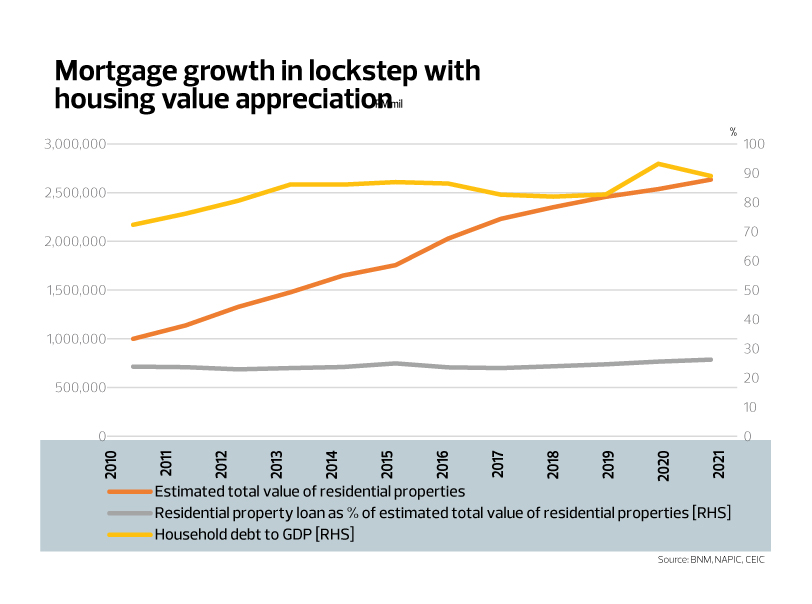

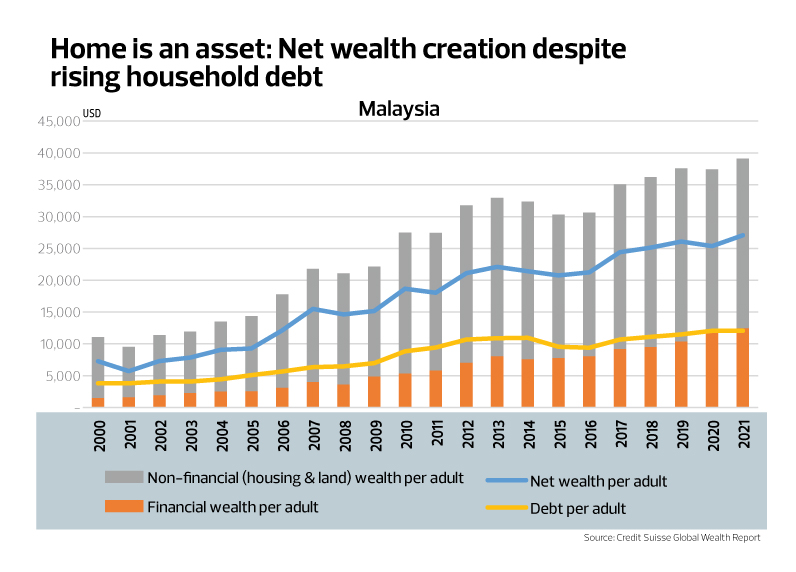

This is similarly the case in Malaysia. Although household debt-to-GDP has risen sharply — from 72% in 2010 to 89% currently — this is in large part due to mortgages. Residential property loans (the single largest item in household debts) as a percentage of house value has stayed flattish (see Chart 2) — that is, the absolute debt growth is tracking higher property values. Chart 3 clearly shows household wealth per adult — especially from non-financial assets (mainly land and housing) — expanding at a much faster clip than debts. In other words, net wealth per adult is rising.

House prices and home equity have risen substantially over the past 20 years

Coming back to the question of risks. Remember, homebuyers must contribute equity, typically 20% of the value of the property. Hence, the first 20% price drop will only wipe out equity in the short term, without serious repercussions, as long as people are able to continue servicing their mortgages. And since home equity has been building over time, there is relatively low risk of negative value for those who bought their homes years ago — unless the market spirals into a catastrophic collapse. Most property slumps in the past have been due to excessive speculation and overbuilding in specific locations, not a broad global property crash.

There are reasons why property prices worldwide have trended up over the course of history. They include factors that increase demand — land scarcity (premium to centre due to time and transport costs), population growth and declining household size, urbanisation and migration, inflation (in construction costs, for labour, land and building materials), policy incentives (such as tax deductibility of interest payments) and, of course, speculation and financial innovation (that makes buying a home easier and more affordable) — and reduce supply such as regulatory approvals, land conversion and zoning rules.

The bigger threat is rising housing unaffordability

The threat is the growing unaffordability of homes as a consequence of rapid price appreciation. Historically, ownership — and steady rise in prices — of housing have been the key driver of mass wealth creation-accumulation. This is due to their comparatively wide ownership compared with other asset classes, such as stocks. Case in point, home ownership in Romania and Laos is a high 96%. A huge majority of people in China (90%), Singapore (89%), Malaysia (77%), the US (66%) and the UK (65%) are homeowners. Often, the extent of homeownership is a reflection of public policies and inequality. For example, it is low in Germany (50%) due to the country’s high real estate transfer tax and social housing programmes, where not-for-profit and private housing developers receive subsidies to build and rent to low-income households. And it is very high in Singapore because of the Housing & Development Board’s (HDB) very successful public housing scheme.

However, what has been a boon for hundreds of millions of homeowners in the past is now becoming a bane for the younger generation. As we wrote (in Issue 1442, Oct 10), the golden decades of broad-based wealth creation (accumulation) are over. Decades of housing price gains — made worse by speculation that was enabled by ultra-low interest rates and excessive liquidity — that outpaced income growth has resulted in increasing unaffordability of homes. Left unaddressed, homeownership will become increasingly concentrated, which will worsen inequality. Soon, only the rich will be able to afford to buy a home, while the majority of households will no longer be able to participate in the wealth creation process.

In countries with some of the lowest homeownership numbers, including Hong Kong, Switzerland and South Korea, soaring prices — as a percentage of incomes — are pricing an increasing percentage of their populations out of the market, and especially the young. This is why governments often try to rein in speculation, especially when prices are being driven by non-residents. Shelter — in addition to food — is a basic necessity in life, the lack of which oftentimes leads to discontent, unrest and, ultimately, sociopolitical instability. How do we improve affordability without destroying property values — and the wealth of the majority of the population?

How to improve home affordability without destroying property values?

Housing has two primary functions. One, as we noted, is for use as shelter and the other is as an investment, an asset class for wealth accumulation. There is a separate price for both functions or characteristics, which the market, very helpfully, already supplies us with the answer. It is the difference in yields between renting a landed property and a high-rise condo apartment — where capital gains for the former is expected to be much higher than for the latter over time.

For example, the current rental yield for landed housing in Malaysia is about 2%-3% on the property value while that for high-rise property is around 4%-5%. The rental yield for landed housing is lower because it is, primarily, the price for utility (shelter). The difference in yields (high-rise minus landed) is made up by the capital appreciation (the investment returns that accrue to owners) over time.

Therefore, if we can unstaple the two characteristics, we can make homeownership affordable to people who are currently renting a landed home — you pay the same rent AND own the home. In fact, it will also reduce overall rents, making the housing market a more efficient asset for all. How? By introducing a perpetual mortgage.

On a side note, in order for strata residential properties in Malaysia to also enjoy capital appreciation, current regulations must be changed to allow for easier en bloc sales, to facilitate redevelopment. In many other countries, approvals from only 80% of owners will force an en bloc sale, instead of 100%. Such a rule change would not only benefit owners, but also renters — as with the case for landed properties, where there is meaningful capital appreciation, rental yields are lower. For the owners, it is the total expected returns on investment that matters, the sum of capital gains and rental incomes.

(Read also: How FundMyHome did in comparison … let the facts speak for themselves)

An out-of-the-box solution

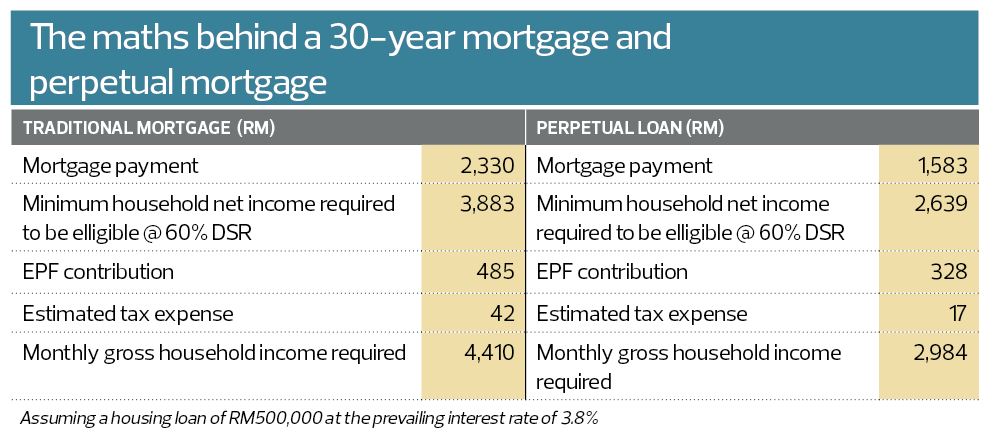

For a traditional mortgage, the monthly instalment consists of the interest payment (on balance outstanding) and principal repayment. By stretching out the mortgage tenure, say, from 20 years to 35 years, we can reduce the monthly instalment. Why not go further? In a perpetual mortgage, there would be no principal repayment at all — until the home is sold or the owner decides to pay off the loan. In other words, homeowners need only pay the monthly interest payment on the loan amount, which would roughly be what one would expect to pay for rent.

The table above is a back-of-the-envelope calculation comparing a traditional 30-year housing loan of RM500,000 with a perpetual loan (of the same amount) at the prevailing mortgage rate of 3.8%. Under the traditional mortgage, the monthly instalment works out to RM2,330 and based on current eligibility criteria, the household income must be above RM4,410 to qualify for the loan. For a perpetual mortgage, the monthly instalment is less, at RM1,583 (in the absence of principal repayment) and the qualifying household income is correspondingly lower at just RM2,984. In other words, all those households with incomes below RM4,410 but higher than RM2,984 are now eligible for a loan.

This means a huge segment of the population can now own a home much sooner (since the required income is 32% lower) and start building their home equity (wealth accumulation). There will be greater savings from disposable incomes over their working life, which would pay towards maintaining their lifestyles after retirement, without having to sell their homes in their old age. Home equity — and net wealth — will grow as the house price appreciates and the value of the debt falls over time.

Why would banks offer a perpetual mortgage with no principal repayment? Because their core business is lending and a perpetual mortgage just means there is no need to replenish a loan book that is continuously being paid down. New customer acquisition is very expensive — just look at the cost of the entire sales team in banks.

Perpetual mortgages can be sold in the secondary market, providing it with the liquidity similar to traditional mortgages, which can currently be sold to other banks and central agencies such as Cagamas Bhd, the National Mortgage Corporation of Malaysia. Most banks, though, prefer to keep their mortgages, as evidenced by Cagamas’ difficulty in growing its loans. Mortgages carry low interest rates because of their perceived low risks (risk of default or risk of loss to banks). Indeed, they generally require minimal provisions, which effectively lower the cost of funding for banks.

The risks on the perpetual mortgage can be defrayed with insurance, guaranteeing the loan amount (80% of property value based on 20% equity contribution from homeowners). This would shift its risk profile closer to those of government securities. We are fairly certain the insurance premium will be marginal (relative to the house value). As we said, property prices will have to fall by more than 20% before there is any loss for insurers. And with a vast, diversified portfolio, the average risks for the insurance company will be even lower. And in fact, Cagamas currently already has a scheme — in collaboration with the government and Bank Negara Malaysia — called the Skim Rumah Pertamaku (SRP), in which it provides up to 110% guarantee (insurance) to banks for houses below RM300,000 and aspiring first-time homeowners with household incomes of less than RM10,000.

While the risk of losses may be low (to banks), having the insurance intermediary or independent third-party valuers is very important. It is an independent validation of the house value, for example, to prevent cases of over-valuation and to maintain confidence in the house pricing process.

Conclusion

We believe the risks of the current high household debt-to-GDP is not as worrying as the headline numbers may suggest. This is because a huge chunk of the borrowings are mortgages for residential housing. And a home is an asset as compared to, say, a car, which is an expense. Based on robust price gains — that have outpaced income growth historically — households have built substantial equity in their homes. Hence, their net wealth (home value less mortgage) has actually risen over time. Home ownership has been the single biggest driver of mass wealth creation-accumulation in the past decades.

The real problem is, we think, the growing unaffordability of homes — especially for the younger generation — as the consequence of rapid house price appreciation. The question, therefore, is how do we improve home affordability without destroying property values and, with it, the wealth of the majority of the population?

Our solution lies in disaggregating or unstapling the two functions of housing — for use as shelter and for investment. This can be achieved by structuring mortgages as perpetual loans. By lowering monthly instalments, homeownership will be made affordable to a larger segment of the population. The risks can be defrayed with insurance, and tradability of loans in the secondary market will provide originating banks with the necessary liquidity.

Yes, it means not paying down the principal amount of debt, and likely leaving it to one’s beneficiaries. But there is nothing to stop homeowners from paying down the debt, if and when they so choose — it just means there is no monthly commitment to do so. In fact, leaving a house that is not fully paid off to beneficiaries is not as novel as some might think. A reverse mortgage does exactly that.

Reverse mortgages allow homeowners to convert their home equity (that has built up over the years) into cash. There is no monthly repayment for the loan (the sum of home equity withdrawn) while interest and insurance payments are added to the balance, all of which must be repaid (by the beneficiaries) when the homeowner dies or the house is sold. Reverse mortgages, typically for older homeowners, are available in many countries, including Australia, Canada and the US. Cagamas launched Malaysia’s first reverse mortgage scheme in December 2021.

In the US, the loan is guaranteed by the federal government — for the protection of homeowners, lenders and beneficiaries, in cases where proceeds from the house sale are less than the loan amount. The upfront insurance premium is 2% of the property value or maximum claim (whichever is less) and 0.50% annually on the outstanding balance of the loan.

Similar to our proposed perpetual mortgage, the underlying capital gains (increase in house value) is left to beneficiaries while the homeowner enjoys the comfort of use now.

We have explained why property prices have trended higher historically and why they are likely to continue doing so, periodic market corrections notwithstanding. This is why most people are biased towards owning instead of renting, and why homeownership is a cornerstone of life. In the Asian culture, buying a home is a social norm and almost an expected rite of passage for young adults. We invest the bulk of our savings in a home. And this has proved to be the correct decision, given that investment in housing has outperformed inflation and done better than savings in banks.

It is also true that the current environment of rapidly rising interest rates may result in more volatile property prices — prices may stay flattish or even drop in the near term. For some, greater uncertainties may be reason enough to shift towards rental. And that is fine. We have some thoughts on public housing for rental too, which we hope to share in a future article.

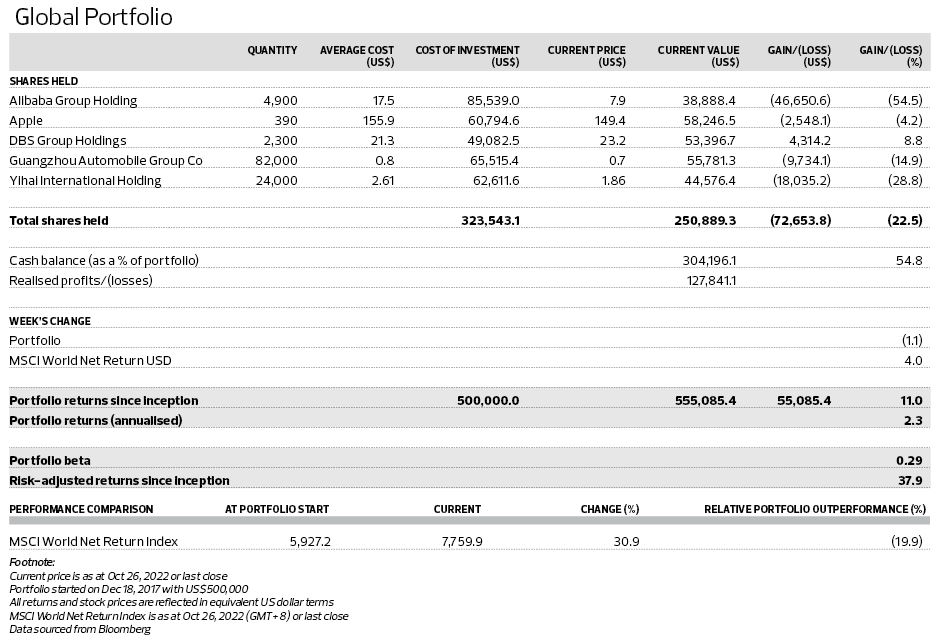

The Global Portfolio declined 1.1% for the week ended Oct 26, weighed down by heavy losses for Chinese stocks. There was a huge selloff by foreign investors immediately after the conclusion of the Chinese Communist Party Congress where President Xi Jinping solidified his leadership. Shares for Alibaba Group Holding fell 14.3% while Guangzhou Automobile Group Co ended 3.8% lower. On the other hand, Apple (+3.8%), DBS Group Holdings (+0.8%) and Yihai International Holding (+0.4%) finished higher for the week. Total portfolio returns since inception now stand at 11%, trailing the MSCI World Net Return Index’s 30.9% returns over the same period.

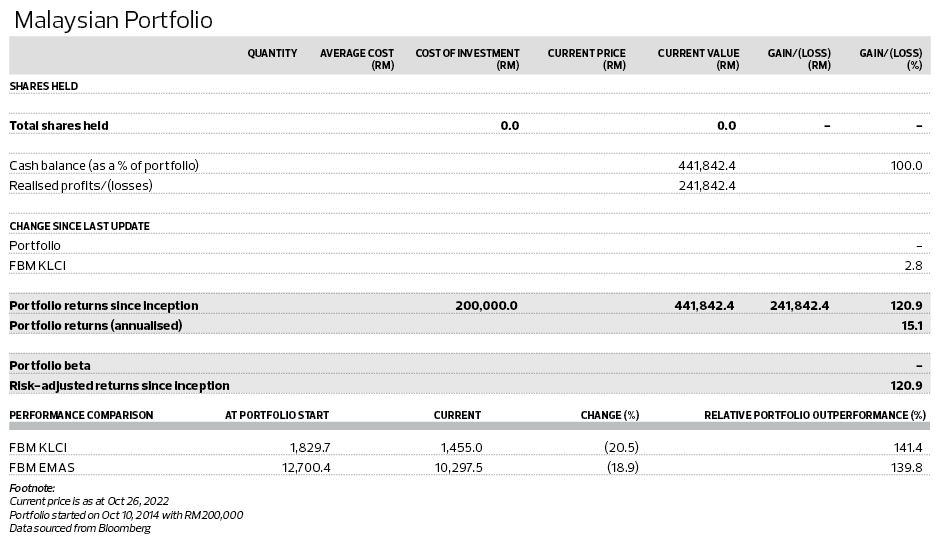

The FBM KLCI was up 2.8% last week while total returns for the all-cash Malaysian Portfolio remained at 120.9% since inception. This portfolio is outperforming the benchmark index, which is down 20.5% over the same period, by a long, long way.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.