Bank Negara: Most Malaysians can 'tahan' drastic income and housing price falls

PETALING JAYA (April 3): Banks and most households in Malaysia can withstand severe house price and income falls, according to Bank Negara Malaysia (BNM), based on a series of housing price shock simulations carried out to determine the resilience of households and banks to survive in the event of such hypothetical housing market correction.

"These can be attributed to generally prudent loan affordability standards applied by banks when extending loans to households, and the strong levels of capitalisation maintained by Malaysian banks,” BNM said in its Financial Stability Review for Second Half of 2019 report released today.

These were the scenarios under the simulation:

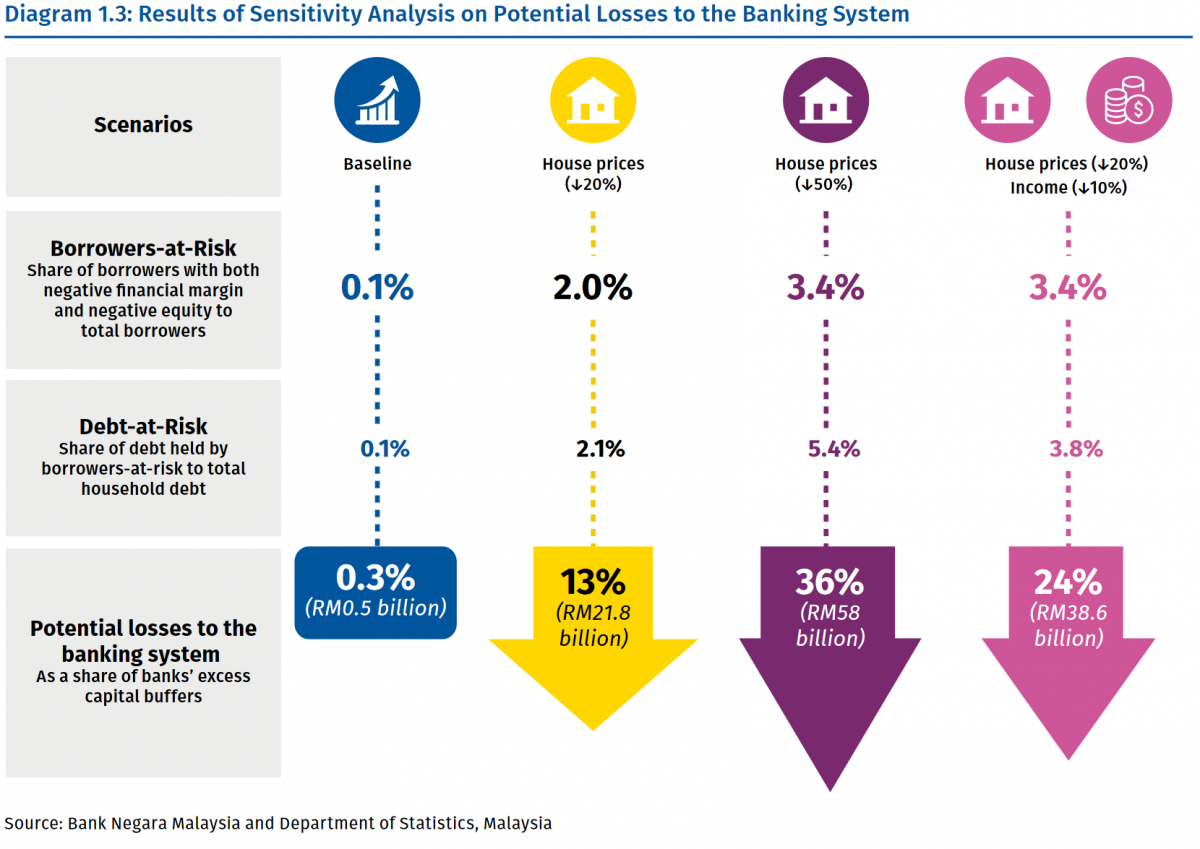

Scenario 1: A 20% housing price decline double that of during the Asian Financial Crisis (AFC) in 1998 would increase the risk of defaults by 2%.

Scenario 2: A 50% housing price decline due to a reversal of more than nine years cumulative house price growth would increase the risk of defaulting by 3.4%.

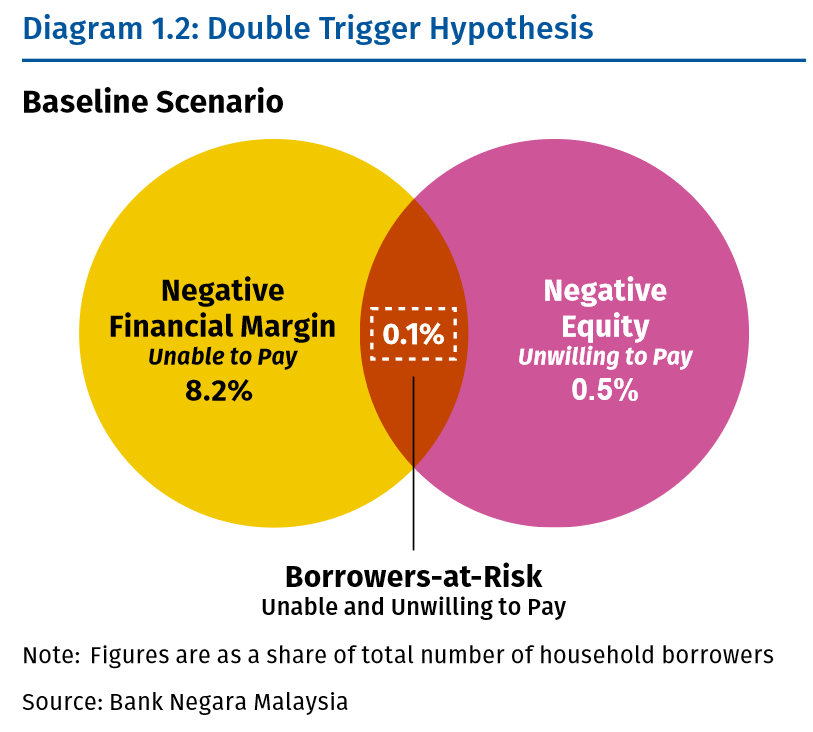

Both risk figures are an increase from a baseline at-risk borrowers figure of 0.1%.

Correspondingly, losses to the banking system including potential cross-defaults on other loans would amount to 13% (RM21.8 billion) and 36% (RM58 billion) of banks’ excess capital buffers, for each of the respective scenarios above.

Scenario 3: A simultaneous 10% decline in income (larger than AFC’s 8.7%) coupled with a 20% house price decline would result in the share of borrowers-at-risk increasing to 3.4% of total borrowers, with losses equivalent to 24% of banks’ excess capital or RM38.6 billion – less damage than Scenario 2.

According to BNM, Scenario 3 borrowers tend to be highly indebted with a debt service ratio of close to 80% and are mainly from the middle-income group living in Kuala Lumpur, Selangor, Johor or Penang.

They also tend to purchase houses that on average are priced at about 33% higher than houses purchased by borrowers who are not at risk. Borrowers with more than one housing loan are also seen to be at higher risk, the report stated.

The stress tests also examined how borrowers would react to shocks – in an event their home values dip below that of its total outstanding loan amount coupled with that of their income levels, after spending on basic needs such as (i) food and non-alcoholic beverages; (ii) housing rental and maintenance; (iii) water, electricity, gas and other fuels; (iv) transportation; (v) education; (vi) healthcare; and (vii) communication services.

Based on the tests, it was deduced that loan defaults may not usually occur and that most households would compensate their shortfall by dipping into other assets such as their Employees Provident Fund (EPF) or borrow from family and friends to avoid defaulting and damage their creditworthiness.

“Defaulting is also unfavourable for owner-occupiers, who account for the majority (82%) of Malaysian housing loan borrowers, as this would result in the borrowers losing their homes,” said BNM.

However, households are more likely to default when both conditions – inability to repay and negative equity – are met as in the "Double Trigger Hypothesis" described in Scenario 3.

“Households with negative financial margin and negative equity are in a particularly perilous position as they lack both the incentive and means to repay their loan,” the central bank added

Stay calm. Stay at home. Keep updated on the latest news at www.EdgeProp.my #stayathome #flattenthecurve

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

View AllFollow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.